The game industry’s motto for all of last year was “survive til 2025.” And in some respects, that wasn’t just wishful thinking.

As the industry trudged through 2024, market researcher DDM saw positive signs. And with one quarter of 2025 in the books, it certainly seems that things are trending in the right direction when it comes to game deals — investments or M&A.

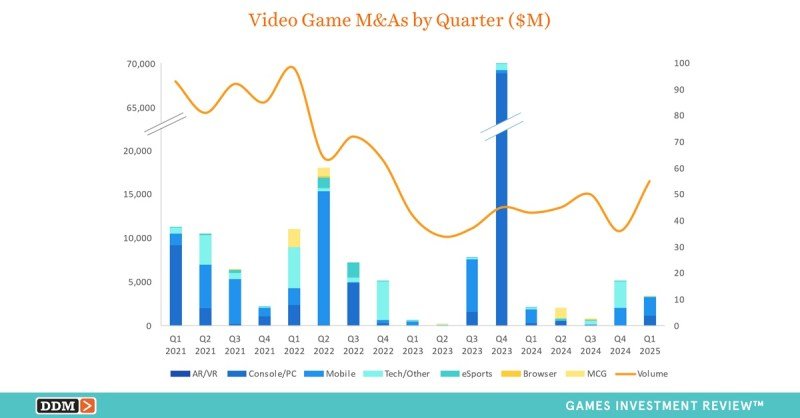

Q1 2025 not only marks the second consecutive quarter of growth, but it is the largest quarter since Q4 2023, with combined games investments and M&As totaling $7.8 billion across 245 transactions (+29% in value and +1% in volume compared to Q4’s $6.0B across 243 combined investments and M&As).

Q1 2025 overview

Q1 2025 investments saw a significant increase in value, totaling $4.4 billion across 190 investments (+370% in value and -8% in volume compared to Q4’s $945.9 million across 207 investments) recording 4.7 times in value growth QoQ and the largest quarter since Q2 2022.

Q1 2025 M&As saw a sizable decline in value, totaling $3.3 billion across 55 transactions (-34% in value and +53% in volume compared to Q4’s $5.1 billion across 36 transactions), despite having the largest quarterly volume since Q4 2022. That was largely driven by 44 undisclosed M&As (80% of total volume and 13% above the quarterly average of 67%).

And the quarter saw a major surge in new fund announcements, totaling $21.8 billion across 43 funds (+122% in value and +13% in volume compared to Q4’s $9.8 billion across 38 funds), marking the largest quarter since Q2 2022; this 2.2 times QoQ value growth was driven by five funds collectively raising over $14.3 bilion (65% of the capital raised).

Mitchell Reavis, DDM games investment review director, said in a statement, “There’s no doubt that ‘survive til 2025’ became a defining mantra for the games industry during recent turbulent years. While DDM anticipates ongoing layoffs, strategic pivots, and the divestiture of non-core business offerings throughout 2025, the data reveals genuine signs of recovery with investment and M&A trends moving in the right direction.”

Summary of investments

Q1 2025 investments totaled $4.4 billion across 190 investments (+370% in value and -8% in volume compared to Q4’s $945.9 million across 207 investments) achieving a 4.7 times in value growth QoQ and the highest value since Q2 2022 of $6.1 billion; this achievement can be attributed to Infinite Reality’s $3.0 billion mid/late-staged investment from Sterling Select (67% of the quarter’s value).

The firm said Q1 2025 game developer investments totaled $4.0 billion across 103 investments (+457% in value and -27% in volume compared to Q4’s $720.0 million across 141 investments).

Artificial intelligence and blockchain continue to receive ongoing investor enthusiasm as game industry artificial intelligence investments totaled $3.1 billion across 32 investments (+2,288% in value and +14% in volume compared to Q3’s $130.8 million across 28 investments) and games industry blockchain investments totaled $372.2 million across 28 investments (+74% in value and -50% in volume compared to Q4’s $214.5 million across 56 investments).

The highest segment by value was led by Tech/Other (86%), followed by Console/PC (8%), Mobile (5%), MCG* (1%), eSports (<1%), AR/VR (<1%) and Browser (<1%).

And Q1 2025’s undisclosed investments totaled 93 investments (49% of the quarter); using historical averages to estimate the undisclosed investment values, Q1 2025 reached $4.9 billion [+/- $179.1 million].

M&As

The quarter’s M&As totaled $3.3B across 55 transactions (-34% in value and +53% in volume compared to Q4’s $5.1B million across 36 transactions) achieving the highest quarterly volume since Q4 2022 of 63 transactions; the sizable decline in value is a result of undisclosed M&As totaled 44 transactions (80% the total volume or +13% above the quarterly average of 67%).

