Higher starting yields have reignited interest in bonds, but with the outlook for interest rates still uncertain and inflation proving stickier than some had predicted, the investment case may not be as straightforward as simply chasing high yields.

In addition to this, the conflict in the Middle East is putting renewed pressure on energy prices, which is already pushing inflation higher and putting greater stress on global economies.

As a result, fund managers such as Dan Caps, lead portfolio manager of the Evelyn Partners Index MPS range, are carefully managing duration exposure, both in nominal and index-linked exposure.

Why duration management matters

Caps explains: “In higher risk portfolios, we may also look to extend our duration exposure marginally to provide some disaster insurance.

“Should we see a growth shock that impacts our equity positions, we would expect to see interest rates cut quicker than currently anticipated, and in these conditions, some duration exposure should help support the portfolio.

“The extra yield offered in the credit space is also attractive, but with spreads historically tight, we again prefer to target the shorter-dated issues to control our spread duration.”

Caps stresses that duration control has been key throughout this rate-rising environment, noting that trying to predict the path of interest rates over the recent years has been “particularly perilous”, and more so compounded by the Middle East conflict.

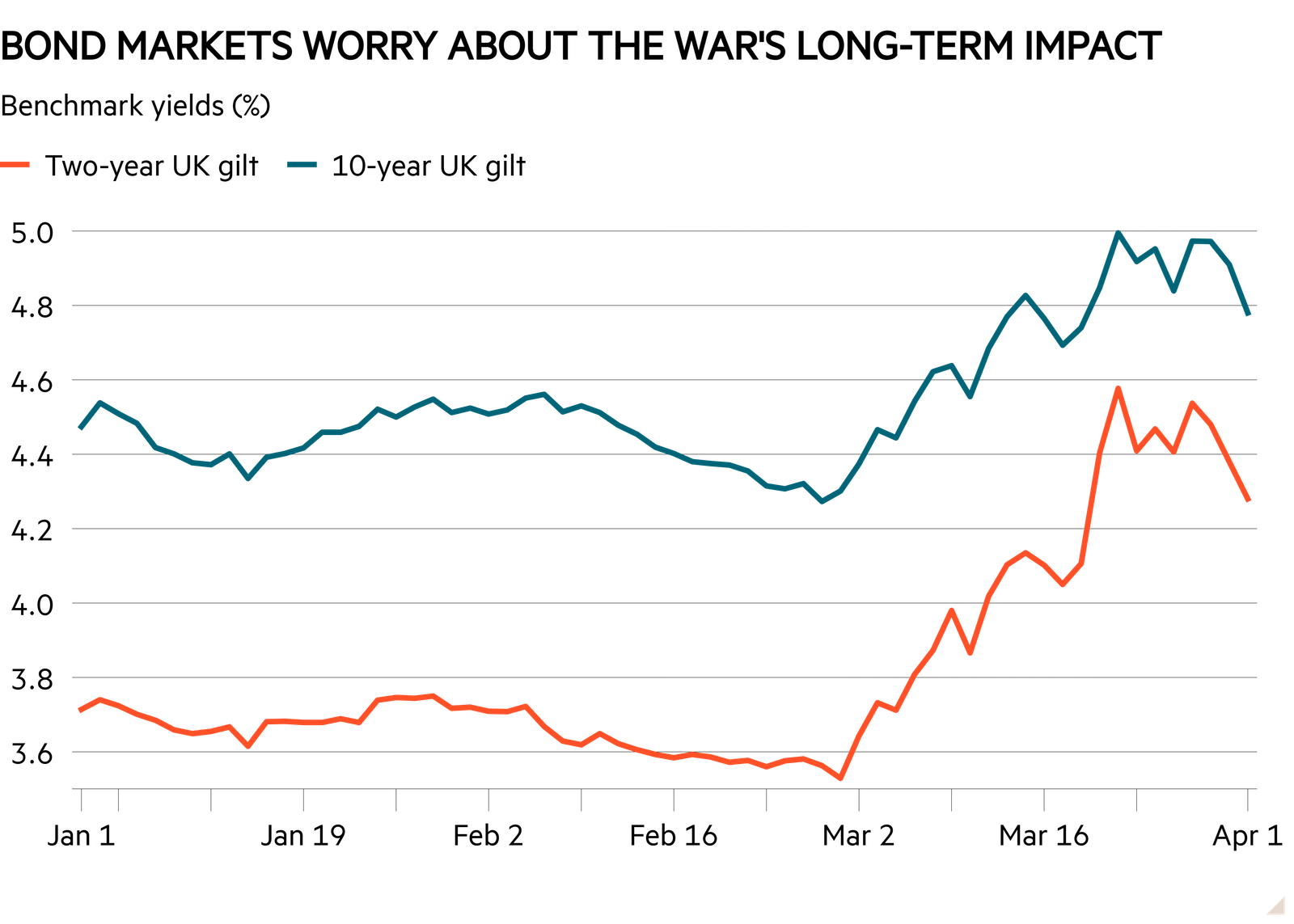

Indeed, bond markets are worrying about the war’s long-term impact, as the below chart indicates.

He adds: “We saw some passive strategies that were holding broad bond benchmarks, which were longer in duration, get caught out during the rate rising environment of 2022.

“Whether we are implementing our view using active or passive funds, the ability to control our duration exposure within our portfolios has been crucial.”

The current geopolitical environment is a challenging time for investors, and traditionally, in such times, investors often revert to ‘risk-off’ assets to look for returns, with bonds seen as a safe or safer haven.

After a prolonged period of low yields and heavy reliance on equities and cash, the rise in interest rates has materially changed the opportunity set for bonds.

Building resilience

According to Darren Ripton, head of MPS at Aberdeen, for a variety of reasons advisers are now having to rethink how they generate sustainable income, manage sequencing risk, and build more resilient portfolios for clients approaching or in retirement.

Fixed interest assets are a key asset class when it comes to constructing balanced portfolios, providing income as well as diversification, which are typically mainstays of long-term retirement investment portfolios.

However, Ripton says he does not think this means fixed interest assets will necessarily provide downside protection in all environments, when risk assets face a challenging time.

“It’s important portfolio constructors are aware of this,” he explains.

“There seems to be a fallacy in some quarters that government bonds are low risk asset classes that provide steady returns over most periods, while in periods of equity market stress, they will provide a defensive offset when equity markets fall.

“There have been some periods over history when this has proved to be the case, but it is very much dependent on the cause of the equity market shock whether fixed interest assets perform this diversifying role.”

