With the oil shock beginning to make itself felt, returning inflation looks set to take the shine out of both gold and equities. The recent spike in India’s Wholesale Price Index to 8 per cent plus suggests that corporate earnings, after a robust Q4 FY26, can take a breather over the next few months as companies try to pass on pinching input costs to consumers.

Global gold prices tend to be inversely correlated to treasury (government bond) yields. As US inflation rears its head and developed market bonds see a rise in yields, investors may make a beeline for treasuries instead of gold.

However, in investing, whenever opportunities in some asset classes recede, they crop up in others. Today, bonds are turning more attractive for investors, with rising inflation expectations and the renewed possibility of policy rate hikes.

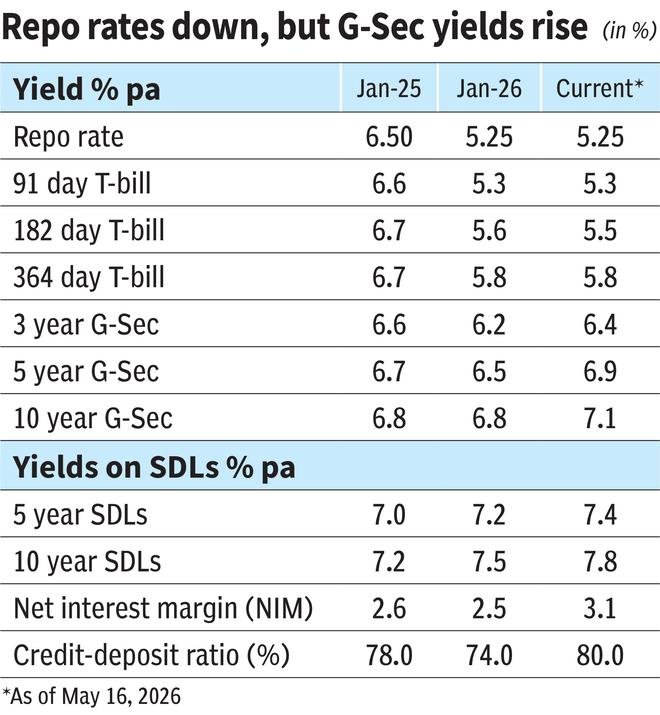

India’s Monetary Policy Committee (MPC) has slashed repo rates by 125 basis points through 2025 and is now sitting on the pause button. But with bond markets responding to the recent oil shock, bond yields in many sections of the market are already ruling at levels that prevailed before these rate cuts!

If low-key tensions in West Asia continue, crude oil remains at $85 plus and the looming El Nino disrupts crop production, analysts are now betting that inflation can shoot past 5 per cent. Should this happen, the MPC can take its finger off the pause button to restart a rate hike cycle.

Bond yields rising

Bond markets always run well ahead of policy actions. Therefore, market yields on bonds have already been rising sharply on expectations of the next rate hike cycle. The yield on the 10-year government security (G-Sec), the benchmark for the bond market, bottomed out at 5.9 per cent in May 2025 and has since climbed to 7.1 per cent now. These are levels that prevailed in 2025 before repo rate cuts began.

Yields on other bonds have climbed in tandem too. (See Table 1). This throws up buying opportunities for investors looking to improve the returns on the debt component of their portfolios.

On the flip side, though, rising rates hurt bond prices. Therefore, while shooting for higher yields, it is also important to limit the losses on your bond holdings from any further rise in rates.

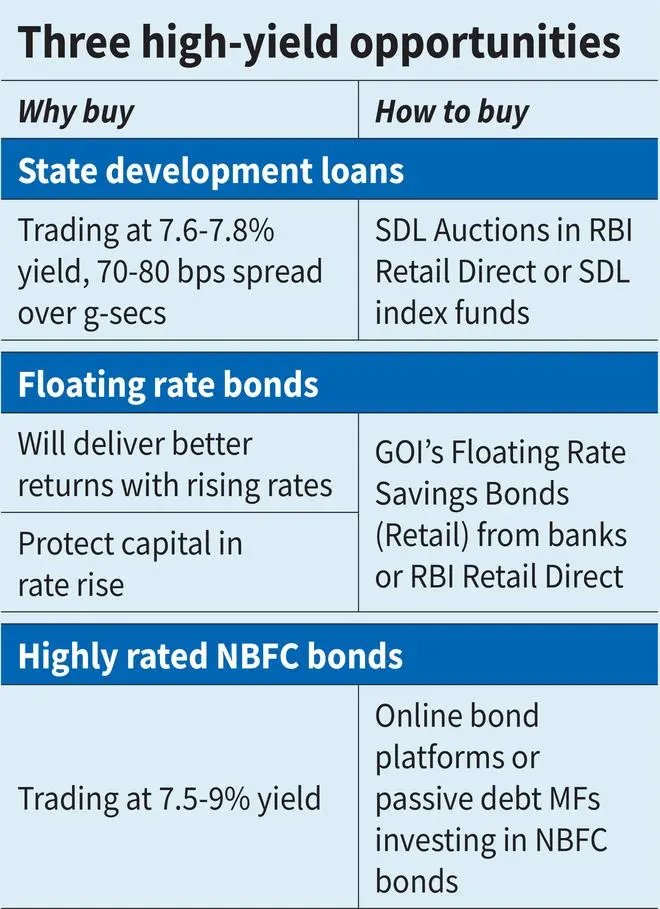

We analysed the entire gamut of bond options, to come up with three sets of high-yielding opportunities that investors can tap today, to balance risk with reward. Do note that we have looked at bonds more from a wealth-creation perspective than the need to generate regular income.

