Screening specific qualities for your portfolio.

© Scrudje/stock.adobe.com, © Dmitriy/stock.adobe.com; Photo illustration Encyclopædia Britannica, Inc.

Investors and fund managers are always looking for ways to beat the market. Many financial researchers spend their entire careers slicing, dicing, and modeling data to find the common traits that drive asset returns. Sounds like a perfect match, right?

That’s the philosophy behind factor investing—seeking the attributes that drive stock returns and tailoring a portfolio around the best ones. It’s not just a Wall Street gimmick; rather, it’s based on decades of academic research studying securities’ movements. Active managers at institutional firms used these strategies for decades.

Key Points

- Factor investing is based on decades of academic research, beginning with the 1964 capital asset pricing model (CAPM).

- Top factors include size, value, market risk, profitability, and the company’s investing strategy.

- The terms “factor based” and “smart-beta” are used interchangeably, but there are differences, although some see smart-beta as a subset of factor investing.

Factor investing became accessible to retail investors when exchange-traded fund (ETF) issuers began to offer funds designed to take advantage of that academic research in an attempt to beat stock market benchmarks over time. Although this investing style is based on research, past performance doesn’t guarantee future results. Factors can underperform or outperform depending on economic cycles, and anomalies can extend longer than usual before reverting to their historical tendencies.

What is factor investing?

In the investing world, a factor is an attribute or a characteristic that can drive returns over time and in different asset classes. The idea behind what has become factor investing started in the 1960s, when economist William Sharpe created the capital asset pricing model (CAPM) and introduced the concept of beta, which measures how sensitive a stock is to the broader market’s movement.

Two University of Chicago professors Eugene Fama and Ken French (now at Dartmouth College) built on Sharpe’s model in 1993. They found certain investment factors such as a company’s size (market capitalization), a firm’s price-to-book ratio, and market risk would outperform the broader S&P 500 over time. Their model was called the Fama-French three-factor model. Other researchers, including Mark Carhart of the University of Southern California, drew on this work with their own factor-investing research.

The “fab five” of factor investing

As factor investing grew popular in the 2000s, researchers began to suggest there were dozens of investment factors for asset pricing beyond the Fama-French model, resulting in what some quantitative researchers called “the factor zoo.”

Fama and French expanded their three-factor model to five:

- Size. Small-cap companies will outperform large-cap companies (known in the model as small minus big).

- Value. Cheaper companies (as measured by the price-to-earnings or P/E ratio) will, over time, outperform more expensive companies (high minus low).

- Market risk. Known as systematic risk, it’s the risk of loss that affects all markets to some degree (e.g., changes in interest rates or a rise in unemployment).

- Profitability. Stocks with higher operating profit perform better (robust minus weak).

- Investment. Companies that aggressively invest versus those that don’t have lower returns (conservative minus aggressive).

Other quantitative researchers find that momentum, quality, and low volatility are also distinct factors, and many fund companies issuing factor ETFs use them as well.

What are factor ETFs?

A factor ETF may incorporate specific criteria to express a certain style (such as quality or profitability), or it may combine two or more factors in what’s known as a multifactor ETF.

Factor ETFs differ from other types of ETFs by their construction. Most factor ETFs are passive, index-based funds in the same way that plain-vanilla index ETFs such as the SPDR S&P 500 ETF Trust (SPY) tracks the performance of the S&P 500 or the Technology Select Sector SPDR Fund (XLK) tracks the information technology sector. The difference is which factor(s) are targeted.

For example, the Invesco S&P 500 Low Volatility ETF (SPLV) is a factor ETF that includes the 100 least volatile stocks in the S&P 500. The iShares Edge MSCI USA Quality Factor ETF (QUAL) includes stocks deemed financially strong and poised for growth.

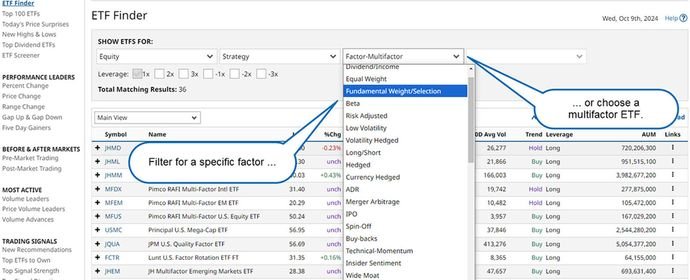

One way to find factor ETFs is to search by name, such as “momentum ETFs” or “value ETFs.” Most fund issuers will put the style of factor in the name of the fund. And, depending on the brokerage or trading platform you use, you may be able to screen for the criteria you want (see figure 1).

Figure 1: SCREEN TIME. Your brokerage or trading platform may allow you to set up “screeners” to help you find the right factor (or factors) to align with your strategy. Source: Barchart.com. Annotations by Encyclopædia Britannica. For educational purposes only.

Source: Barchart.com. Annotations by Encyclopædia Britannica. For educational purposes only.

Smart beta versus factor

The terms smart beta and factor are often used interchangeably, but they are different (although some see smart beta as a subset of factor based). Smart beta can include both active and passive strategies, and smart beta strategies can include factors such as selecting quality or low P/E companies. Most pure factor ETFs, however, are passive, index-based approaches.

One popular smart beta strategy seeks to break the link with traditional market-cap-weighted indexes such as the S&P 500 or Nasdaq-100 in an effort to outperform them. These smart beta ETFs may “equal-weight” constituent holdings so that no one stock dominates.

For example, the Invesco S&P 500 Equal Weight ETF (RSP) includes the same exact companies as the S&P 500, but holds them such that each is about 0.22% of the ETF. Conversely, as of October 2024, Apple (AAPL), which is the top company in the world by market cap, represents 6.9% of the the S&P 500. That means a big rally or selloff in Apple shares would have an outsize impact on the S&P 500, but in an equal-weighted S&P 500 ETF, it would have the same 0.22% impact as any other stock in the ETF.

Factor ETFs can underperform

Factor ETFs are rooted in academic research, but that doesn’t mean they’re infallible. Factors are affected by economic and market cycles, and sometimes they go out of style for a while.

One recent example: The value factor and the small-cap factor underperformed for years while large-cap growth stocks—led by technology companies—outpaced both value and small-cap indexes. In 2020 alone, large-cap growth indexes outperformed large-cap value indexes by more than 35%, according to Russell Investments. That’s the largest margin of difference between the two in any calendar year.

Fund issuers may combine factors to create multifactor ETFs; for example, they might pair size and quality. Because some factors are not correlated, combining two or three can improve performance. But watch for factor stuffing, where issuers combine multiple factors that may cancel each other out, or become so broad that they mirror the profile of a traditional index fund—but with a higher expense ratio.

The bottom line

If you’re considering factor ETFs, remember that the academic research was focused on long-term returns, not short-term performance. Factor investing is geared more toward retirement savings than short-term momentum trading.

When you seek a factor ETF, study the strategy and the holdings, which can be found in the prospectus. How a fund issuer constructs the strategy and defines the criteria matters. For example, two “quality” ETFs may hold different companies (or in different quantities) depending on how the issuer defines quality.

And as with any other investment, know your goals, your risk tolerance, and time horizon, and remember that past performance doesn’t guarantee future returns. Academic research—like all fundamental analysis—is backward looking, and thus can’t predict the future.

Specific companies and funds are mentioned in this article for educational purposes only and not as an endorsement.