Inflation and geopolitical impact

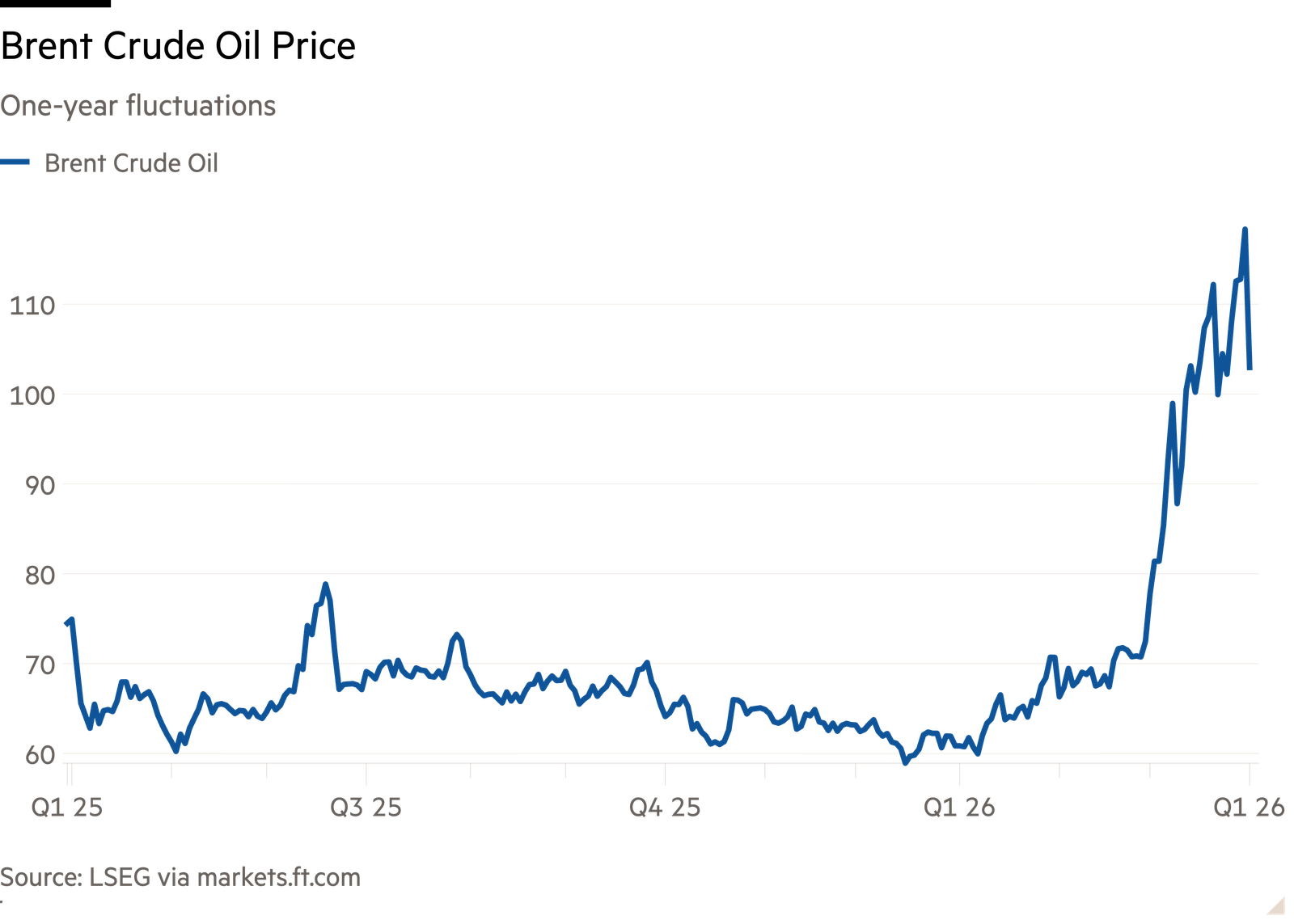

The US/Israel-Iran war has been sending oil and gas prices upwards, and significantly so, as the one-year graph below shows.

Higher energy costs mean higher costs for most goods produced in the global economy.

Higher inflation in the coming months also makes it more difficult for central banks to cut interest rates. In fact, they may have to increase interest rates if inflation remains higher for longer.

Higher inflation also puts upward pressure on bond yields, increasing borrowing costs for consumers, corporates, and governments.

As a result, investment returns for bond investors are likely to be negatively impacted in this environment, says Vincent McEntegart, co-manager of the Aegon Diversified Monthly Income fund.

“Nominal assets like bonds and cash do not provide attractive real returns when inflation is higher, but they can still have a role in dampening overall volatility in multi-asset portfolios.

“Portfolio construction is always easier when bond duration can be called upon to at least partially offset equity downside.

“But these golden periods when bonds and equities offer uncorrelated returns are never permanent and multi-asset funds need to use the flexibilities of their mandates to ensure risk-adjusted returns remain attractive in all market cycles.”

Bond yields, particularly in the UK, have been significantly impacted by the Iran war.

They had already rallied to their lowest yield levels in more than a year on expectations of further Bank of England cuts.

Inflation complacency has unwound

The market had become quite complacent about inflation, but that has now been abruptly reversed, particularly over recent weeks.

