")

ridvan_celik

Many of you here on Seeking Alpha know me as a REIT analyst.

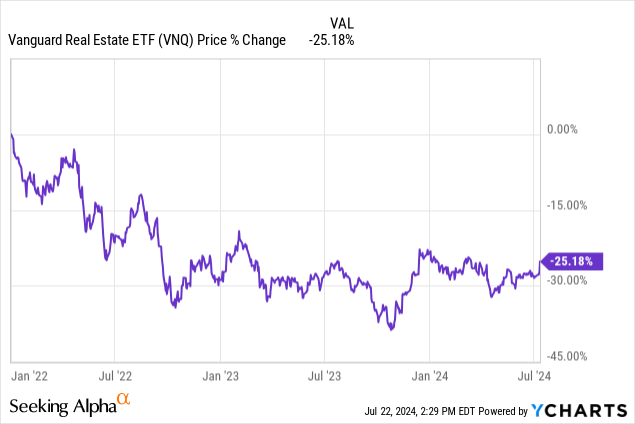

REITs (VNQ) are my specialty, and I invest heavily in them because they are today priced at historically low valuations and essentially allow you to buy high-quality, professionally managed real estate at a heavily discounted price.

But just because I’m bullish on REITs does not mean that I invest all of my capital into them.

The only free lunch in the capital markets is diversification, and you never want to be fully exposed to a single sector as it could become the victim of a black swan. A great example of that is the recent surge in interest rates and the two-year-long REIT bear market that followed…

For this reason, I invest about 50% of my portfolio outside of the REIT sector, and right now, my biggest non-REIT investment is an asset management company called Patria Investments Limited (NASDAQ:PAX).

I have accumulated a lot more of it lately, and it has become one of my largest holdings in my entire portfolio, even larger than some of my biggest REIT investments.

Here’s my investment thesis:

Alternative Asset Management Is A Great Business

Let us start with some basics.

Asset management companies are in the business of offering investment services in exchange for fees.

Most often, they will manage various investment funds, and investors will pay fees to the manager for taking care of these investments.

However, not all asset management businesses are created equal.

The company’s profitability is heavily dependent on the ability to grow assets under management and pricing power in terms of the fees it can charge investors.

With that in mind, asset management businesses that focus on alternative investments like private equity, infrastructure, and credit are especially interesting because they enjoy rapidly growing demand from investors and high pricing power.

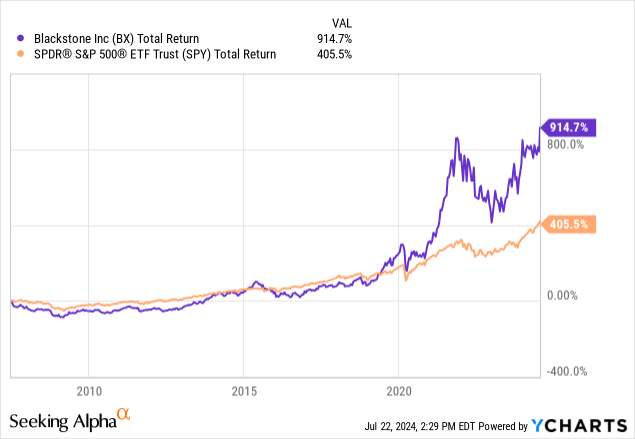

Blackstone Inc. (BX) is the biggest company in its space, and just look at its historic performance relative to the S&P 500 (SPY):

Its investors have earned huge returns over the years because it has been able to rapidly grow its assets under management and charge relatively high fees. The future looks bright.