Q1 2025 game developer M&As totaled $2.1 billion across 26 transactions (+7% in value and +53% in volume compared to Q4’s $2.0 billion across 17 transactions).

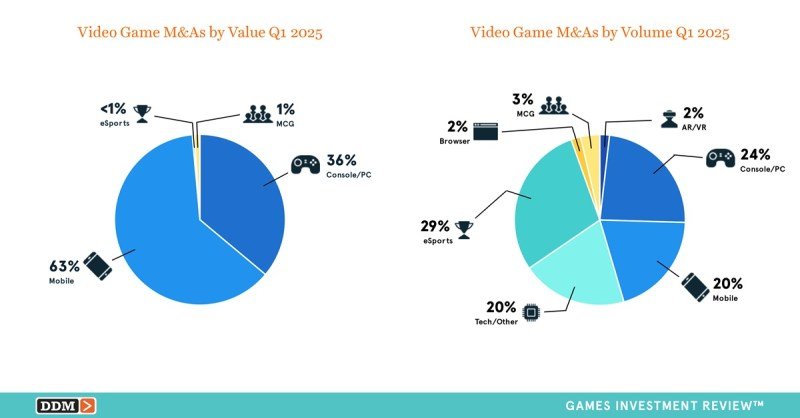

The highest M&A segment by value was led by mobile (63%), followed by console/PC (36%), MCG* (1%), and esports (<1%).

Asia, Europe, and North America led M&A activity by both value and volume with Asia totaling for $1.3 billion over seven transactions (38% of the value and 13% of the volume) and Europe totaling $1.2 billion across 22 transactions (37% of the value and 40% of the volume); North America contributed 38% of the total transaction volume however, deal values were not disclosed.

Exits (M&A + IPOs)

Q1 2025 Exits (M&As + IPO) totaled $5.6 billion across 56 transactions (+10% in value and +44% in volume compared to Q4’s $5.1 billion in value and 39 in volume) marking the largest quarter by volume since Q2 2022’s 67 transactions and a full-year of increased value dating back to Q1 2024 of $5.2 million.

Grand Centrex’s SPAC reverse merger is the first such transaction since Semper Fortis Esports’ $15.9 million deal in Q4 2023.

The first quarter’s sole IPO had a market capitalization of $2.2 billion (+14,038% in value and -67% in volume compared to Q4’s $15.9 million in combined market capitalization across 3 IPOs).

The highest exit (M&A + IPOs) by segment value was led by tech/other (40%), followed by mobile (37%), console/PC (22%), MCG* (1%), and esports (<1%).

Fund Announcements

[Note: DDM tracks announcements from venture capital firms and funds on the new capital they raise that eventually become deployed in the investments in its reports].

The first quarter’s new fund announcements totaled $21.8 billion across 43 funds (+122% in value and +13% in volume compared to Q4’s $9.8 billion across 38 funds) marking the largest quarter for fund announcements since Q2 2022 of $25.1 billion across 40 funds; this 2.2 times QoQ value growth was driven by five funds collectively raising over $14.3 billion (65% of the capital raised): Bank of China ($6.9 billion), Khosla Ventures ($3.5 billion), Thoma Bravo ($1.9 billion), Haun Ventures ($1.0 billion), and the Government of India ($1.0B).

Worth noting: Not all of that capital is going to be invested in games. Artificial intelligence and blockchain are still drawing significant interest from venture capital firms as funds targeting AI totaled $5.2 billion across 15 funds (+128% in value and +15% in volume compared to Q4’s $2.3 billion across 13 funds) and blockchain totaled $2.1B across 8 funds (+22% in value and -43% in volume compared to Q4’s $1.7 billion across 14 funds).

Funds that were solely focused on early-staged companies dominated in value and volume raising $10.9 billion across 28 funds (50% of the value and 65% of the volume) with stage-agnostic funds trailing closely behind raising $8.8 billion across 13 funds (40% of value and 30% of the volume); funds focused solely on mid/late-staged companies raised $2.1 billion across two funds (10% of the value and 5% of the volume)

*Mass Community Games (MCG) are games driven by online community play. Includes MMOs, MOBAs, battle royale, and metaverse games.

Methodology

In reporting values, DDM only include deals when the investment or acquisition closes, not simply announced. This methodology has been used consistently with DDM data for 17+ years and it ensures that the company is measuring actual activity instead of potential activity.

Additionally, with SPACs, DDM considers the investment value to be what was raised in the transaction, not the company valuation afterward. This is consistent with how DDM tracks investment data, where it tracks the money raised in the transaction and, separately, its effect on the company’s overall enterprise value.

The exclusion of announced deals may result in a large difference between DDM’s quarterly total and other firms, but DDM said its methodology gives a clearer picture of the money deployed in the last quarter, providing valuable data consistency for companies evaluating game industry investment and acquisitions.

Source link