The majority of those with savings or investments would abandon transferring their funds to alternative providers because of delays and complexity, according to research.

Commissioned by entrepreneur and consumer champion Saira Khan, the study combined in-depth focus groups with a survey of 1,000 adults who hold savings or investments.

The research found delays are seen as the single most important challenge when trying to switch investments with 70 per cent abandoning a switch when the process is too slow or complicated.

The findings point to widespread frustration with lengthy transfer times, inconsistent processes, and a lack of transparency.

The consequence is that they will lose the chance to move to companies offering higher interest rates, lower charges and better returns — and 72 per cent believe providers are deliberately making it harder to switch.

Khan said the research findings echoed her own experience.

“People are so frustrated and angry at these unnecessary delays it can feel like their money is being held hostage,” she said.

“In my five years working alongside Martin Lewis, I heard stories like this repeatedly of consumers being denied the best deals, often by outdated processes and industry apathy.”

The report also revealed that 94 per cent said switching investment providers should be fast, and 79 per cent said it should be straightforward.

Yet, just 9 per cent believed switching stocks and shares platforms is fast, compared with 41 per cent who said the same about switching mobile or energy providers.

Meanwhile, when told that in-specie transfers — the movement of assets such as shares, Isas, or pensions between providers without selling them for cash — can take up to 100 days, 75 per cent said they would be less likely to move their investments.

More than half, 57 per cent, said such delays would deter them even more during periods of market volatility.

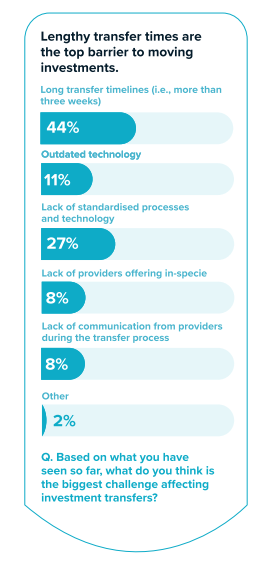

Almost half (44 per cent) also said lengthy timelines are the biggest barrier to moving investments, with 27 per cent blaming outdated systems and a lack of standardisation.

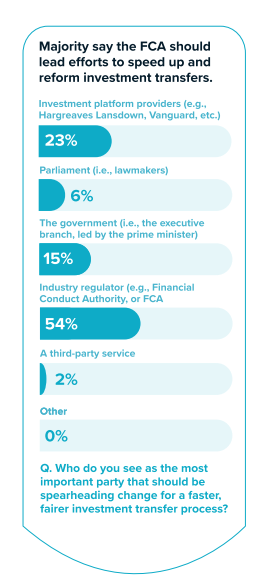

The report also revealed that a majority (54 per cent) believed the FCA should lead reform, compared with 23 per cent who said providers themselves should take the lead.

More than half (55 per cent) support strict maximum transfer deadlines backed by escalating financial penalties, while 41 per cent back mandatory real-time transfer tracking.

Khan said: “These delays have real consequences for millions of investors. They stop them from switching to better deals, higher returns and lower charges.

“That is why we are calling on regulators to step in now to demand faster timeframes and impose tough fines on those who fail to meet them.

“I am also setting up the Fair Switching Initiative so that people can join us in demanding a fairer, faster system.”

The report concluded there is strong public backing for reform, and that binding transfer deadlines, enforceable penalties, and modernised digital standards are essential.

Without clear standards, slow and fragmented transfer processes will continue to limit competition and restrict the flow of investment that supports growth across the UK economy.

FT Adviser does not believe it should be that hard to get average transfer times down, which is why we have launched out campaign to tidy up transfers.

sonia.rach@ft.com