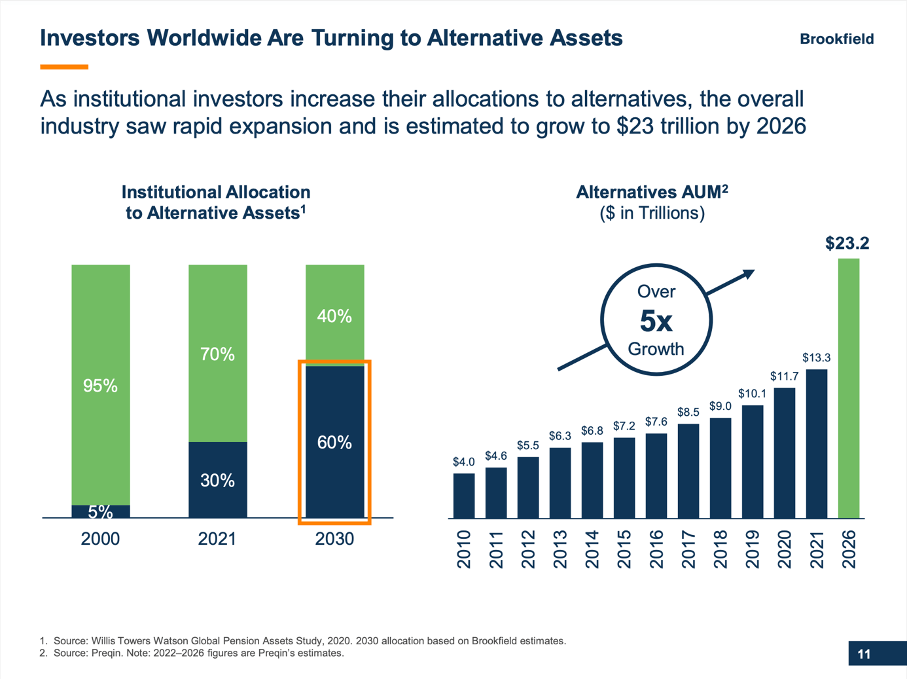

Today, investors are allocating increasingly large portions of their portfolios to alternative investments to diversify away from stocks and bonds. Brookfield Asset Management Ltd. (BAM) predicts that allocations to alternatives will grow from 30% today to over 60% by the end of this decade. This represents trillions of capital, and it provides a great opportunity for the leading asset managers to grow their assets under management. Moreover, since most of these investments are private and illiquid, the fee income is very sticky. Unlike stocks and bonds, which can be sold in a few clicks, investors cannot easily move in and out of alternative investments, and this is a great advantage for these asset managers as it results in more consistent and predictable fee income for them.

Brookfield Asset Management

Also, because these are complex investments that require unique skills and relationships, the leading asset managers with great track records are able to charge relatively high fees, often including an asset management fee, but also incentive fees, acquisitions fees, disposition fees, etc. This is different from the asset management businesses that focus on public equities, which have become far more competitive and lost in pricing power. Think of BlackRock, Inc. (BLK) and Vanguard and their extremely low fees: Investors are willing to pay a premium to invest with the leading alternative asset managers because the higher fee is well worth it.

Unfortunately for investors, this is already well reflected in the valuations of most alternative asset managers. The market knows that they’re expected to grow at a rapid pace in the coming years, and it has priced them accordingly.

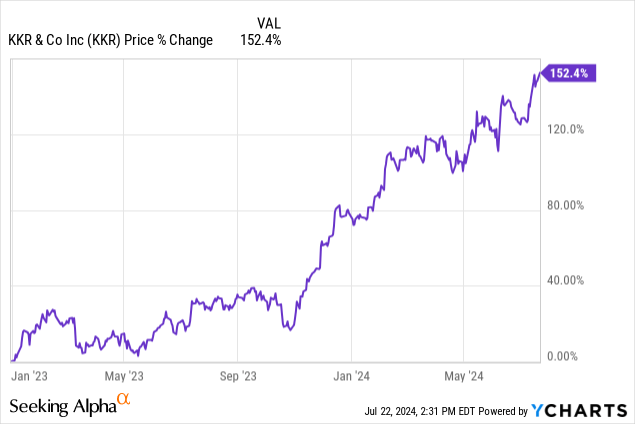

I invested in KKR & Co. Inc. (KKR) in early 2023, and it has more than doubled in value since then:

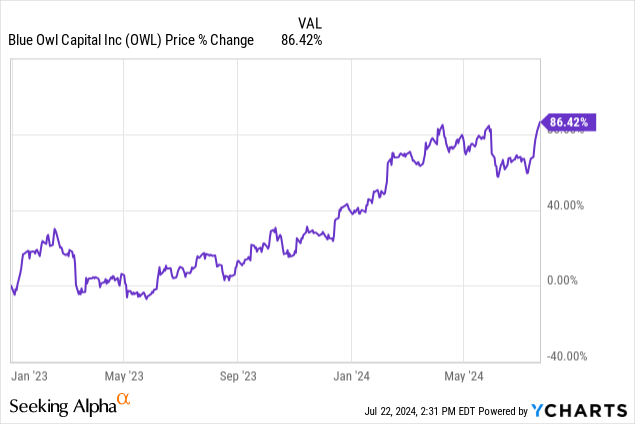

Around the same time, I also heavily invested in Blue Owl Capital Inc. (OWL), and it’s also up 85%:

