Even as investors eagerly seek an end to the ongoing conflict in West Asia, there are no signs of a thaw as yet, with the US President’s recent address to his nation adding to the anxiety of the already beleaguered Indian equity markets.

Furthermore, there is no clarity on when the Strait of Hormuz would be opened for regular goods traffic shipments without disruptions. The sharp rise in crude prices has brought fiscal calculations of the government under the scanner.

LPG cylinder prices have already seen price hikes. Any disruption or shortage due to the war may lead to higher inflation and possibility of higher interest rates as well, later in the year.

From a market perspective, along with mid and small-caps, large-cap stocks (perceived as resilient in volatile phases) too continue to face the heat.

Given their importance to most investor portfolios, underperforming large-cap funds can hamper financial goals and would thus need careful decision-making while making investment choices.

Many large-cap funds have struggled to get past the Nifty 100 TRI or BSE 100 TRI on a consistent basis.

UTI Large Cap (UTI Master Share), which is in its 40th year, has seen returns turn lukewarm for years now, going below many peers and standard benchmarks.

Investors can exit the fund and also stop any SIPs in the scheme and move to better-performing schemes.

Slackening returns

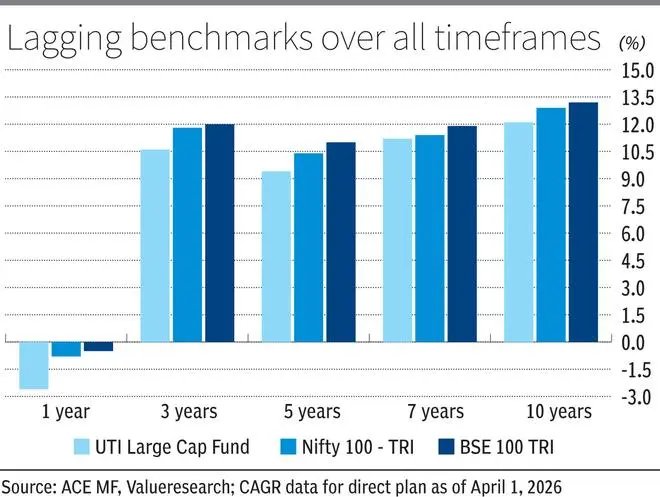

UTI Large Cap’s track record over the past several years has been underwhelming, with the fund’s performance falling below those of standard benchmarks and peers.

Over one, three, five and 10-year timeframes, the fund has underperformed the Nifty 100 TRI by 1-2.5 percentage points. The fund’s underperformance with respect to the BSE 100 TRI is also similar.

UTI Large Cap’s five-year point-to-point returns are moderate, at 9.4 per cent. In this timeframe, the Nifty 100 TRI gave 10.1 per cent and the BSE 100 TRI delivered 11 per cent. Even on a 10-year basis the fund lags these benchmarks.

When five-year rolling returns are considered from January 2013 to March 2026, the fund has outperformed the Nifty 100 TRI a mere 36.2 per cent of the times. The mean return for the fund in this rolling period is 13.7 per cent, while for the Nifty 100 TRI it is 13.9 per cent.

When returns on monthly SIPs (XIRR) over the past 10 years are considered, UTI Large Cap fund has given 10.3 per cent. A similar SIP in the Nifty 100 TRI would have delivered 11 per cent.

UTI Large Cap has an upside capture ratio of 96, indicating that its NAV rises less than the benchmark during market rallies. The fund has a downside capture ratio of 93.8, indicating that the scheme’s NAV falls less than the benchmark during periods of corrections. A score of 100 indicates that a fund performs exactly in line with its benchmark. Overall, these ratios point to prolonged underperformance.

This inference is based on data from March 2021-March 2026. All return figures and the ratios pertain to the direct plan of the fund.

Churning moderately

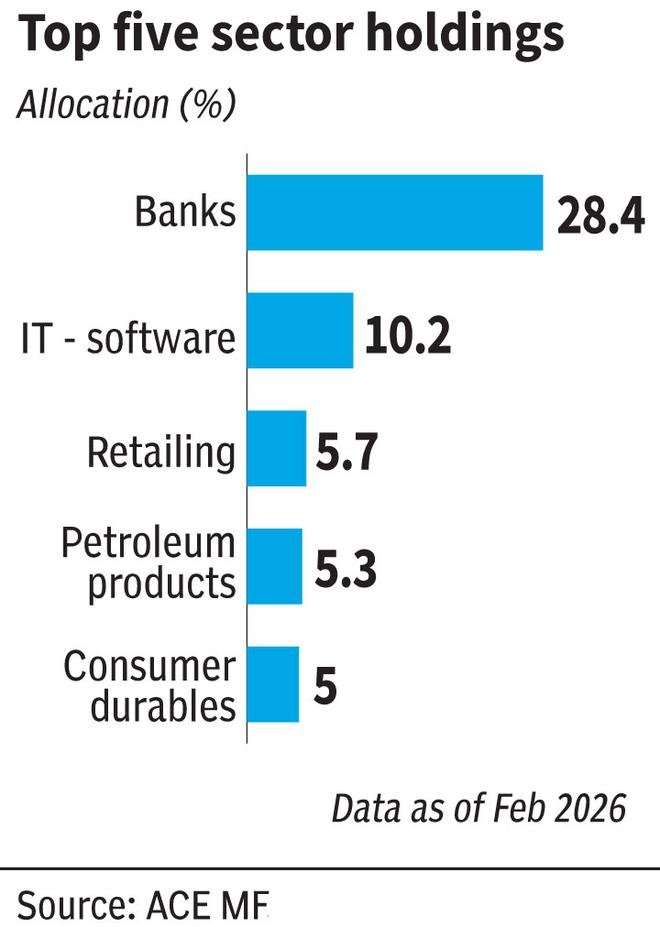

UTI Large cap sticks to being bluechip in character and principle with such stocks accounting for more than 87 per cent of the portfolio at most times.

Mid and small-caps find utmost 8-10 per cent weightage in the fund’s holdings. Cash and debt positions are restricted to 2-4 per cent most of the time.

As with most funds, more so from the large-cap stable, banks figure among the top holdings of the scheme.

Exposure to HDFC Bank, a major underperformer in the past few years, in recent months, and holding on to the likes of Kotak Mahindra Bank and Bajaj Finance which have had a weak run, has hurt returns.

IT software has consistently been the second largest holding for UTI Large Cap fund, despite the underperformance due to AI disruptions. Stocks such as Infosys, which corrected heavily, still find a place among the top holdings.

Not giving higher weightage to segments that have done well such as pharma/healthcare, automobiles, and so forth, has been another cause for the fund’s underperformance.

Instead, retailing and consumer durables figure among key holdings. The likes of Dmart, ITC and lackadaisical insurance picks such as HDFC Life have all added to erosion in returns.

Though there is a certain value orientation to the fund’s picks, it has not paid off well enough even over longer timeframes.

Published on April 4, 2026