Issuance of private catastrophe bonds, or cat bond lites, has now reached $357.6 million in 2024, after two more privately placed insurance-linked securities (ILS) arrangements came to light from the Artex Capital Solutions managed Eclipse Re Ltd. structure. These are now the third and fourth private catastrophe bond issuances from the Eclipse Re platform in 2024.

These are now the third and fourth private catastrophe bond issuances from the Eclipse Re platform in 2024.

Back in January 2024, we revealed the first Eclipse Re private cat bond of the year, a $100 million Eclipse Re Ltd. (Series 2024-1A) issuance.

Then, in May, we reported on a $25 million Eclipse Re Ltd. (Series 2024-2A) deal from the structure.

For comparison, over the course of full-year 2023, the Eclipse Re platform issued just under $210 million of private cat bond notes, solidifying a position as one of the most used structures for these listed private cat bond note issuances. It’s worth remembering though, that giant cat bond fund manager Fermat Capital Management has been known to use Eclipse Re for its private transactions, although we can’t be sure if that manager is the source of the 2024 deals we’ve seen.

Now, building on 2024 issuance for the structure, Eclipse Re Ltd. has issued $9.82 million in Eclipse Re Ltd. (Series 2024-6A) private cat bond notes and $25 million in Eclipse Re Ltd. (Series 2024-7A) private cat bond notes, with each having different terms and maturity dates, Artemis has learned.

Eclipse Re Ltd. is a Bermuda domiciled special purpose insurance (SPI) company and segregated account platform, owned and managed by insurance-linked securities (ILS) market facilitator and service provider Artex Capital Solutions.

Eclipse Re typically acts as a risk transformation vehicle, working on behalf of ILS fund managers and investors, converting collateralized reinsurance or retrocession arrangements into investable notes with features that are more akin to a catastrophe bond, so fully securitized and with secondary transferability as an option.

With these news deals, Eclipse Re Ltd. has issued $9.82 million of Series 2024-6A notes, on behalf of Segregated Account EC66, with these notes having a final maturity date of May 31st 2025.

In addition, Eclipse Re Ltd. has issued $25 million of Series 2024-7A notes, on behalf of Segregated Account EC67, with these notes having a final maturity date of March 31st 2025.

Together, the $38.42 million of Series 2024-6A and Series 2024-7A notes issued by Eclipse Re have been privately placed with qualified investors and admitted for listing on the Bermuda Stock Exchange (BSX) as insurance-linked securities.

As always, with transaction details lacking, we make the assumption that these latest private cat bond deals feature a reinsurance or retrocession transaction that has been transformed utilising the Eclipse Re structure, in order to create and issue a series of investable, securitized catastrophe bond notes, typically for an ILS fund manager or investor portfolio.

We don’t have any details of the underlying trigger or peril(s) for these private catastrophe bond deals, but assume they will be some kind of property catastrophe reinsurance or retrocessional risk.

The proceeds from the sale of the $38.42 million of Series 2024-6A and Series 2024-7A private cat bond notes issued by Eclipse Re will have been used to collateralize the related reinsurance or retrocession contract, held in a trust, enabling the risk transfer and the creation of investable catastrophe-linked securities.

Given the maturity dates of this private cat bonds as for the end of March and May 2025, we suspect these deals represent the securitization of a one year or less duration reinsurance or retrocession arrangement.

With these two new Eclipse Re deals, private catastrophe bond issuance from the structure that has been tracked by Artemis has now reached $163.42 million for 2024, so far.

