But SIPs reward patience. Over the long term, how long you stay invested matters more than picking the perfect scheme, as per an all-new, ET Wealth – Crisil SIP Study 2026. Every year, the ET Wealth–Crisil SIP study runs the numbers across all equity funds, with one objective: to show the true power of SIPs and, more importantly, how to benefit from them.

Only diversified, actively-managed equity schemes with a continuous NAV history dating back to at least 1 January 2011, have been included in the study. SIP tenures range from 1 year to 10 years. This year, we’ve added a new dimension to our study: how a market crash impacts your SIP and, therefore, how long you need to continue your SIP to soften the blow of a market crash.

Will you lose money?

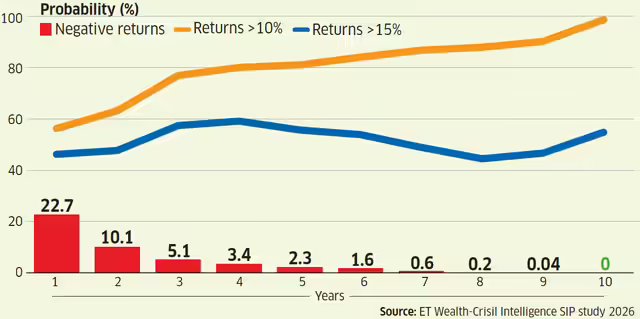

It is widely known that equity markets do not assure returns. But the probability of making a loss goes down as your tenure goes up. The study shows that if you do a 1-year SIP, the probability of a negative return is 22.7%. In simple words, you could lose money 22.7% of the time. The good news is that the probability decreases with tenure. After 6 years, the chances that you make a loss in SIP come down to below 2%. And if you stay invested for 10 years, the chances of a loss are zero.

But avoiding losses is not the reason you invest in an SIP. The question is: will my SIP work? Let’s assume a 10% return is a reasonable worst-case expectation from an equity fund. How long does it take to earn 10% through an SIP? The probability of generating more than 10% SIP returns exceeds 80% from the 4-year tenure onwards and rises to 98.6% for 10-year SIPs, indicating strong return consistency over longer horizons.

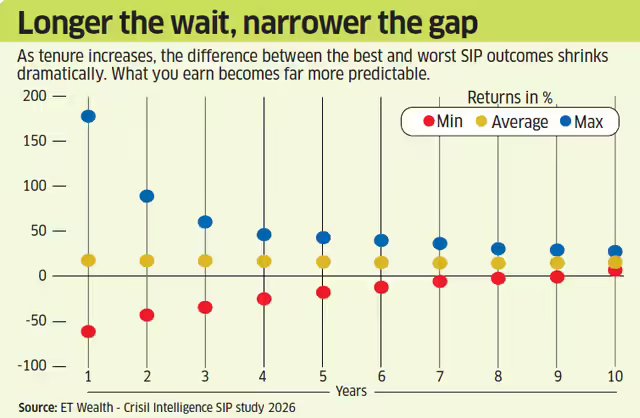

The average SIP returns also stabilise at around 15% beyond the 5-year mark. This suggests that longer holding periods do not necessarily deliver higher returns, but they do reduce the variation in outcomes. Here’s the clincher: over a 10-year SIP period, the minimum return earned was 7%—the worstcase outcome.

In reality, how many investors stay invested for 10 years? “Barely one-third of investors stay with the exact same SIP for a full decade without any interruption,” says Mumbai-based Vinod Jain, principal adviser, Jain Investment Planner. But investors exiting may not necessarily move out of MFs entirely; they could also switch to other funds. Kirttan Shah, Founder & CEO of Truvanta Wealth, says (of his own clients) that if you include those who paused or switched funds along the way but stayed on the SIP journey, the number jumps to 80%. Jain’s own estimate is a broad 50-60%, if switchers are included. Prabin Agarwal, a Siliguri-based MF distributor, says that just 18% of his firm’s SIPs run for more than 10 years. That’s a sobering fact coming from a ground-level, yet top distributor in a small city. The truth is, very few investors run a perfectly uninterrupted SIP for 10 years, but many more stay in the game in some form. The reasons are a familiar mix: market corrections that test patience, life events that drain cash flow, and the very human urge to do something — anything — when a portfolio turns red. Agarwal of Siliguri sums it up simply: completing 10 years in an SIP, he says, is more about behaviour and discipline than about returns alone.

