")

Many Canadians have mutual fund and/or segregated fund investments that impact what they owe in income tax. While, at a high level, these investments are similar in purpose and structure — they allow investors to pool their money and invest in a diversified portfolio of securities — there are differences and other points of note that may attract investors to one or the other.

Here are five things to note, especially during tax-filing season when receipts are being gathered and taxes payable for the previous year is being determined.

1. T3s, T5s and T5008s

Both mutual funds and segregated funds might earn income (e.g., interest, foreign income or Canadian dividends) and realized capital gains within the fund. While net income and capital gains are taxable, they normally flow-through to investors and are taxed in their hands, as opposed to at the fund level, at potentially higher tax rates. (Segregated fund capital gains and losses are deemed to be gains and losses of the investor.)

Mutual fund trust and segregated fund investors normally receive a T3 tax slip for non-registered accounts (Releve 16 for Quebec tax purposes). Mutual fund corporation investors normally receive a T5 (Releve 3 in Quebec). Amounts paid or allocated for registered accounts would not produce a tax slip as income and gains for these accounts benefit from the tax-advantaged status of the account.

For mutual fund trusts and segregated funds, income and gains typically retain their character when flowed to investors. Interest earned at the fund level is taxed as interest income at the investor level for Canadian investors. The same is true for foreign income, Canadian dividends and realized capital gains.

Mutual fund corporations are not flow-through entities — while their investors would still typically report net income or gains realized at the fund level, the income would normally be Canadian dividends or capital gains dividends for tax purposes regardless of source. Mutual fund corporation investors cannot receive interest or foreign income from the investment.

T5008 tax slips (Releve 18 in Quebec) are normally issued to mutual fund trust and mutual fund corporation investors in respect of the redemption of their units or shares. Along with their year-end client statements, investors would calculate and confirm their capital gains and capital losses realized from the sale of their investments, and report this information on their tax returns for the year of the sale.

Segregated fund investors do not receive T5008 tax slips for the sale of their notional units. While they too would normally have capital gains or capital losses triggered from the sale of their notional units, because these are insurance contracts, this information is calculated at the contract level and reported to investors on T3 tax slips for the year.

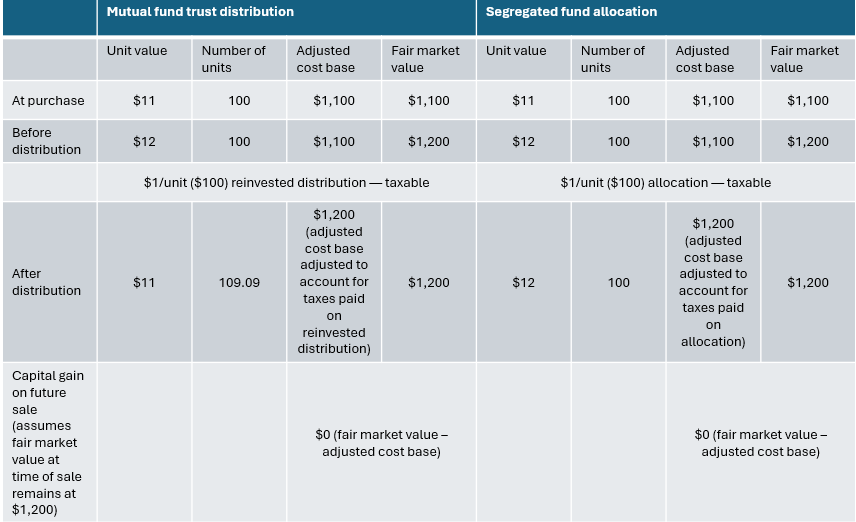

2. Distributions vs. allocations

Mutual funds (both trusts and corporations) distribute taxable income and capital gains earned within the fund to investors. Segregated funds allocate income and gains to investors. While the overall tax treatment at the investor level is similar for both structures, the process for getting there is different.

When mutual funds pay a distribution to investors, the value per unit for the fund decreases. Investors can receive the distribution in cash or can reinvest it to purchase additional units of the fund. When the distribution is reinvested, the adjusted cost base (ACB) of the investment increases to avoid double taxation when the units are eventually sold.

