-

Building a personalized fixed-income allocation based on risk tolerance and investment time horizon -

Benefits of bond funds versus individual bonds, and criteria for selecting bond funds -

Comparison of short- and intermediate-term bond ETFs and mutual funds

As part of an ongoing series, this column takes a look at the exchange-traded fund (ETF) and mutual fund choices that can help investors build the fixed-income portion of a diversified portfolio. Our March 2026 AAII Journal column covered “Customizing Your Large-Cap Allocation With ETFs and Mutual Funds.”

The AAII Asset Allocation Models offer sample portfolio mixes designed around an investor’s time horizon and tolerance for short-term market swings. Each model combines stocks, bonds and cash to create a diversified allocation strategy, with fixed-income exposure increasing as an investor’s time horizon shortens or risk tolerance becomes more conservative.

Fixed income, and bonds in particular, play an important role by providing income and capital preservation, which help manage risk within an investor’s portfolio. The AAII Asset Allocation Models suggest a 60%, 40% and 10% allocation to fixed income for conservative, moderate and aggressive investors, respectively. The conservative and moderate models use tailored amounts of short- and intermediate-term bonds. The aggressive model includes only intermediate-term bonds.

Short- and Intermediate-Term Characteristics

Short-term bonds typically have low sensitivity to interest rate changes and generally mature within one to five years, making them appropriate for a more conservative fixed-income allocation. Intermediate-term core bonds are designed to provide a balance of income generation, diversification and moderate interest rate exposure through broadly diversified investments in government, corporate and securitized debt. Their maturities typically range from three to 10 years.

Short-term government bonds seek to provide high credit quality, stability and liquidity through investments in short-maturity U.S. government securities. Intermediate government bonds also invest in U.S. government securities but carry greater interest rate sensitivity because of their longer maturities.

Bond Funds Simplify Access to Bonds

Important differences exist between owning individual bonds and investing in an ETF or mutual fund that holds a diversified portfolio of bonds. Individual bonds provide a preset return if you hold them until maturity. Because all cash flows are fixed (assuming no default), you can know exactly how much money you’ll receive and when.

Bond prices are not fixed and do fluctuate. This creates uncertainty in returns for those who sell a bond prior to maturity (or if the bond is callable).

Buying and selling a single bond, or small quantities of bonds, for portfolio rebalancing or other reasons places individual investors at a disadvantage. Individual bonds pay a lump sum at maturity, meaning that the proceeds need to be reinvested. Since bond markets are less transparent than equity markets, it can be difficult for smaller investors to compare prices and assess fair value.

Access to the bond market is simplified when investing with an ETF or mutual fund. Bond ETFs and mutual funds reinvest cash flows on behalf of investors, eliminating the need to select and invest in another bond.

Additionally, bond ETFs and mutual funds hold assets with different maturity dates. So, at any given time, some bonds in the portfolio may provide cash flows through coupon payments. Many bond funds seek to maintain a maturity of a specified length by continually buying and selling bonds to maintain the portfolio’s mandated average maturity.

Criteria Used to Select Fixed-Income Funds

Tables 1 and 2 include bond ETFs and mutual funds, respectively, that might be considered to fulfill the fixed-income portion of one of the AAII Asset Allocation Models.

Mutual funds were required to be identified by Morningstar as true no-load funds and open to new investors. None are classified as adviser, institutional, other, retirement or S class shares. A minimum purchase amount of $5,000 or less applies to all mutual funds. Individual investors must be able to purchase funds directly through a brokerage account. Funds were required to have assets greater than $500 million.

Expense ratios were required to be lower than the category average. ETFs and mutual funds with fees greater than 0.57% were not included. The majority have A+ Investor Grades of A or B for their expense ratios.

Only funds with at least a five-year history were considered. Returns for the one-, three- and five-year periods were required to rank in the range of 40% to 100% within their category, resulting in strong AAII A+ Grades for performance.

