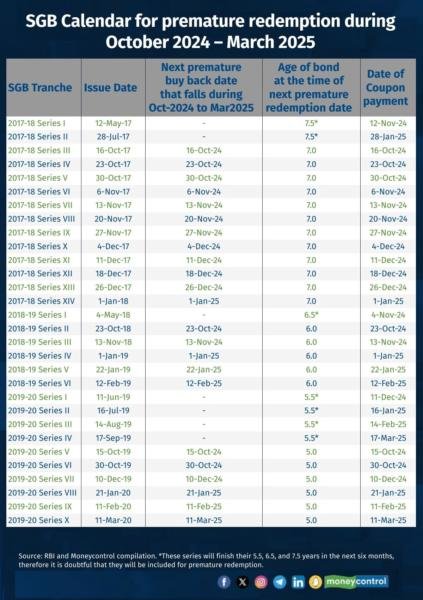

As many as 30 Sovereign Gold Bonds (SGB) are coming up for redemption in the next six months between October 2024 and March 2025. Many of these SGBs are up for premature redemption, meaning they have completed five, six and seven years.

It must be noted that capital gains on these bonds are exempted only if you tender the units using the Reserve Bank of India’s (RBI) premature exit window. If you miss this small window and sell your SGBs on the stock exchange instead, then the capital gains will be taxable.

The RBI releases this list twice a year to notify SGB unitholders of the deadlines for submitting applications for premature redemption. As per the list, there are 30 SGB series eligible for premature redemption in the next six months.

Of these, Seven series will finish their 5.5, 6.5, and 7.5 years in the next six months, therefore it is doubtful that they will be included for premature redemption.

A flexible exit window

SGBs are government-backed gold bonds issued by the RBI. These bonds were first launched in November 2015 and have been sold in 67 tranches subsequently.

SGBs are eight-year instruments but impose a five-year lock-in. Although SGBs are listed on the stock exchanges, most of them are thinly traded. However, the RBI provides a buyback facility at the end of the fifth, sixth and seventh years. Unitholders can submit their redemption requests during the designated windows through Receiving Offices, NSDL, CDSL, or RBI Retail Direct.

Read here: Will customs duty cut hurt investors in sovereign gold bonds maturing in 2024?

How do I tender my SGB units?

Inform your agent, bank or post office that enabled you to buy these bonds. Make sure you initiate your redemption request at least 10 days before the interest payment date. Premature redemption requests are accepted by the RBI beginning one month before the coupon payout date.

The redemption price will be a simple average of the closing price of gold during the previous week (Monday to Friday) published by the India Bullion and Jewellers Association. The redemption proceeds are transferred to your bank account.

Interesting trends in the past premature redemptions

From 2015, the RBI has launched 67 SGB tranches and issued 14.7 crore units.

The RBI has so far facilitated 61 premature redemptions for the SGBs completing fifth, sixth and seventh years with average redeemed units of 17,000.

Interestingly, the number of units surrendered for the SGBs that completed the fifth and sixth years was lower than the surrender of SGBs that completed the seventh year.

The units surrendered in the last six months using the premature window for SGBs completed the fifth year were very low with an average of just 2,500 units. This also shows the rising popularity of gold as an instrument and how investors like to hold gold for as long as they can.

That there is little or no scope for new SGB launches adds to the list of reasons why premature redemption windows have drawn fewer tender requests of late.

A compelling substitute for physical gold

SGBs are substitutes for holding physical gold. The bonds were issued in denominations of one gram of gold and multiples thereof.

They score over other gold investment options as they pay a fixed interest on the holding (2.5-2.75 percent per annum) apart from giving a discount of Rs 50 on the issue price if invested online at the time of initial offer.

Unlike other gold asset classes like gold exchange-traded funds (ETFs) and physical gold, the coupon rates offered by SGBs are an added advantage.

Tax advantage on SGB premature redemption

In terms of tax treatment, if individuals redeem their SGB investment at maturity (after eight years), they are not liable to pay capital gains tax.

For premature redemption, capital gains are exempt if you redeem your SGBs through the RBI’s window.

Nirav Karkera, Head of Research at Fisdom, says, “Considering how the premature redemption will be by way of tendering the bonds back to the issuer and not through a transfer through the exchange, the gains here will be tax exempt.”

However, if you sell your SGBs outside of this window or on the stock exchange, the capital gains will be taxable according to your income tax slab.

All the SGB series are listed and traded in the cash segment of the BSE and NSE. Investors can buy and sell them through demat accounts. Liquidity has been an issue in most of the SGB series. The daily average traded volume of the top 10 most liquid SGBs on NSE over the last three months was Rs 90 lakh.

Read here: No new sovereign gold bonds? Check out the most liquid ones on the NSE

Increase in demand in the secondary markets

SGBs traded in the secondary markets have seen a surge in the traded volume in recent periods. This is probably due to less chance of fresh SGB issues going forward. On August 17, Moneycontrol reported that the highly liquid SGBs were traded at a 5-12 percent premium to their reference rates.

Read here: Why are Sovereign Gold Bonds trading at 5-12% premium?

Should you withdraw or stay invested?

Gold has been considered as a hedge against inflation and economic uncertainties.

“Gold should be looked at as an asset allocation product rather than looking at only from a returns perspective. Considering that the gold has rallied over the last few years, those investors who had invested for returns can opt for this premature exit window. Investors who are looking for diversification should hold their SGB investment,” says Harshad Chetanwala, Co-Founder, MyWealthGrowth.com.

Those seeking to maintain a strategic allocation to the asset class and instrument can continue to hold, advises Karkera. “We maintain a bullish bias on gold with the positive outlook being further supported by a variety of factors that could lead to an earlier-than-expected rate cut by the US Fed and related softening for the dollar,” he adds.If the value of your SGB holding now exceeds about 10 percent of your overall portfolio, then you can take some profits off the table. Else, stay invested.