Diving into the deep

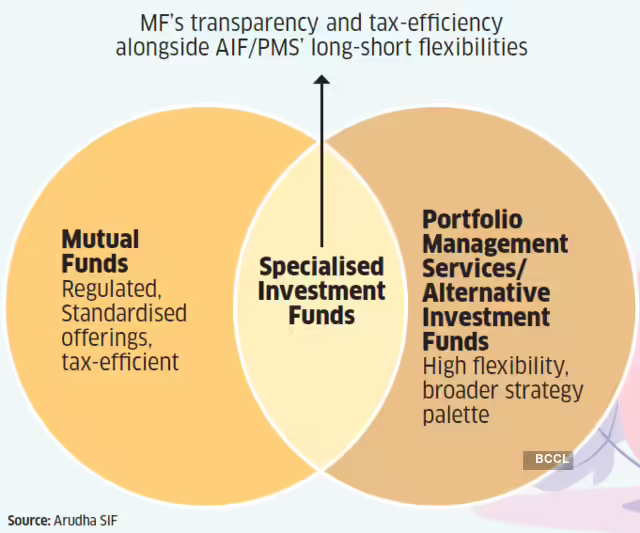

SIFs were launched amid much fanfare last year as a vehicle bridging the gap between mass-market mutual funds and high-ticket Portfolio Management Services (PMS) or Alternate Investment Funds (AIFs). With a ticket size of Rs.10 lakh, SIFs offer flexible investment strategies akin to the latter, while operating within a more tightly supervised, tax-friendly framework.

While mutual funds are restricted to ‘long-only’ strategies, SIFs can pursue both ‘long’ and ‘short’ bets. Unlike traditional mutual funds, SIFs are allowed to sell shares without holding the underlying assets—termed naked short positions—up to 25% of the portfolio. So, asset managers don’t just bet on a rising market; they can also gain from falling stock prices. This allows fund managers to act with conviction instead of simply holding cash. Further, SIFs are permitted to use a wide range of derivative strategies to pursue opportunities across rising, falling and sideways markets. These include covered calls, bear put spreads, short or long straddles, short or long strangles, pair trades and arbitrage, among others.

Theoretically, this flexibility gives SIFs a distinct edge. Ankur Punj, MD and Business Head, Equirus Wealth, says, “Fund managers have the ability to reduce risk in the portfolio and even profit from dislocations on the short side, something long-only equity mutual funds structurally cannot do.” With the market environment turning fragile, these fledgling SIFs must quickly prove they can walk the talk.

Shobhit Mathur, Co-Founder, Ionic Wealth, remarks, “The ongoing correction is an early litmus test for SIFs, and it is precisely in such phases that the flexibility of these strategies becomes relevant.” Punj concurs, “This correction is effectively an early live ‘stress test’ of SIF long-short designs. Fund managers should be able to use market volatility and show alpha generation through their funds at this time.”

Heightened volatility creates ripe conditions for deploying clever derivative strategies that are not permitted within the traditional mutual fund framework. Nilesh Mishra, Senior Financial Advisor at 1 Finance, insists, “The current correction is creating exactly the raw material longshort funds need: high dispersion, clear sector winners and losers, and valuation gaps widening between quality and weak stocks.”