The longer you stay, safer you get

Probability of losing money and probability of earning above 10% for SIPs across 1- to 10-year tenures, across 120 diversified equity schemes (Jan 2011 to Mar 2026)

Returns to realistically expect

The study shows that you stand at least an 80% chance to earn more than 10% returns, if you stay invested for at least 4 years. Interestingly, our study shows that the chances of earning at least a 15% return peak around the 4-5 year mark, after which they taper off slightly. This shows that a long tenure is not necessarily the route to higher returns; it is the path to the most reliable outcomes.

Want a shot at earning a 20% return, at the bare minimum? Our study shows that the probability of generating such high returns falls sharply as SIP tenures increase. The chances of earning over 20% are the highest for 1-year SIPs, at 37.8%. If you continue your SIP for 10 years, your chances of earning at least 20% return drop to 8.9%. Long tenures are about consistency, not fireworks. If you have been in the equity markets for a few years and have seen strong returns, that experience is unlikely to last forever.

Does that mean investors who stay longer are essentially trading peak return potential for consistency and safety—and is that a trade-off most investors understand they are making? “Yes, there is a trade-off, but it is often the right one for most investors,” says Piyush Gupta, Director, Crisil Intelligence. “The highest return periods are usually the hardest to identify in advance, while longer holding periods tend to offer a better mix of consistency, discipline and downside comfort. In investing, catching peaks and troughs are extremely difficult goals. Staying invested long enough to let the process work is the optimal path. Further, a longer investment horizon enables compounding benefits to kick in and enhance wealth creation.”

There are exceptions. Small-cap funds have a 41.8% chance of earning you at least 20% returns if you continue your SIPs for 10 years. Mid-cap funds have a 17.3% chance of generating returns in excess of 20%. In sharp contrast, large-cap funds have virtually no chance of delivering such returns over a 10- year period. The large-cap fund category is the steady, defensive option with an average 10-year return of around 13.5%.

“A bit lower return earned consistently is often more valuable than a higher-return strategy that investors are unable to stick to over the long term,” says Aditya Agarwal, Co-founder of Wealthy.in, a wealth management platform of mutual fund distributors.

Ride out the storm, and time does the rest

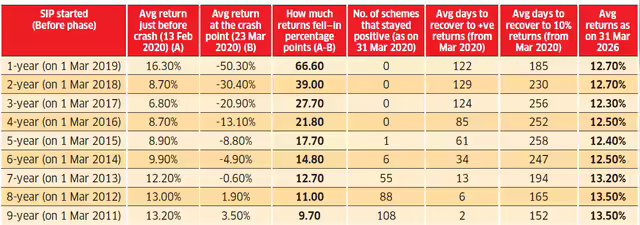

How SIPs across 120 equity schemes behaved during the 2020 Covid crash—from the deepest falls to the quickest recoveries—and where they stood by March 2026 for investors who stayed invested.

Returns are measured as XIRR (extended internal rate of return) which factors in the timing and amount of each SIP investment to give true picture of actual returns earned.

Source: ET Wealth-Crisil Intelligence SIP study 2026

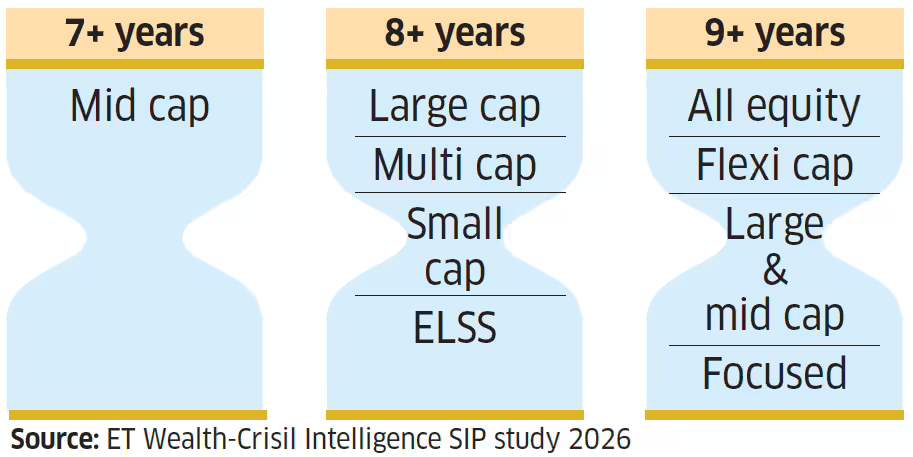

How long before your SIP is guaranteed to make money?

