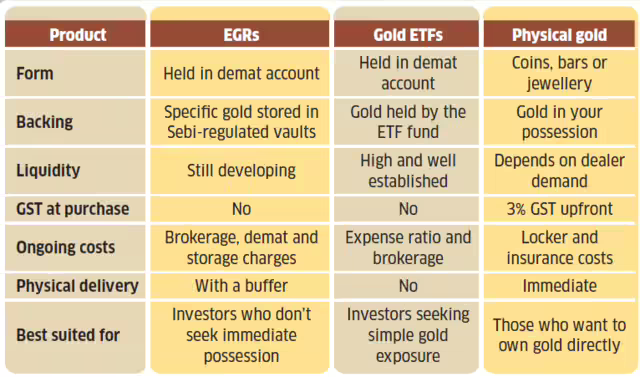

What format of gold best suits you

How EGRs work

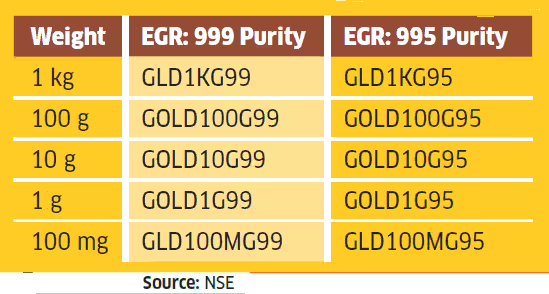

An EGR is a digital certificate backed by actual physical gold stored in a Securities and Exchange Board of India (Sebi)-regulated vault. The receipt is held in your demat account, like a share or ETF. You can buy EGRs in denominations of either 0.1 gram (i.e. 100 mg), 1 g, 10 g, 100 g and 1 kg.

“If you buy EGRs equivalent to 1 g, you become the beneficial owner of one gram of gold of minimum 999.5 purity stored in an accredited vault. You can buy and sell these receipts on the BSE and NSE during market hours,” says Shweta Rajani, Head—Mutual funds, Anand Rathi Wealth.

ALSO READ | Big shift in gold ETFs: Are funds moving away from physical gold? Is ‘paper gold’ the future or a risk?

Unlike with gold ETFs, if you later want the gold itself, you can redeem the EGR and take physical delivery in the form of a bar or coin by paying applicable charges and 3% GST.

Denominations and contract sizes

Investors can buy EGRs in denominations ranging from 100 milligrams to 1kilogram, with contracts available in both 99.5% and 99.9% purity variants.

Years in the making

“It was only in May 2026 that NSE launched EGR trading on its platform, potentially giving the product greater visibility and reach,” adds Rajan.

Harish Sharma, Associate Director, Sanctum Wealth, says EGRs took years to reach Indian bourses because they required building “an entirely new market framework around gold”.

The first challenge was regulatory. Gold had to be treated not just as a commodity, but a financial security that could be held in one’s demat account and traded on stock exchanges. This required Sebi to create new rules for vault managers, bourses and depositories such as the National Securities Depository Limited (NSDL) and Central Depository Services Limited (CDSL).

The second was operational. “Vault managers had to be registered and monitored, purity standards had to be standardised, and systems had to be built to ensure that every receipt was backed by a corresponding quantity of gold,” explains Sharma.

ALSO READ | Why some global ETFs in India are wildly overpriced and the risks investors don’t realise they’re taking

The third hurdle was technological. Depositories needed to integrate the receipts into their demat infrastructure so they could be held and transferred like securities. Even after the infrastructure was ready, adequate investor interest remained a major concern.

Rajani notes that “gold is seen as a very personal asset in India,” and many investors still prefer to buy it directly from jewellers. At the same time, investors who simply want exposure to gold “already had a clear route through Gold ETFs,” she adds. That left EGRs occupying a narrow middle ground.

Sharma says jewellers, refiners and brokers were initially cautious about shifting from the traditional over-the-counter bullion market to an exchange-based model. Without sufficient participation and market makers, trading volumes were expected to remain thin. That remains one of the biggest challenges even today. EGRs still have lower trading volumes and wider bid-ask spreads—difference between the price buyers are willing to pay and the price sellers are asking—which can make them trade at a slight premium compared to spot gold. As liquidity improves, such deviations are expected to narrow.

Costs and limitations

One of the major benefits of EGRs is their purchase via the exchange does not attract 3% Goods and Services Tax (GST), unlike direct purchases of physical gold. “However, investors still incur brokerage, exchange and demat charges. Vaulting and storage fees may also apply depending on how long you hold the receipts,” says Rajani.

If you convert your EGRs into physical gold, you have to pay withdrawal and delivery charges along with 3% GST on the value of the gold at the time of redemption. You also incur storage charges and must rely on vault managers to safeguard the gold, reconcile physical holdings with electronic records, and process withdrawal requests. While Sebi’s rules reduce these risks, the system still depends on the operational efficiency and financial soundness of vault managers.

Another practical limitation is that physical delivery is not immediate. Investors must submit a withdrawal request through their broker, after which the vault manager arranges delivery. Since exchanges and brokers do not specify a standard timeline, receiving the gold may take several days depending on operational procedures and the location of the vault. Availability is also an issue as not all brokers offer EGR trading.

Taxation

EGRs are treated as listed securities for tax purposes. “If you sell them within 12 months, any profit is treated as a short-term capital gain and taxed at your applicable income tax slab rate. If you hold them for over 12 months, the gains qualify as long-term capital gains and are taxed at 12.5% without indexation,” explains Rajesh H. Gandhi, Partner, Deloitte India. Converting EGRs into physical gold, or depositing physical gold to create EGRs, is not regarded as a transfer for capital gains tax purposes. As a result, this conversion does not trigger any capital gains tax.

Do EGRs fill a real gap?

EGRs bring regulation, transparency and standardisation to a market that has historically been fragmented and opaque. They are useful for investors keen on digital gold. Unlike many app-based digital gold products that operate outside Sebi’s regulatory framework, EGRs are exchange-traded and backed by gold stored in Sebi-regulated vaults.

They also bridge a gap between gold ETFs and physical gold. Like gold ETFs, they can be bought and sold through a demat account during market hours. But unlike ETFs, they can be converted into physical bars or coins if you later want to take delivery. That said, whether they become widely adopted will depend on how quickly liquidity improves and whether investors see enough added value to justify storage charges and other costs. For those who only want exposure to gold prices, gold ETFs may still remain the simpler and more cost-effective option.