SIFs have made their mark amid testing conditions

Varied outcomes

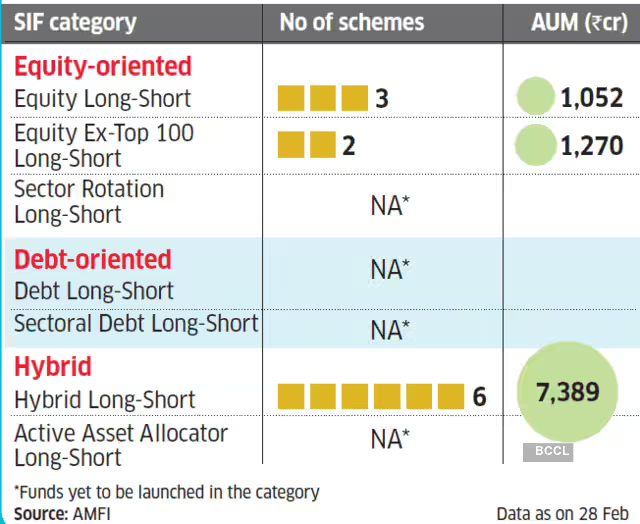

The SIF basket is growing rapidly. The SIF universe now comprises eight asset managers, with 11 schemes (a few more in the pipeline) managing around Rs.9,700 crore in assets as of 28 February, shows data from Amfi (Association of Mutual Funds in India). Hybrid long-short funds have seen the most action, with six funds accounting for about 76% of total SIF AUM. Three equity long-short funds and two equity ex-top 100 long-short funds are also active.

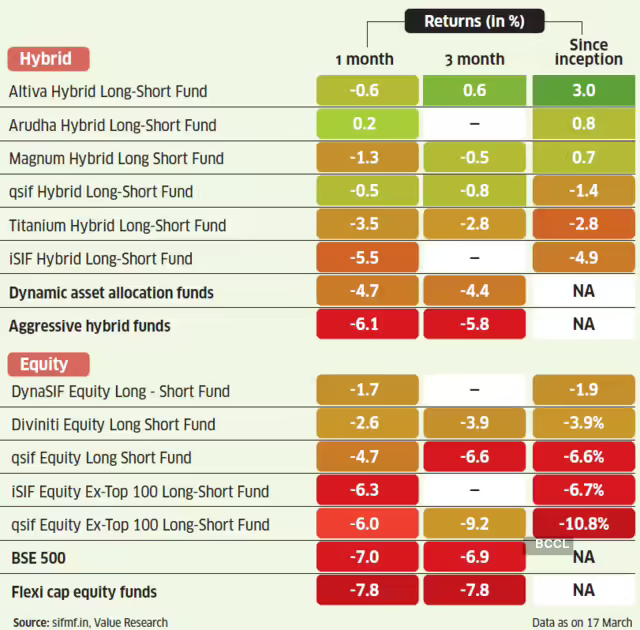

Asset managers are following distinct playbooks in their SIF strategies. With funds harnessing different levers at their disposal, the outcomes are also varied. Equity-oriented SIFs target equity-like returns while keeping volatility akin to that of hybrid funds. Equity long-short funds are flexi-cap, equity-oriented funds that complement arbitrage and short strategies. Meanwhile, ex-top 100 equity long-short funds focus on mid- and small-cap stocks. “This strategy offers a defensive way to invest in the broader market, seeking to participate in the upside while minimising the downside and volatility associated with the segment,” points out Chintan Haria, Principal-Investment Strategy at ICICI Prudential Mutual Fund. These funds have exhibited a range of outcomes. While Diviniti Equity Long Short Fund (from ITI Mutual Fund) has shed 3.86% in the past three months (compared to the BSE 500 index’s 6.9% fall), qsif Equity Ex-Top Comparatively, dynamic asset allocation funds have lost 4.4%, while aggressive hybrid funds have fallen 5.8%. Mathur observes, “SIFs are beginning to demonstrate the benefits of a flexible mandate in a volatile market environment. Hybrid long-short strategies have shown relative resilience during the recent correction.” He points out that many hybrid SIFs are running selective short positions of around 3-7% while maintaining a net equity exposure of 30-50%, even as equity long-short SIFs are taking 13-20% tactical shorts to navigate turbulence. Manuj Jain, Cofounder ValueMetrics Technologies, maintains, “While regulations allow unhedged short exposure of up to 25% of the portfolio, most recently launched SIFs are unlikely to operate at that limit initially.”

