Achieving a soft landing

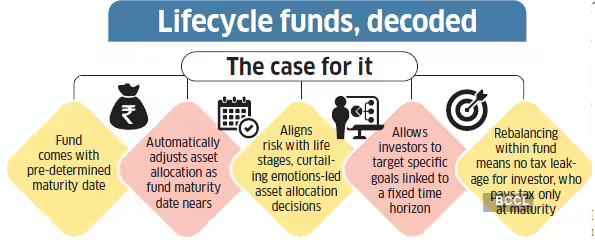

Lifecycle funds take a differentiated path compared to traditional mutual funds. These are essentially openended target-date funds—featuring a predetermined maturity date. The tenure will range from 5 to 30 years, in 5-year increments. Further, a lifecycle fund will automatically adjust its asset allocation as the fund’s maturity date nears. It mechanically shifts the portfolio away from equity to safer instruments over the fund’s tenure, based on a pre-defined glide path.

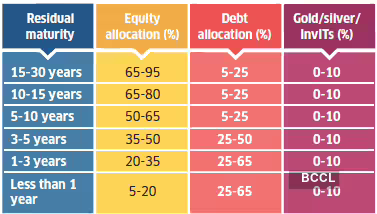

Essentially, funds with residual maturity exceeding 15 years will be allowed equity exposure between 65-95%. As residual maturity falls to 10-15 years, this will be pared to 65-80%. Between 5-10 years, maximum equity is reduced to 50-65%. This further drops to 35-50% and 20-35%, respectively, for residual maturity between 3-5 years and 1-3 years. When the fund’s residual maturity is less than a year, the equity allocation will drop to 5-20%.

This contrasts with traditional solution-oriented mutual funds, which follow a static allocation approach. The glide-path mechanism of lifecycle funds is designed to allow investors to target specific goals tied to a fixed time horizon. It removes human emotions, which lead investors to sub-optimal decisions during the accumulation phase. “By automating portfolio rebalancing and gradually de-risking the portfolio, lifecycle funds help reduce the impact of emotional decisions during periods of market volatility,” says Aditya Agarwal, Co-Founder, Wealthy.in, a wealth management platform.

To further encourage financial discipline, an exit load of 3% will be levied on any exit by an investor within one year of investment. This reduces to 2% for exits within the first two years of investment and 1% for exits within the first three years.

Besides, lifecycle funds solve a vexing taxation problem in rebalancing. When investors rebalance on their own, shifting from one fund to another (say, from an equity fund to a debt fund) invites capital gains tax liability. This tax leakage comes in the way of rebalancing. However, lifecycle funds address this problem because asset rebalancing occurs within the fund. The investor only pays tax at the time of fund maturity. “Over a 20-30 year investment period, this tax-free internal compounding makes a massive difference to your final corpus,” says Basavaraj Tonagatti, Founder, BasuNivesh Fee-Only Financial Planners.

How equity exposure shrinks over time

Lifecycle funds will automatically adjust asset allocation as the fund maturity date nears.

What may not work

- Funds get free hand in how they allocate within each asset class

- Automatic equity reduction over time may cap your long-term compounding gains

- Formuladriven allocation does not recognise varying individual risk appetite

- It will not allow the fund to take advantage of temporary market distortions

Who is it for?

- DIY investors who invest directly, with no adviser or distributor to guide them

- Not for investors who want more control, higher equity exposure, or the ability to time the market

Hidden risks

Some questions remain. One: lifecycle funds seem to have a free hand in how they allocate within individual segments. So, fund managers retain the flexibility to take a large-cap tilt in the equity portion or load up on mid- and small-caps. Similarly, no duration risk boundaries are defined for the bond portion. “The lack of clear internal allocation rules gives the AMC a completely free hand. For a product where you are investing for 20-30 years, this is a serious concern,” avers Tonagatti.

Two: the glide path mechanism could potentially stifle wealth creation in the long term. Early moderation in equity allocation could limit upside participation if equity markets continue to perform strongly towards later years. “Equities create most of the wealth in the later years, when the benefits of compounding are the sharpest. By shifting out of equity in the later years, that advantage is lost,” reckons Nehal Mota, Co-Founder, Finnovate. A mechanism like Systematic Withdrawal Plan (SWP) is geared for a calibrated exit. It allows parts of the corpus to remain invested even as the investor gradually withdraws small amounts.

Three: its formula-driven allocation can make the lifecycle fund rather rigid, argues Mota. “The lifecycle fund is an off-the-shelf product, which does not recognise the finer differences between the risk capacity and risk appetite of people. For instance, two people aged 40 with 10 years to their goal may have entirely different risk capacity, but the lifecycle fund will treat them similarly.”

What’s more, the rigid glide path will not allow the fund to capitalise on temporary market distortions. To be sure, financial advisers have long implemented similar strategies through periodic portfolio rebalancing and SWP as the goal nears, observes Agarwal. “The key difference lies in flexibility. Lifecycle funds follow a pre-defined glide path, which is implemented regardless of market conditions. In contrast, advisers can exercise discretion—by adjusting the timing or pace of equity reduction depending on valuations or market cycles,” he adds.

Who should consider it?

Agarwal maintains that the primary objective of lifecycle funds is goal protection rather than return maximisation. For investors prioritising certainty of outcomes over maximising returns, this approach can be valuable. He reckons lifecycle funds would benefit investors without advisory support or those prone to behavioural biases. Investors who prefer greater control over asset allocation, higher equity exposure for longer periods, or tactical adjustments based on market conditions may find traditional equity or hybrid fund strategies more suitable.