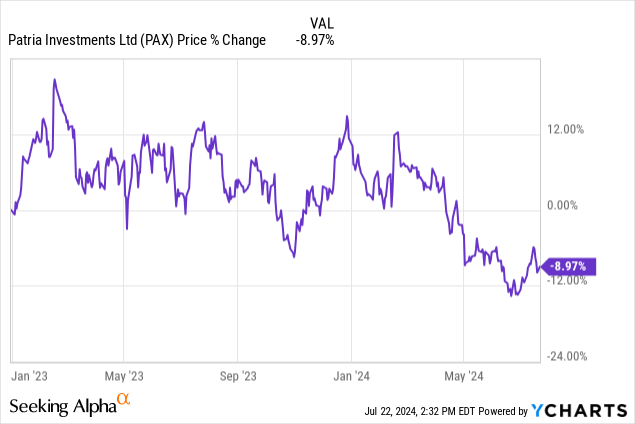

But one opportunity remains, and it’s Patria Investments. Its share price has slightly declined even as its close peers surged in value:

This would lead you to think Patria is struggling or facing headwinds, but this isn’t the case at all.

On the contrary, it has grown even faster than most of its peers.

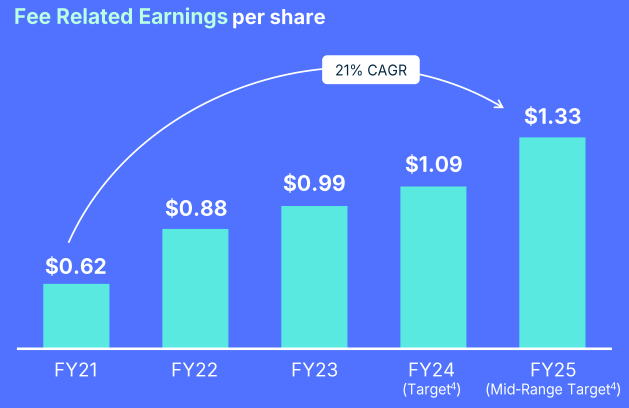

It has managed to grow its fee-related earnings per share by 21% annually since it went public, and that’s despite distributing 85% of its distributable income in dividends to shareholders:

Patria Investments

As a result of this rapid growth and its stagnating share price, the company has now become deeply undervalued.

With a $12 share price, it would seem that the company is priced at 9x its forward FRE, but it’s actually even cheaper than that because it also has $2.87 of net accrued performance fees that are yet to be realized.

If you deduct that from its current share price, it then trades at just 7x its FRE, which is an incredibly low valuation for such a rapidly growing asset management company. How many companies do you know that trade at a single-digit multiple of their cash flow despite growing at 20%-plus annually?

But is it so cheap then?

I think it’s because it specializes in Latin American markets, and they’re today out of favor.

But I actually view this as an advantage because I expect allocations to alternatives in Latin America to grow substantially over the coming decade because of:

- The trend of nearshoring.

- The growing geopolitical tensions.

- The untapped opportunities in the region.

- The low valuations.

- The uncorrelated returns.

Despite that, this is a less competitive market with fewer well-established asset management companies, and therefore, I think that Patria is ideally positioned to capture a large share of this growth.

It’s known as the “Blackstone of Latin America” because it used to work closely with Blackstone, and they even owned a chunk of Patria at one point. This gives it a lot of credibility with international investors, and today, it’s the leader with $40 billion of assets under management, a multi-decade track record, and an amazing reputation.