ETFs have an average daily trading volume of at least 7,000 shares. Higher trading activity can enhance pricing efficiency and improve liquidity, making it easier for investors to enter and exit positions.

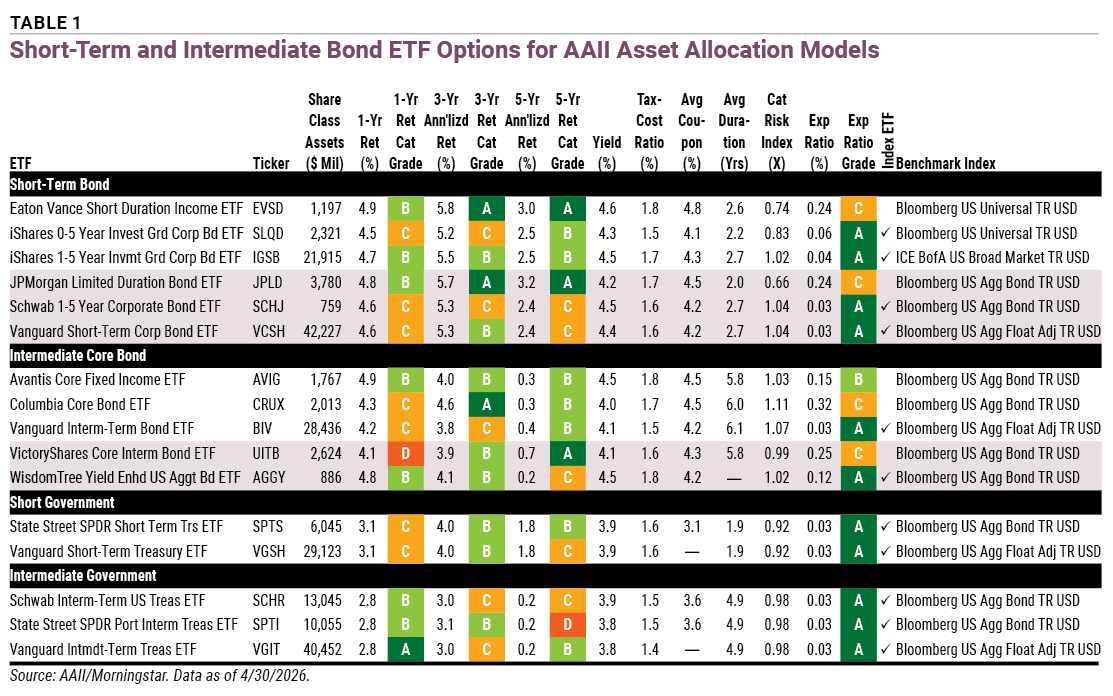

Short-Term and Intermediate Bond ETFs

Table 1 presents ETFs that could be used for a fixed-income allocation. Most of these ETFs are passively managed, with a median expense ratio of 0.04%, compared to 0.32% for the mutual funds in Table 2.

Download the Excel spreadsheet for Table 1.

Short-Term Bond ETFs

The six short-term bond ETFs provide different strategies. Eaton Vance Short Duration Income ETF ![]() (EVSD) and JPMorgan Limited Duration Bond ETF

(EVSD) and JPMorgan Limited Duration Bond ETF ![]() (JPLD) are actively managed. Eaton Vance Short Duration Income seeks to offer an above-average total return over a market cycle of three to five years, whereas JPMorgan Limited Duration Bond seeks to provide a high level of current income consistent with low volatility of principal. Both invest in mortgage-backed and asset-backed securities. Eaton Vance Short Duration Income also incorporates U.S. government securities and corporate bonds.

(JPLD) are actively managed. Eaton Vance Short Duration Income seeks to offer an above-average total return over a market cycle of three to five years, whereas JPMorgan Limited Duration Bond seeks to provide a high level of current income consistent with low volatility of principal. Both invest in mortgage-backed and asset-backed securities. Eaton Vance Short Duration Income also incorporates U.S. government securities and corporate bonds.

