More and more target-date funds are coming with annuities advertising “income for life.” Issuers include BlackRock and Vanguard. I’m going to explain why I’m recommending that clients not buy these either inside or outside of a target-date fund. Rather than just criticize, I’ll provide two better alternatives.

Morningstar’s Samantha Lamas and Jason Kephart wrote about the pros and cons of these annuities within the funds. Jason also recently wrote another article titled Guaranteed Income in Your 401(k)? Sounds Good in Theory. They explain the different versions, so I’m not going to repeat that in this article.

Income for Life?

A first look at these annuities shows something very attractive. I estimate that an income annuity within a 401(k) would pay 7.46% annually for a 65-year-old woman. That is, $100,000 would pay $622 a month, or $7,464 annually, in what they say is “guaranteed lifetime income.” Compare that with a 30-year Treasury yielding only 5.12%, or only $5,122, annually. The argument I’ve heard many times is that the annuity can pay a higher income due to risk pooling—meaning that those who die earlier will be subsidizing those with long lives.

While there is some truth to the benefits of risk pooling, it doesn’t explain the vast majority of the higher cash flow over Treasuries. The Treasury bond really is income, as it’s not eating into principal. The annuity, on the other hand, is not all income. A large portion is paying back principal that the investor has within the 401(k). I’m not recommending a 30-year Treasury bond, but one could also spend down some of the bonds to live on. So, my first point is that an annuity is really a cash payment of both principal and interest and is not income for life.

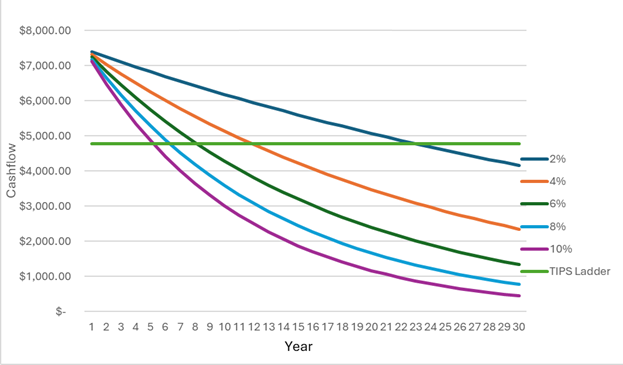

The Inflation Worry

My next point is that I teach all of my clients to “get real.” That means think in real inflation-adjusted terms. Jason mentions inflation, stating: “Inflation is another challenge because most payments are fixed and lose purchasing power over time.” I agree wholeheartedly. Inflation is incredibly anxiety-inducing, and we are all feeling it now as the cost of almost everything is far more expensive than only a year ago. The April Consumer Price Index came in at 0.6% over the previous month and 3.8% over the prior year. Without food and energy, prices rose 0.4% and 2.8%, respectively. If that weren’t bad enough, the Producer Price Index rose 1.4% over the prior month and 6% over the past year. The Producer Price Index is perhaps even more important, as it’s indicative of the future CPI. All of these numbers are well above the Federal Reserve’s 2% annual target. The US debt and deficit are in uncharted territory. It’s not that I know the future, but the possibility of long-term high inflation does scare the heck out of me.

In the chart below, I show what happens to spending power based on what annual inflation ends up being in the next 30 years. If the Federal Reserve does manage to hit its long-term target of 2% annual inflation, which I would bet heavily against, 44% of the spending power would be wiped out in 30 years. But 10% annual inflation would wipe out over 96% of that spending power. I’m not going to recommend rolling the dice and counting on low inflation. If inflation is high, the value of the longevity protection is virtually wiped out.

Some annuities can come with fixed cost-of-living adjustments, meaning they will increase by a fixed percentage point annually, such as 2%. Of course, they start at a much lower first payment, and counterintuitively, they actually increase inflation risk because the duration of the payments is longer. Even Vanguard, which just issued a paper titled “Vanguard’s Principles for Retirement Income,” mentioned inflation 43 times, yet makes the assumption inflation will run at only 2% annually.

I don’t believe I’m alone in my inflation anxiety. I’ve worked with a lot of actuaries and find them to be really smart people. Many years ago, the insurance industry offered annuities tied to the CPI, but they no longer exist. I believe it was because the insurance industry’s actuaries were unwilling to take that risk. Though several folks from the insurance industry counter by telling me they dropped the product because few were buying, I’m skeptical.

The ‘Annuities’ I Am Recommending

I have essentially bought two “annuities,” though they aren’t through insurance companies. I recommend both.

The first was mentioned by Jason, who stated: “Delaying Social Security can help maximize lifetime benefits, but many retirees may not have the flexibility to wait until age 70.” By waiting until age 70, I’m increasing my payment by 8 percentage points annually, and that extra payment increases with inflation. Beyond that, it has a survivor benefit in that my wife will get that payment when I pass, assuming she outlives me. Back when the insurance industry did offer inflation-adjusted annuities, I calculated that delaying Social Security was the equivalent of buying the annuity at a 40% discount. There is always some risk, of course, but I reframe the decision as if I were actually taking Social Security and using the funds to buy the best inflation-protected annuity on the planet.

I don’t agree with Jason’s comment in this context that some may not have the flexibility to wait, because one can always roll the 401(k) to an IRA and begin withdrawing some of the money. In other words, if they have the funds to buy the annuity, then they have the funds to withdraw money to live on in the meantime and buy the better “annuity” known as Social Security.

The second “annuity” I often recommend is a Treasury Inflation-Protected Securities ladder. A 30-year TIPS ladder is now paying out 4.8% annually in inflation-adjusted dollars. Building a TIPS ladder is buying TIPS that mature each year to provide an inflation-adjusted annual cash flow, which I explain here. The cash flow is composed of a real 2.6 percentage points of inflation-adjusted income, and the rest is the return of inflation-adjusted principal. I think of it as a 30-year period certain annuity. In the chart, I show a TIPS ladder paying an inflation-adjusted $4,780 annually. With even 4% inflation, it provides more spending power than the insurance annuity by the 12th year. While it doesn’t have the longevity protection beyond 30 years, the Society of Actuaries shows a 65-year-old woman will, on average, live to age 90. If you want more longevity protection, put 10% of that money in a low-cost stock index fund and don’t touch it for those 30 years. It lowers the payment by 10% but provides real longevity protection.

Both of my solutions are backed by the US government, whereas the insurance annuity is backed by an insurance company, which has default risk. While there are state guarantees for insurance products, the states would have to get the funds from other insurance companies, and that would be unlikely in a systemic environment affecting the entire insurance industry.

Better Options Than Annuities

An insurance annuity feels great, and we sure would like a higher payment upfront. Yet the nominal payments mean the buying power will almost certainly erode and, potentially, virtually disappear. If actuaries aren’t willing to roll the dice on inflation, I’m not going to recommend that anyone else do so. If one can afford to buy an insurance annuity either within a target-date fund or otherwise, then they can use the funds to delay Social Security. If one wants more than Social Security can provide at age 70, a TIPS ladder is superior to an insurance annuity.