When segregated funds allocate amounts to investors, no amount is paid from the fund. There is no change in the fund’s net asset value and no additional units are purchased. However, similar to reinvested distributions with mutual funds, while segregated fund allocations are taxable, the ACB of the investment is increased to avoid double taxation on future sale.

This table compares the distribution and allocation procedures for mutual funds and segregated funds. While the procedures differ, the tax treatment is the same, assuming the same type of income.

3. Flow-through of capital losses

Mutual funds cannot distribute capital losses to investors. Instead, net capital losses realized at the fund level are carried forward for use within the fund in a future year.

Segregated funds, on the other hand, allocate net capital losses to investors. Such losses, would appear on a T3 slip issued to the investor for the year, allowing the investor to claim the capital loss on their personal tax return for that year. Where the investor’s capital losses exceed capital gains for the year, their net loss can be carried back to offset capital gains in any of the three previous years or can be carried forward for use in any future year. This provides segregated fund investors with flexibility to manage their fund-related losses.

For mutual funds, while net capital losses cannot flow-through to investors, they would normally be used at the fund level to offset capital gains in future years, reducing the potential for taxable distributions to investors for those years.

4. Interest deductibility

Where borrowed money is used to invest in mutual funds within the non-registered environment, the federal Income Tax Act (ITA) allows investors to deduct their interest cost each year, provided the money continues to be invested in an investment that has the potential to pay income (e.g., dividend income, foreign income).

It should be noted that investments that produce only capital gains would not normally qualify as eligible for these purposes as there would be no reasonable expectation of income. Also, interest on borrowed money used to invest within registered accounts such as RRSPs, TFSAs and first home savings accounts is not tax-deductible.

Consider for example an Ontario resident who received an investment loan from their local bank which they used to purchase a mutual fund — a balanced fund for their non-registered portfolio. While interest and dividend income from the investment is not guaranteed each year, the mandate of the fund does not prevent it, and both income types are distributed to mutual fund investors as it is earned. Because of the potential to earn income from the investment, interest paid on the investment loan is tax-deductible.

Generally, where borrowed money is used to acquire an interest in a life insurance policy, the interest cost is non-deductible. That said, while segregated funds are insurance contracts, there is a section of the ITA that exempts a policy “that is an annuity contract all of the insurer’s reserves for which vary in amount depending on the fair market value of a specified group of properties.”

Segregated funds normally fall into this category, allowing for its investors to deduct related interest costs provided the investment has the potential to allocate income (not including capital gains) in the non-registered environment.

Eligible interest costs are deducted on line 22100 of the federal income tax return (T1) under “Carrying charges, interest expenses and other expenses.”

5. Deductibility of investment counsel fees

The ITA allows for a deduction of fees, other than a commission, paid for:

- advice related to the purchase or sale of securities of the taxpayer, or

- the administration or management of securities of the taxpayer.

While the tax rules do not define the term securities for this purpose, mutual funds are generally considered to meet the definition. When fees are paid by a mutual fund investor directly to a provider of the above services, a deduction is normally claimable on line 22100 of the federal income tax return, “Carrying charges, interest expenses and other expenses.”

Expenses incurred for registered accounts are not tax-deductible. Management fees paid to a mutual fund manager for the management of securities within the fund are normally deducted at the mutual fund level, providing an indirect benefit to the investor via a reduction of taxable distributions for the year.

As per Canada Revenue Agency (CRA) technical interpretation 2014-0542581E5, given their status as a contract of insurance, the CRA does not consider segregated funds to be securities for purposes of the above. While this position can certainly be debated, it suggests that the deductibility of this fee at the client level can be problematic. Segregated fund investors should discuss this matter with their tax advisor for a formal opinion on the deductibility of such fees.

Similar to mutual funds, however, where the fee is part of the segregated fund management expense ratio, the fee would normally be deducted at the fund level, providing an indirect benefit to the investor.

Both mutual funds and segregated funds are common and useful investments for many investors. While they are similar in nature, there are nuances. Understanding the differences and benefits of each product can allow for appropriate management of assets, tax minimization and the maximization of wealth.