Average duration is shown in Table 1. Average duration estimates how much the price of a bond or bond fund is expected to change for a 1% change in interest rates. Bonds with higher durations typically have higher maturities and lower coupons, and they tend to be more sensitive to value changes due to interest rate fluctuations. JPMorgan Limited Duration Bond has lower interest rate sensitivity due to its greater exposure to securitized assets, which often carry lower or more stable duration characteristics due to their structural features.

iShares 0-5 Year Investment Grade Corporate Bond ETF ![]() (SLQD), iShares 1-5 Year Investment Grade Corporate Bond ETF

(SLQD), iShares 1-5 Year Investment Grade Corporate Bond ETF ![]() (IGSB), Schwab 1-5 Year Corporate Bond ETF

(IGSB), Schwab 1-5 Year Corporate Bond ETF ![]() (SCHJ) and Vanguard Short-Term Corporate Bond ETF

(SCHJ) and Vanguard Short-Term Corporate Bond ETF ![]() (VCSH) are passively managed and provide short-duration, investment-grade bond exposure. All track market-weighted corporate bond indexes, where each bond included is based on the size of its outstanding debt. This means that larger issuers have greater influence on the index’s performance. iShares 0-5 Year Investment Grade Corporate Bond includes an extra layer of screening to focus on bonds that trade easily. All invest in foreign debt; iShares 1-5 Year Investment Grade Corporate Bond has the highest percentage allocation at 29.5%.

(VCSH) are passively managed and provide short-duration, investment-grade bond exposure. All track market-weighted corporate bond indexes, where each bond included is based on the size of its outstanding debt. This means that larger issuers have greater influence on the index’s performance. iShares 0-5 Year Investment Grade Corporate Bond includes an extra layer of screening to focus on bonds that trade easily. All invest in foreign debt; iShares 1-5 Year Investment Grade Corporate Bond has the highest percentage allocation at 29.5%.

Intermediate Core Bond ETFs

Avantis Core Fixed Income ETF ![]() (AVIG) has the lowest expense ratio of the actively managed ETFs in Table 1. Its expense ratio is also below the category average of 0.32%. Its research-driven strategy actively adjusts sector weights, security selection and portfolio positioning in an effort to maximize total return. The ETF achieved above-average returns over the one-, three- and five-year periods.

(AVIG) has the lowest expense ratio of the actively managed ETFs in Table 1. Its expense ratio is also below the category average of 0.32%. Its research-driven strategy actively adjusts sector weights, security selection and portfolio positioning in an effort to maximize total return. The ETF achieved above-average returns over the one-, three- and five-year periods.

Vanguard Intermediate-Term Bond ETF ![]() (BIV) tracks the Bloomberg U.S. 5-10 Year Government/Credit Float-Adjusted Bond index, which includes 2,528 bonds. Because holding every bond in the index would be impractical, the ETF uses index sampling to invest in a representative subset of securities designed to closely match the index’s overall characteristics, resulting in a portfolio of 2,303 bonds.

(BIV) tracks the Bloomberg U.S. 5-10 Year Government/Credit Float-Adjusted Bond index, which includes 2,528 bonds. Because holding every bond in the index would be impractical, the ETF uses index sampling to invest in a representative subset of securities designed to closely match the index’s overall characteristics, resulting in a portfolio of 2,303 bonds.

Short and Intermediate Government ETFs

All government ETFs shown in Table 1 are passively managed and have below-average expense ratios (0.03%), as reflected by their grades of A. State Street SPDR Short Term Treasury ETF ![]() (SPTS) and Vanguard Short-Term Treasury ETF

(SPTS) and Vanguard Short-Term Treasury ETF ![]() (VGSH) offer similar strategies and performance for short-term U.S. Treasury bond exposure. Vanguard Short-Term Treasury has nearly five times more in share class assets.

