Investors have long debated unit-linked insurance plans (ULIPs) versus mutual funds. ULIPs are sold as a two-in-one solution — life cover plus investment. Mutual funds, in contrast, are pure wealth-creation vehicles. Most commentary treats them separately, but category data show mutual funds have outperformed ULIPs across equity, debt and hybrid allocations. The differences aren’t always dramatic, but they are fairly consistent. For performance-driven investors, mutual funds are the clear winner. Unlike mutual funds, which follow SEBI’s defined mandates, ULIP categories are broader and more flexible, so comparisons are indicative, not exact. Data has been collated from Morningstar and Value Research as on September 24.

Allocation categories: Funds lead

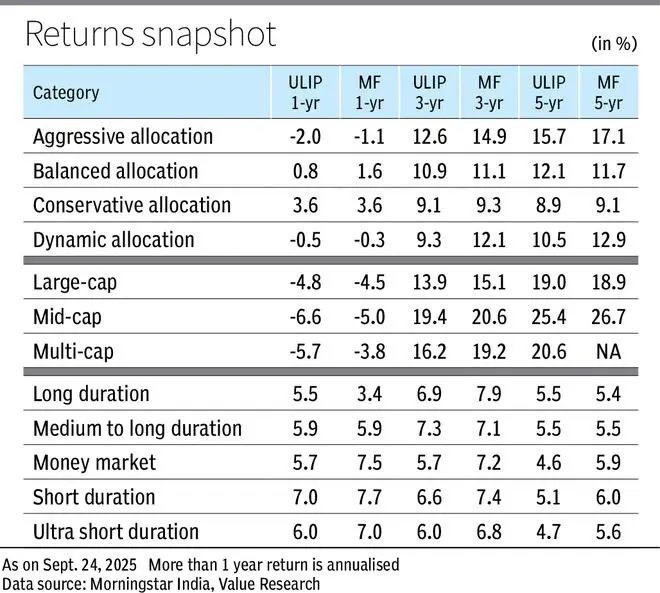

Both ULIPs and mutual funds offer mixed portfolios blending equity and debt, often under similar labels such as aggressive, balanced or conservative. That makes them natural comparables.

Aggressive allocation ULIPs returned –2.0 per cent, 12.6 per cent and 15.7 per cent over one, three and five years; mutual funds did better at –1.1 per cent, 14.9 per cent and 17.1 per cent. Balanced ULIPs at 0.8 per cent, 10.9 per cent and 12.1 per cent were close to funds at 1.6 per cent, 11.1 per cent and 11.7 per cent. Conservative ULIPs delivered 3.6 per cent in the past year against 3.6 per cent for funds, with three- and five-year averages converging around 9 per cent. Dynamic allocation shows the widest gap: ULIPs at –0.5 per cent, 9.3 per cent and 10.5 per cent over one, three and five years versus –0.3 per cent, 12.1 per cent and 12.9 per cent for funds.

ULIP allocation funds often rebalance less actively. Mutual funds are bound by SEBI’s hybrid category rules, which could be forcing sharper allocation discipline. Consequently, over three-five years, MFs squeeze out higher returns (over 200 bps more) as seen in dynamic strategies where timing matters.

Investors usually choose allocation products for stability and smoother returns. ULIPs match funds in balanced and conservative categories, but funds consistently lead in aggressive and dynamic strategies. Over time, even small performance gaps compound into meaningful differences.

Equity categories: Funds hold the edge

Equity-oriented ULIPs and mutual funds both promise wealth creation, but the tilt is in favour of funds. Large-cap ULIPs delivered -4.8 per cent, 13.9 per cent and 19 per cent over one, three and five years, compared with –4.5 per cent, 15.1 per cent and 18.9 per cent for funds. The performance difference is especially evident in mid-caps.: –6.6 per cent, 19.4 per cent and 25.4 per cent in ULIPs against –5 per cent, 20.6 per cent and 26.7 per cent for funds. Multi-cap ULIPs posted –5.7 per cent, 16.2 per cent and 20.6 per cent in one, three and five years, while funds managed –3.8 per cent and 19.2 per cent in one- and three-year periods (five-year not available).

Generally, mutual funds have broader research teams and active participation in IPOs, block deals and sector rotations. In contrast, ULIPs typically track a narrower set of benchmark stocks. Also, in volatile mid-cap space, even small differences in portfolio churn and expense leakage can widen the gap.

The above returns show that while ULIPs keep investors exposed to equity, mutual funds capture more upside. Yearly gaps may look marginal, but over long horizons they widen corpus differences. For long-term goals such as retirement or wealth transfer, mutual funds remain the more efficient choice. ULIPs, though competitive, work better when investors also value bundled cover.

Debt categories: MFs more efficient

Debt investments are usually chosen for stability and income. Here too, funds generally outperform. Money market ULIPs returned 5.7 per cent, 5.7 per cent and 4.6 per cent over one, three and five years; MFs did better at 7.5 per cent, 7.2 per cent and 5.9 per cent. Short-duration ULIPs posted 7 per cent, 6.6 per cent and 5.1 per cent, trailing funds at 7.7 per cent, 7.4 per cent and 6 per cent. Ultra-short ULIPs gave 6 per cent, 6 per cent and 4.7 per cent, compared with 7 per cent, 6.8 per cent and 5.6 per cent for mutual funds. In long duration, ULIPs actually lead over one year at 5.5 per cent versus 3.4 per cent for funds, but over three years fritter way much of the advantage.

Mutual funds run dedicated strategies (short duration, money market, etc.) with active calls on duration, credit quality and liquidity. ULIP debt funds are often managed conservatively (high G-Sec/AAA tilt) to minimise risk, possibly leading to slightly lower yields. Hence, in money market and short-term buckets, MFs consistently lead. ULIPs shined in longer-duration debt when government bond rallies lifted all boats.

For investors seeking predictability, mutual funds provide consistently better efficiency. ULIPs serve the purpose, but with lower yields. They may still appeal where insurance bundling or tax treatment is valued, but for pure fixed-income returns, mutual funds are the stronger option.

ULIPs were never meant as pure investment vehicles. Charges such as premium allocation, policy administration and mortality eat into returns. The fund numbers shown are before these deductions. Mutual fund returns, in contrast, are post-expense ratios, so closer to what investors receive. That explains their edge.

ULIPs aren’t irrelevant, though. For households without term cover, they offer bundled protection. Plus, they enjoy some tax sops. Subject to premium limits, ULIP maturity proceeds can enjoy exemptions under Section 10(10D).

Published on September 27, 2025