Prediction-market ETFs are proposed exchange-traded funds that seek exposure to event contracts instead of stocks, bonds, or digital assets. They are designed to be traded like ordinary ETFs inside a brokerage account, but the value can depend on one yes-or-no outcome rather than a diversified basket of assets.

The SEC delayed the first batch in May 2026 while seeking more information on product mechanics and investor disclosures. That delay also highlights a key point: these products may look like standard ETFs, but their risk profile can be closer to a single-event contract than a diversified investment.

In this quick guide, we cover what prediction-market ETFs are, how they work, and the key risks you need to understand.

KEY TAKEAWAYS

➤ Prediction-market ETFs package event-contract exposure into ETF form, giving brokerage access to yes-or-no outcome trades.

➤ These funds can track elections, recessions, layoffs, or commodity-price thresholds, not just political events.

➤ A wrong outcome can cause near-total loss, and losses are final with no recourse even if the result is later disputed.

➤ The SEC delayed the first batch in May 2026 while reviewing product mechanics and investor disclosures.

What is a prediction-market ETF?

A prediction-market ETF is an exchange-traded fund that seeks exposure to event contracts rather than to a stock index, commodity, or crypto asset.

An event contract is a derivative instrument that pays out based on whether a specific real-world outcome occurs. Each contract settles at $1.00 if the event happens and at $0.00 if it does not.

The ETF wrapper makes this exposure accessible through a standard brokerage account. Investors do not need to open an account on a prediction-market platform such as Kalshi. That accessibility is part of the appeal, but the ETF label can create a sense of familiarity that the underlying structure does not necessarily support.

Three asset managers, Roundhill Investments, GraniteShares, and Bitwise, filed for more than two dozen of these products with the Securities and Exchange Commission (SEC) in February 2026, based on public registration statements, including Roundhill’s Feb. 13, 2026, filing and similar submissions from competing issuers.

The first wave of proposed funds covers the 2026 midterm elections, the 2028 presidential race, and events such as US recession risk, tech-industry layoffs, and crude oil crossing $120 a barrel.

Prediction-market ETFs are not the same as trading directly on Kalshi or Polymarket. They add fund-level rules, fees, disclosures, and issuer-specific mechanics on top of the underlying event-contract exposure.

How do prediction-market ETFs work?