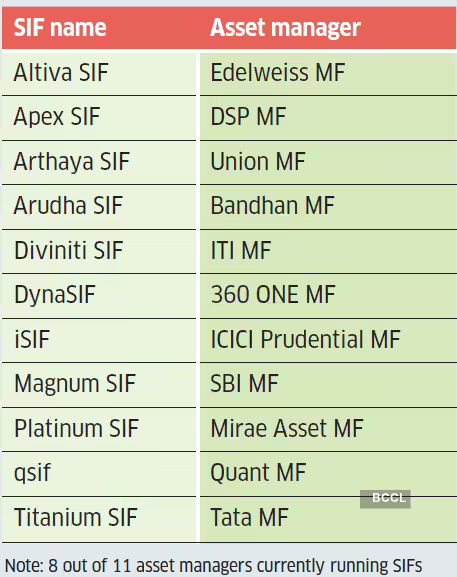

Further, hybrid long-short funds, which invest across equity and fixed income, seek to reduce drawdowns during bear or sideways markets. Asset managers deploy various approaches here—covering distinct strategies such as an income-plus arbitrage fund, a balanced advantage fund, and an equity savings fund. Altiva Hybrid Long-Short Fund has so far outperformed in this space, gaining 0.55% in the past three months and 2.95% since inception. It is aimed at income-oriented investors seeking slightly better returns than arbitrage funds. It avoids naked shorts and limits derivatives usage to covered calls and pair trades. Bhavesh Jain, Co-Head, Factor Investing, Edelweiss Mutual Fund, says, “We take limited equity exposure through calls and some derivative strategies, focusing more on arbitrage and fixed income as core strategies along with special situation trades.”

iSIF Hybrid Long-Short Fund adopts a dynamic asset allocation strategy with net equity ranging from -7.5% to 75% and unhedged shorts capped at 10%. Meanwhile, Arudha Hybrid Long-Short (from Bandhan Mutual Fund) follows a market-neutral strategy, with full hedged equity positions capturing opportunities arising from pricing inefficiencies and spreads, rather than taking directional market exposure.

SIF assets are growing rapidly

.jpg)

Hybrid long-short funds currently dominate SIF assets

The SIF platter

Verdict awaited

These are still early days for SIFs. While initial performance provides some idea of their capabilities, it would be wrong to judge them purely on this limited track record. The real prowess of SIF will be evident over a market cycle. Jain of ValueMetrics says, “Over time, the true test will be whether these strategies can consistently reduce drawdowns during market corrections while still participating in the upside phases.”

Experts insist that SIFs are a different breed—their flexibility holds promise, but execution remains key. To be sure, investors cannot extrapolate asset managers’ SIF execution capabilities from their prowess in mutual funds. Jain says, “Managing longshort strategies requires a very different skill set compared to traditional long-only portfolios. Robust risk management frameworks will be critical, given the use of derivatives and short positions in these strategies.”

Mishra adds, “Most AMCs launching SIFs built their reputation in long-only portfolios, a fundamentally different skill from running a disciplined short book. Until we see a full market cycle, it is hard to separate genuine long-short expertise from rebranded equity funds with occasional derivative overlays.” He suggests checking the SIF average short exposure in monthly factsheets. “If it consistently stays below 10%, it is a long-only fund in SIF clothing,” says Mishra.

Given the disparate outcomes in both returns and volatility, investors must evaluate options carefully. Punj of Equirus Wealth maintains, “Since the track records are nascent, it is important not to look at returns and rather focus on risk metrics amid the correction. Hybrids show promise for shallower drawdowns via debt/arbitrage anchors, while equity longshort funds may exhibit higher volatility but potential alpha in dispersion phases.” Some experts are convinced that SIFs will gradually play a larger role in investors’ portfolios. Ionic Wealth’s Mathur insists, “Hybrid SIFs can act as core portfolio anchors while equity long-short SIFs can help navigate market cycles more effectively. As investors increasingly seek risk-adjusted returns rather than just directional exposure, SIFs are likely to see greater adoption in the coming years.”

However, SIFs will have to earn their stripes, and the current market represents the first hurdle. Mishra of 1 Finance contends, “The role SIFs play depends entirely on whether fund managers consistently use the derivatives toolkit they were handed, and whether the first real recovery cycle proves that long-short actually delivers better risk-adjusted returns than a simple index fund.”

If it does, SIFs will reshape how India’s emerging wealthy class thinks about equity investing. If it doesn’t, SIFs risk becoming another well-intentioned product that sounded better in the Securities and Exchange Board of India (Sebi) circular than in the investor’s portfolio, Mishra adds.