At the time of writing, UK two-year yields have risen from 3.52 per cent to 4.17 per cent, five-year yields from 3.68 per cent to 4.35 per cent, and 10-year yields from 4.23 per cent to 4.80 per cent.

Craig Veysey, fixed income lead at Guinness Global Investors, says: “Those are very large moves in a matter of days, and much bigger than we have seen in most other major developed bond markets.

“The UK is especially sensitive to higher energy prices, so a Middle East-driven energy shock feeds much more quickly into inflation concerns here than in the US, for example.

“UK CPI is still running at 3 per cent year-on-year, already above target, so when gas prices surge, the market immediately starts to question how much room the BoE really has to cut.”

Around 50 basis points of cuts that were priced at the end of February have been stripped out, he adds.

The limits of bonds as a safe haven

But Veysey does not believe this is a fiscal crisis or a repeat of the 2022 Truss episode, but rather an inflation repricing story.

He says: “Safe havens do not work in the usual way when bonds have already rallied hard, yields are near their lows, and markets suddenly have to worry about inflation again.”

At these levels, he says gilt yields are becoming attractive again.

There is clearly a risk that energy prices stay higher for longer if the conflict drags on, and central banks are far too early in the process to react.

But he says this still represents a buying opportunity.

Veysey adds: “If yields move further out of proportion to the underlying UK economic data and/or energy prices begin to stabilise, my bias would be to be a buyer of gilts.”

Ima Jackson-Obot is deputy features editor at FT Adviser