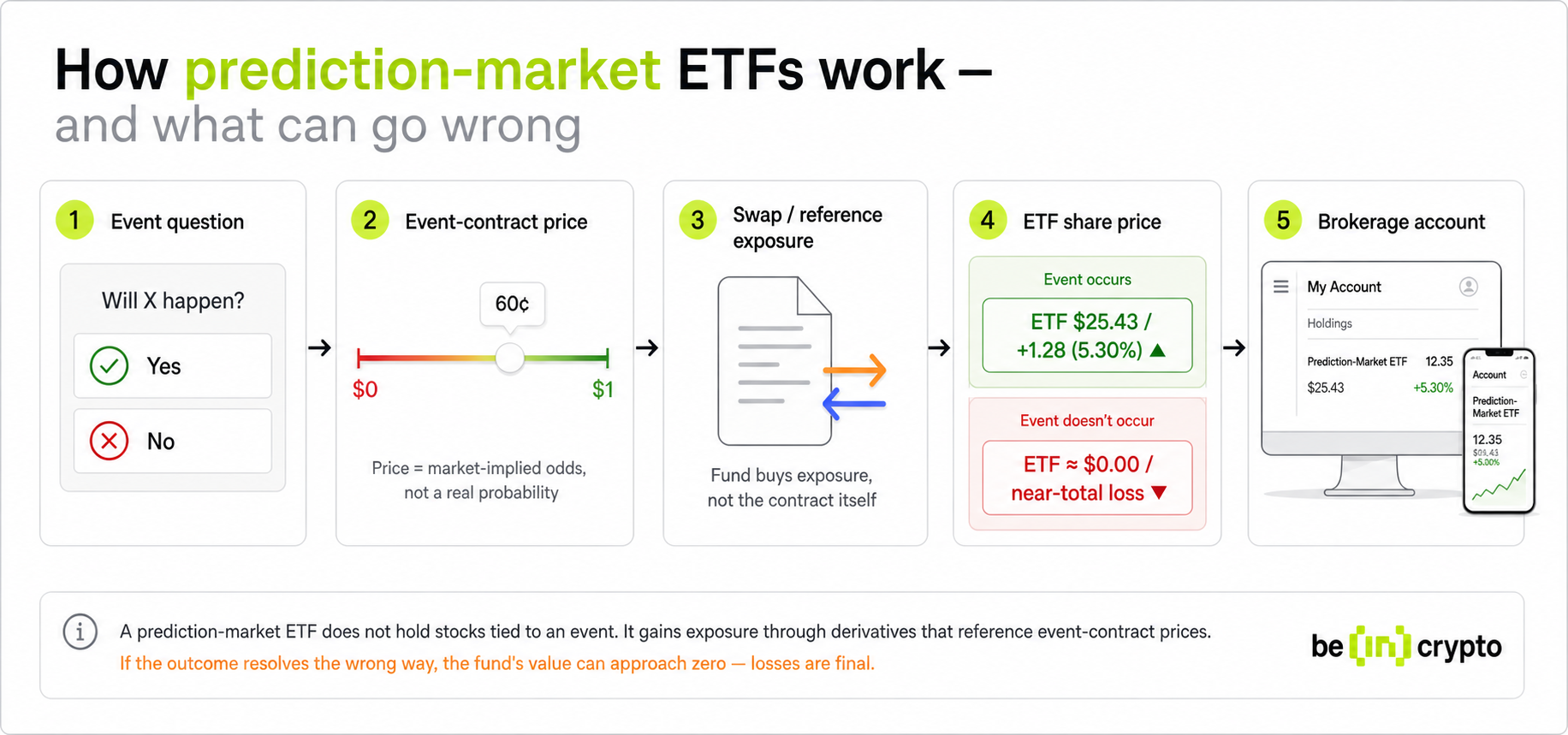

A prediction-market ETF works by gaining exposure to event-contract prices through derivatives, typically swaps, rather than by holding the contracts directly.

The structure works in a simple chain. For perspective, let’s consider the example of a Senate race.

An event question asks whether a specific party wins the seat. A contract tied to that question trades on a CFTC-regulated exchange, with its price moving between $0 and $1 as participants buy and sell based on their view of the odds.

The ETF uses swaps or similar instruments that reference those prices, so the fund’s value tracks the market’s implied view on the outcome. When the result is known, contracts settle at $1 or $0, and the ETF’s value adjusts accordingly.

One important detail often gets missed, though. Contract prices are not objective probabilities. A $0.60 price implies a 60% chance based on market activity, but that figure reflects liquidity, news flow, participant behavior, and contract rules rather than a verified statistical forecast.

Fund structure also matters:

- Roundhill and GraniteShares plan to roll their funds into new contracts tied to the next election cycle or period, so the fund continues beyond one outcome.

- Bitwise’s PredictionShares funds are designed to terminate after the outcome is determined, which more closely mirrors how prediction-market contracts themselves work.

Why did the SEC delay prediction-market ETFs?

The SEC delayed the first batch of prediction-market ETFs on or around May 4, 2026, while it sought more information from issuers about product mechanics and investor disclosures, according to Reuters.

Under SEC rules, ETFs filed under a standard registration process become automatically effective 75 days after filing unless the SEC intervenes. The 75-day window for the February 2026 filings was due to expire in early May. The SEC stepped in before that deadline to push back the effective date while it reviewed the products more closely.

Sources familiar with the matter told Reuters that the delay is likely temporary and does not represent a permanent rejection. The SEC has taken a more accommodating stance toward novel ETF products under the current administration. Issuers, including Bitwise, have publicly noted that other novel products, such as bitcoin ETFs, went through extended reviews before ultimately launching.

The SEC’s concern centers on the binary structure of these products and what disclosures investors need before taking on that type of risk.

That concern overlaps with a broader regulatory issue. Prediction-market ETFs rely on event contracts, which fall under the jurisdiction of the Commodity Futures Trading Commission (CFTC). The CFTC asserts exclusive federal oversight of these markets.

At the same time, some US states, including Wisconsin, have moved to restrict prediction-market platforms under gambling laws. The CFTC has responded by suing those states to defend its jurisdiction, according to a CFTC press release dated April 28, 2026.

The SEC delay does not mean these products have been rejected. Status can change quickly. Any article covering these funds, including this one, should be checked against the latest SEC filings and news.