(VGSH) offer similar strategies and performance for short-term U.S. Treasury bond exposure. Vanguard Short-Term Treasury has nearly five times more in share class assets.

Investors can get low credit risk and moderate interest-rate exposure with the three intermediate government ETFs in Table 1. Yields are similar to those of the short government offerings, but average durations of 4.9 years reflect three-to-10-year maturities.

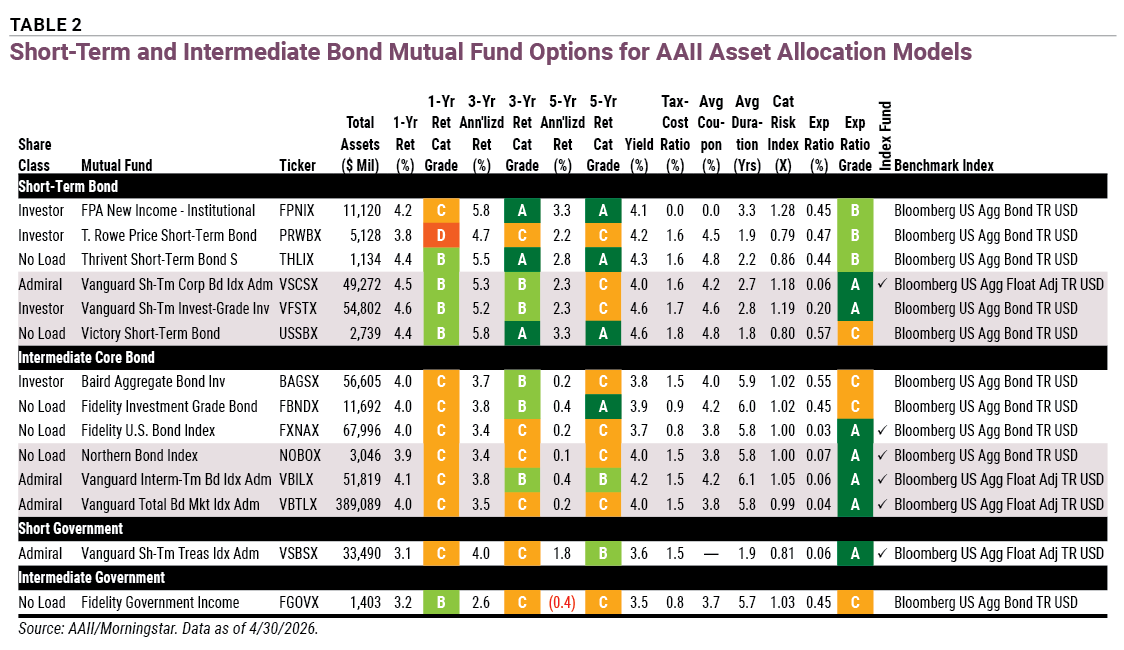

Short-Term and Intermediate Mutual Funds

Table 2 shows mutual funds that could be used for the fixed-income allocation in the AAII Asset Allocation Models.

Download the Excel spreadsheet for Table 2.

Short-Term Bond Mutual Funds

The category risk index included in Tables 1 and 2 relates the volatility of a fund to the average volatility for funds in the same investment category. Values of 1.00 suggest average risk. Values below 1.00 indicate lower risk, and those above 1.00 suggest higher risk. Actively managed mutual funds in Table 2 have the highest category risk indexes. This is attributable to holding investment-grade corporate debt.

Vanguard Short-Term Corporate Bond Index Admiral fund ![]() (VSCSX) is the only short-term bond mutual fund in Table 2 that is passively managed. It has the lowest expense ratio of the short-term bond mutual funds shown at 0.06%. Its ETF counterpart in Table 1 has a cheaper expense ratio of 0.03%.