Minimum number of years an investor needs to stay invested in each equity fund category to eliminate any chance of a loss, based on historical data from January 2011 to March 2026.

SIP period to positive returns

How bad is a market crash?

Numbers about long-term returns, however reassuring, tell you nothing about what the journey actually feels like when markets crash. That is the question this year’s study sets out to answer for the first time. This year’s study evaluates the behaviour of SIP portfolios during a sharp market-correction phase (Covid in 2020), focusing on drawdowns and recovery patterns.

The study examines investors who had been running SIPs for 1 to 9 years already when Covid-19 hit. As we always say, this study assumes that investors didn’t stop their SIPs during the pandemic-led market crash and continued thereafter. Essentially, the study checks two things:

Recovery to 0%: How long before your SIP stops losing money, the moment your returns crawl back above zero after a crash? Recovery to 10%: How long before your SIP gets back to doing what you hoped it would — earning a return worth talking about. Zero is relief; 10% is when you start feeling good.

The data also tracks where each portfolio stood by March 2026 — six years after the crash — for those who simply stayed put.

Here is what it shows. Unlike the rolling returns analysis earlier, which captures all market conditions across 15 years, this section zooms in on one specific crash — which is why even long-tenure investors felt some pain here. One-year SIP investors saw the average return crash to -50.3% at the trough (on 23 March 2020), a fall of 66.6 percentage points from its level just before the crash. The pain eased with longer holding periods: 2-year SIPs fell to -30.4%, 3-year SIPs to -20.9%, 4-year SIPs to -13.1%, and 5-year SIPs to -8.8%. By the sixth and seventh years, the damage had largely been contained, with returns at -4.9% and -0.6%, respectively. Remarkably, most 8 and 9-year SIP investors remained in positive territory even at the market’s lowest point. How long does it take to be back to above zero after the crash? It took 122 days for 1-year investors to get back above zero. For 9-year investors to return to positive territory, it took just 2 days.

The data reveals something beyond just returns. An investor sitting at -50% return during a crash is in deep financial pain— and far more likely to panic and stop. An investor who has been at it for seven or more years barely felt the crash. Time in the market, it turns out, doesn’t just protect your returns. It protects your behaviour when it matters most. “When your portfolio shows 12% and markets crash and it becomes 9-10%, you don’t see a significant impact and might not panic. But when you’re a new in vestor, and your portfolio shows a minus, behaviourally you don’t want to stay invested,” says Shah of Truvanta Wealth. The beauty of compounding, explains Hanoz Patel, Co-founder and Partner, PowerPusher Financial Services LLP, is that it kicks in after the 6th and 7th year. “Even if a crash happens then, you’re cushioned,” he adds. Patel observes that youngsters and firsttime salaried investors are often more prone to stop their SIPs due to peer pressure and the urge to spend. Agarwal of Wealthy.in contradicts slightly: “While long-tenure SIP investors are financially better positioned during market crashes, investor behaviour does not always reflect that comfort. Even experienced investors often react emotionally during sharp corrections, though they generally recover discipline fast.”

Shalab Gupta, Founder & CEO of Bibhab Capital, an Agra-based MF distribution firm, says many investors are willing to stay invested as long as they remain in the overall profit zone. “But when capital starts going down, loss aversion hits more strongly,” he adds. The problem is that most investors don’t know their ‘years invested’ number off the top of their head. Gupta of Crisil says that ‘the number of years invested’ should become a standard metric that platforms and distributors regularly communicate to investors, as they do returns. “Returns tell you what happened, while the years invested tell you whether the strategy had enough time to work. For SIP investors, tenure is a far more useful conversation starter than short-term performance. That is because it helps set realistic expectations undergirded by patience, while riding through volatility and economic cycles and allowing the compounding effect to manifest.”

The only number that matters

Fifteen years of rolling data across 120 schemes, across bull runs and crashes and everything in between, produces a remarkably consistent answer to one simple question: how long is long enough? The experts broadly agree on somewhere between 7 and 10 years — though Agarwal of Wealthy.in says 10 years, Crisil puts the floor at 5 years as a pragmatic starting point but notes that real stability only kicks in after 7-8 years, and Prabin Agarwal points out that since SIP money gets invested gradually, even a 10-year SIP has its average rupee working for only about 5 years, making a longer commitment more meaningful.

That’s not the complicated answer. The complicated part, as the investors in the next story (What really happens when life and markets push you to stop your SIPs, P 4) know, is actually doing it.