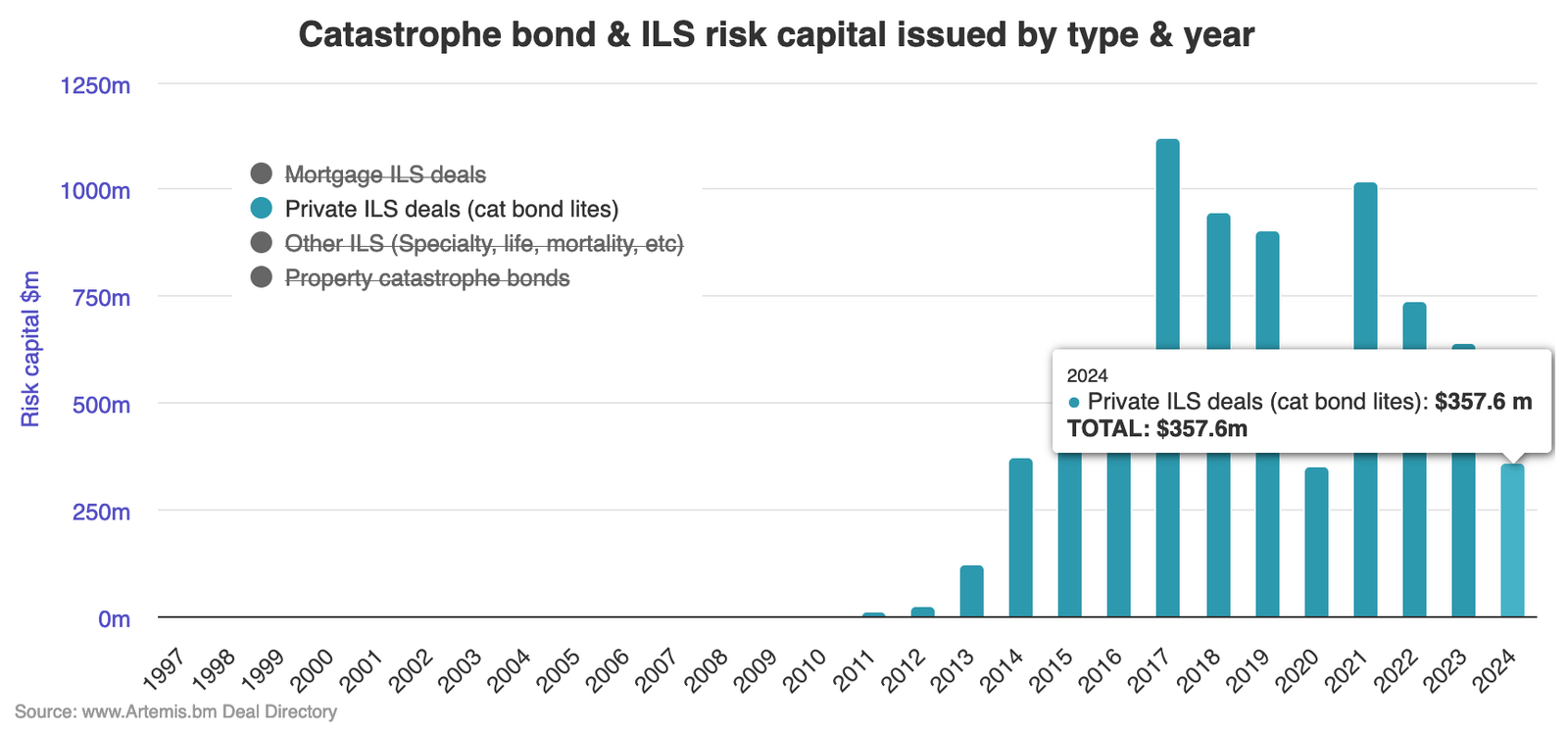

In total, private catastrophe bond issuance across all structures tracked year-to-date by Artemis now stands at $357.6 million.

You can analyse private cat bond issuance by year through accessing this chart, where you can split our tracked catastrophe bond and related ILS issuance by type of arrangement, using the key.

Private cat bonds continue to be a useful structure for the market, that is also supportive of cat bond market growth, helping cedents to try out the market, either at lower-cost, or with fewer investors, while also providing a mechanism for ILS managers to securitize excess-of-loss risks for their funds.

Analyse private catastrophe bond issuance by year using our interactive chart.