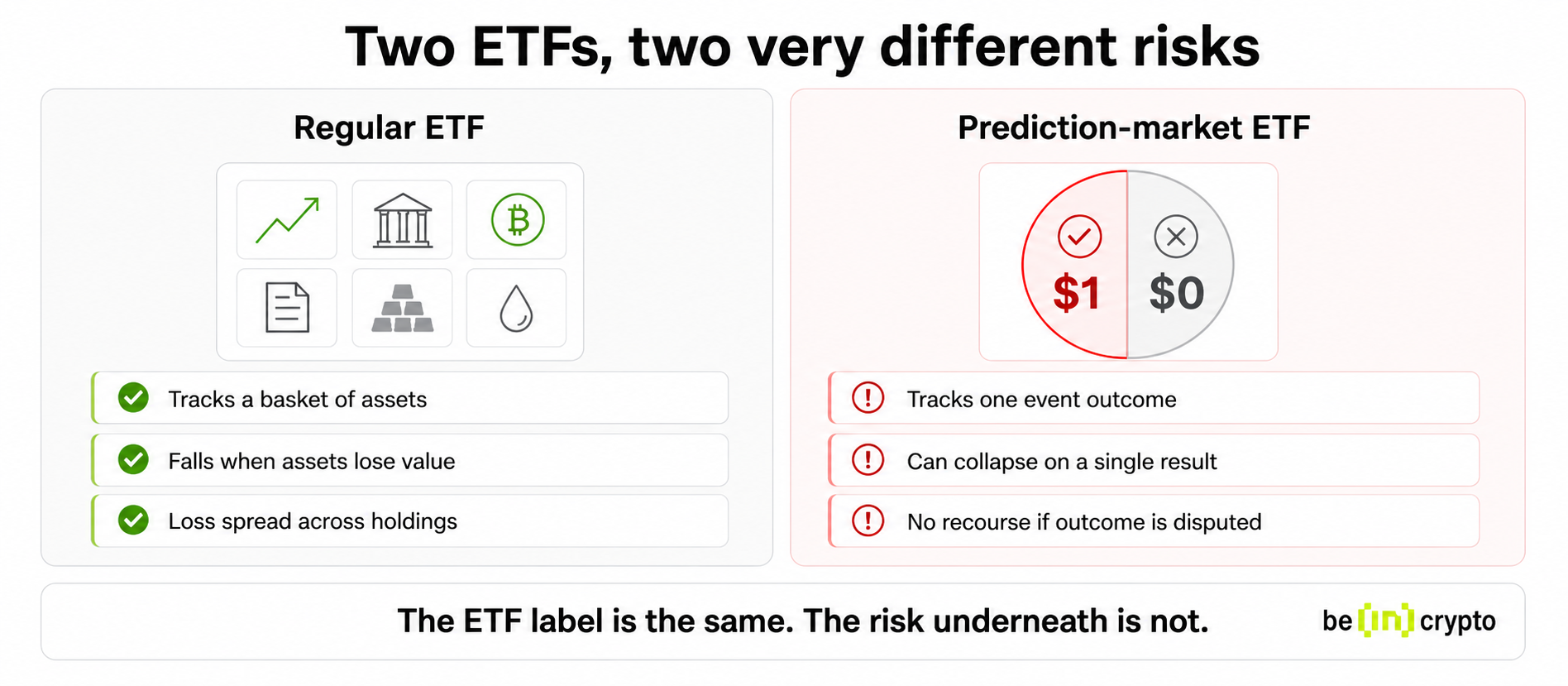

Prediction-market ETFs vs. regular ETFs

The most important distinction for readers coming from a standard ETF background is straightforward. A regular ETF can fall because its assets lose value gradually, while a prediction-market ETF can effectively collapse because a single outcome resolves the wrong way.

| Feature | Regular ETF | Prediction-market ETF |

| Core exposure | Stocks, bonds, commodities, crypto, or indexes | Event-contract outcomes |

| Main value driver | Asset prices | Market-implied event odds |

| Typical structure | Basket or index exposure | Binary or event-linked exposure |

| Main risk | Gradual market decline | Wrong event outcome or contract-price collapse |

| Common reader mistake | Assuming all ETFs are diversified | Treating event ETFs like normal funds |

The ETF label creates a familiarity problem. Most retail investors associate ETFs with diversification and gradual price movement.

In contrast, prediction-market ETFs can move sharply as new information changes the market-implied odds on an event, and they can approach zero if the market consensus shifts firmly against the tracked outcome before the event even occurs.

What are the main risks?

- Near-total loss is the primary risk. Roundhill’s SEC filing warns that investors run the risk of catastrophic losses. If the event does not occur as the fund anticipated, the underlying contracts settle at $0, and the fund’s value can approach zero.

- No recourse is a related risk that receives too little attention. Once the contract settles, the result is final. If the outcome later changes or gets disputed, the fund does not adjust past payouts. For example, if an election result is contested after settlement, your losses are not reversed. There is no way to recover that value after the contract closes.

- Early determination risk applies only to certain fund structures. Some funds may act before the final result is confirmed. If the market treats the outcome as decided, the fund can close or adjust its position early. If that view later turns out to be wrong, you may not benefit from the correction.

- Insider-trading risk is another notable risk flagged in SEC filings. Some participants may have access to information before it becomes public. That can affect prices in event contracts, especially for political or corporate outcomes. Roundhill’s filing highlights this risk, and similar concerns have already attracted federal scrutiny.

- Regulatory uncertainty adds another layer. The SEC-CFTC jurisdictional split, ongoing state-level legal challenges, and the products’ novel structure all mean that the regulatory environment around these funds remains unsettled as of May 2026.

What to check before any exposure

Prediction-market ETFs should not be treated like ordinary diversified funds. Always do your research and verify four aspects before taking any position in one of these products:

First, confirm whether the fund rolls into new contracts after outcomes resolve or terminates entirely. These structures carry different risk timelines.

Second, identify exactly which event or events the fund tracks, and whether those events are narrow enough to create near-total-loss scenarios quickly.

Third, look for the early determination trigger, which describes the conditions under which the fund may act before the official outcome is confirmed.

Fourth, check the fee structure, because funds that roll repeatedly will accumulate costs that compound over time.

Note that the regulatory status of these products should also be verified before any action. As of May 4, 2026, none of the prediction-market ETFs filed in the current wave had received SEC approval to begin trading.