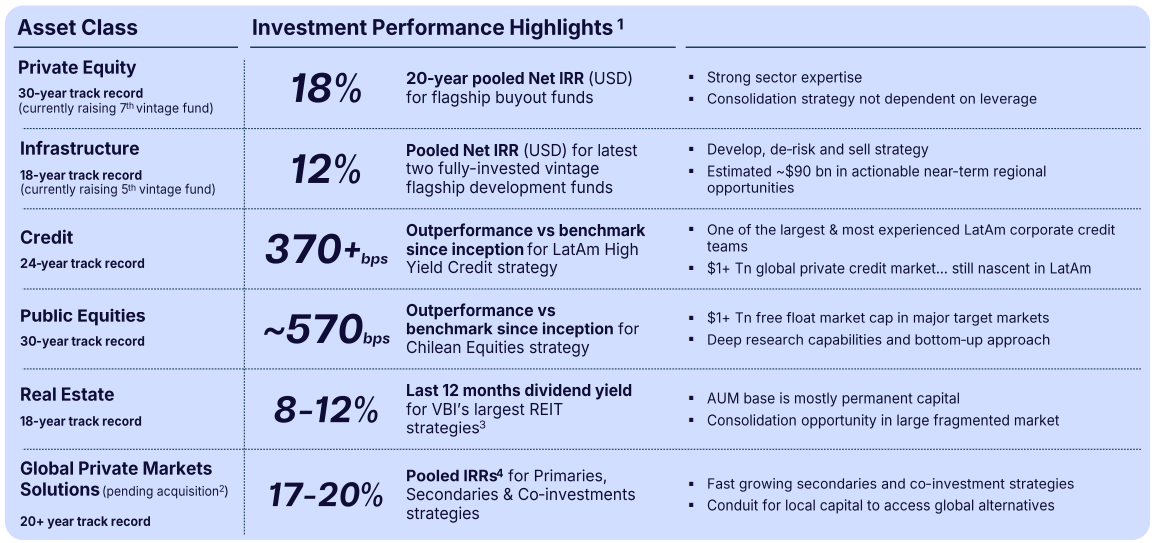

Here’s how its various funds have performed over the long run:

Patria Investments

It focuses mainly on private equity, and its funds have easily beaten their benchmarks:

Patria Investments

Something that the market appears to have missed is that Patria has recently acquired two REIT managers, and as a result, it has now become the largest REIT asset management company in Brazil.

This is very good news because the business of managing REITs can be very rewarding. The capital is permanent, and the fees are very consistent.

The REIT management business is one of the main reasons why Blackstone has been so incredibly rewarding to its shareholders, and Patria is now replicating it in Latin America:

Patria Investments

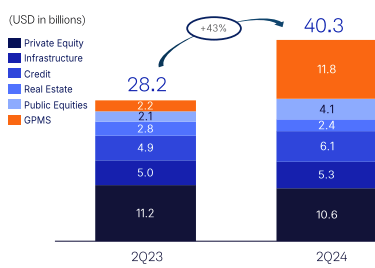

Therefore, I expect its assets under management to continue to grow at a rapid pace over the coming years. It has grown by 40% annually since it went public, and the company is still in its early days as it manages 30x less capital than Blackstone and it focuses on a massive market with relatively little competition:

Patria Investments Patria Investments

And the amazing thing about these asset management businesses is that they’re capital-light.

Patria can achieve this rapid growth without having to invest much if any additional capital. For this reason, they have very little debt, and the management even expects the company to be debt-free by the end of this year. Moreover, they can distribute substantially all of their profits in the form of dividends to its shareholders. At its current share price, this is expected to result in a 6%-8% dividend yield, and there are also zero withholding taxes because they are structured in the Cayman Islands.

Risks

Latin America is a riskier region of the world. There’s more crime, corruption, and political risk. The local economies and currencies are also more volatile and exposed to commodity prices.

However, Patria does a good job of mitigating these risks.

It only invests in Latin American countries with long histories of respecting private capital and have established trustworthy institutions. Therefore, they have no exposure to Venezuela or Argentina.

Moreover, Patria actually earns the majority of its fees in USD, EUR, and GBP. Therefore, it’s not that heavily exposed to the local currency risk.

Bottom Line

I think that Patria has one of the best asset management businesses in its peer group because it focuses on a region with rapidly growing demand and limited competition, and this gives it strong pricing power and should result in rapid AUM growth.

Historically, it has grown its fee-related earnings per share by 20% per year. We expect that to continue, but despite that, it is today priced at just 7x its fee-related earnings net of accrued performance fees.

The company will soon be fully debt-free, and it pays a high yield.

What more could you ask for?

How I see it is that Patria offers an amazing combination of yield, growth, value, and safety. Finally, it also provides valuable diversification benefits to my portfolio, which is heavily exposed to North America and Europe.

This is why I have been accumulating so much of it lately.