(VSCSX) is the only short-term bond mutual fund in Table 2 that is passively managed. It has the lowest expense ratio of the short-term bond mutual funds shown at 0.06%. Its ETF counterpart in Table 1 has a cheaper expense ratio of 0.03%.

Vanguard Short-Term Investment-Grade Investor fund ![]() (VFSTX) is actively managed and broadens its holdings to securitized assets and government bonds, whereas Vanguard Short-Term Corporate Bond Index Admiral is mostly focused on corporate bonds.

(VFSTX) is actively managed and broadens its holdings to securitized assets and government bonds, whereas Vanguard Short-Term Corporate Bond Index Admiral is mostly focused on corporate bonds.

Victory Short-Term Bond fund ![]() (USSBX) has the best performance of the short-term bond mutual funds in Table 2 and the highest expense ratio (0.57%) for all mutual funds and ETFs shown. It has one of the highest yields in Table 2 and the highest tax-cost ratio.

(USSBX) has the best performance of the short-term bond mutual funds in Table 2 and the highest expense ratio (0.57%) for all mutual funds and ETFs shown. It has one of the highest yields in Table 2 and the highest tax-cost ratio.

Intermediate Core Bond Mutual Funds

Vanguard Intermediate-Term Bond Index Admiral fund ![]() (VBILX) and Vanguard Total Bond Market Index Admiral fund

(VBILX) and Vanguard Total Bond Market Index Admiral fund ![]() (VBTLX) offer two ways to gain exposure to the intermediate core bond market. Vanguard Total Bond Market Index Admiral invests across nearly the entire U.S. investment-grade bond market, including U.S. Treasurys, mortgage-backed and asset-backed securities, and corporate bonds with short-, intermediate- and long-term maturities. Vanguard Intermediate-Term Bond Index Admiral sticks with intermediate bonds. As a result, it has a slightly higher average duration of 6.1 years and a slightly higher yield than the total bond market fund.

(VBTLX) offer two ways to gain exposure to the intermediate core bond market. Vanguard Total Bond Market Index Admiral invests across nearly the entire U.S. investment-grade bond market, including U.S. Treasurys, mortgage-backed and asset-backed securities, and corporate bonds with short-, intermediate- and long-term maturities. Vanguard Intermediate-Term Bond Index Admiral sticks with intermediate bonds. As a result, it has a slightly higher average duration of 6.1 years and a slightly higher yield than the total bond market fund.

Short and Intermediate Government Mutual Funds

Vanguard Short-Term Treasury Index Admiral fund ![]() (VSBSX) is the mutual fund share class of Vanguard Short-Term Treasury ETF. It has a slightly lower tax-cost ratio, a modestly lower yield and a higher expense ratio than its ETF counterpart.

(VSBSX) is the mutual fund share class of Vanguard Short-Term Treasury ETF. It has a slightly lower tax-cost ratio, a modestly lower yield and a higher expense ratio than its ETF counterpart.

Fidelity Government Income fund ![]() (FGOVX) is actively managed and invests in a broad universe of U.S. Treasury securities, agency debt and mortgage-backed securities issued or guaranteed by government-related entities such as Fannie Mae and Freddie Mac.

(FGOVX) is actively managed and invests in a broad universe of U.S. Treasury securities, agency debt and mortgage-backed securities issued or guaranteed by government-related entities such as Fannie Mae and Freddie Mac.

Final Considerations

Investors can personalize allocations to match their risk profile. Selecting ETFs and mutual funds with varying levels of category risk, duration and yield can help align a portfolio with changing investing goals. Those who become less risk tolerant can shift their focus from maximizing growth to preserving capital.

It’s important to understand the portfolio’s composition and allocations. Beyond the distinction between active and index funds, exposure to foreign bonds and different corporate sectors can create meaningful differences in risk and return profiles. Market-weighted bond indexes function similarly to market-capitalization-weighted equity indexes, with the largest debt issuers exerting the greatest influence on performance and smaller issuers having less impact.