SDLs: Safety plus yield

Historically, the best times to invest in Central G-Secs in India was when the yield on the 10-year G-Sec hovered between 7.5 per cent and 8 per cent. Yields today are well below those levels at 7.1 per cent. However, State Development Loans or SDLs present a high-yield opportunity.

If you look at historical data, SDLs have usually traded at a 30-40 basis point spread over G-Secs of similar tenure. Since the beginning of 2026, however, SDLs are offering attractive yields because the SDL spread has widened to 70-80 basis points. State governments in India have become more prodigious borrowers than the Centre, leading to the market demanding higher yields from them.

Effectively, investors can earn yields as high as 7.6-7.8 per cent by investing in State government bonds, against 7 per cent from comparable Central G-Secs. Theoretically, State governments are slightly riskier entities than the Central government, because they are reliant on the Centre for funds. However, SDLs still offer near-sovereign safety because the servicing of these loans is managed by the RBI (Reserve Bank of India) through an escrow mechanism. There is no past case of a State government in India defaulting on, or delaying a SDL payout. SDLs are also offering higher yields than many PSU and AAA-rated private sector bonds, presenting a sound investment opportunity.

A caveat here. SDLs are a very different instrument from bonds floated by State government entities such as State-promoted power corporations, transport corporations and infrastructure development corporations which offer yields of 9-10 per cent. These bonds are risky bets — not explicitly guaranteed by States and known to suffer from delayed payments in the past.

What to buy: Retail investors looking to buy individual SDLs can open an account with the RBI Retail Direct platform. This allows retail investors to invest sums starting from ₹10,000 in Central G-Secs and SDls. Weekly auction calendars are emailed to you in advance. You need to wait for SDLs of the desired tenure to be auctioned, so you can participate.

The latest SDL auction on May 8, for instance, offered bonds with maturity dates ranging from 2032 to 2056 and yields ranging from 7.5 per cent to 7.9 per cent. Do note that SDLs bought in auctions need to be held to maturity, as they carry limited secondary market liquidity.

If you want to participate in the SDL opportunity without liquidity issues, debt funds investing in indices made up of SDLs offer a good alternative. Mutual fund houses manage a large menu of SDL-only funds, SDL plus G-Sec funds and SDL plus PSU bond funds that mature on specific target dates. These offer efficient, low-cost vehicles to park your debt money if you can find a fund that matches your desired tenure.

Today, if looking to park two-year money, Kotak SDL plus AAA PSU Bond July 2028 Index Fund offers a 7.05 per cent yield to maturity (YTM) with a 0.21 per cent expense ratio.

UTI has a similar SDL plus PSU bond fund maturing in April 2028 yielding 6.98 per cent with a similar cost. For five- to six-year tenures, Kotal SDL April 2032 Top 12 Index Fund and ABSL Crisil June 2032 Fund are the highest yield options with YTMs of 7.6 per cent and 7.5 per cent respectively, at annual expenses of 0.20-0.21 per cent. Valueresearchonline.com has a comprehensive list of passive debt products from which you can choose the right SDL fund.

FRSBs: Capitalise on the rise

Usually, debt investors shy away from floating rate bonds because of variable returns. But when the economic outlook tells you that rates can only flat-line or go up, floating rate bonds make plenty of sense.

There are three ways for Indian investors to participate in floating rate bonds. They can buy floating rate debt mutual funds, government bonds pegged to floating rates or the retail GOI floating rate savings bonds sold by banks and RBI Retail Direct platform. Of the three, the last is the most viable option.

With very few private issues of floating rate bonds, floating rate debt funds often invest in fixed rate bonds and use swaps to mimic floating rates, which leads to these funds imperfectly mimicking floating rates.

The RBI periodically auctions floating rate bond borrowings by the Centre. These bonds offer yields that are 64-100 basis points higher than the 182-day treasury bill rate (the average of the last three auctions). The current 182-day T-bill yield is about 5.5 per cent. However, because of the peg to the six-month T-bill, these bonds are usually suitable only as short-term parking grounds. You also need to know when the next floating rate auction is coming up and participate in it.

What to buy: The Government of India’s Floating Rate Savings Bonds (FRSBs) meant for retail investors are the only practical option for investors looking to ride the rate cycle through floating rates. These bonds peg their interest rate to a 35-basis point spread over the prevailing interest rate on the NSC. This is a small savings scheme for which the government resets interest rates every quarter.

FRSBs have offered an island of high rates to investors across rate cycles, because when policy rates fall, the government tends to shield NSC from deep cuts. When rates rise, NSC rates tend to rise. They are also fixed 25 basis points above the five-year G-Sec yield. This allows FRSB investors to earn nearly 60 basis points above prevailing G-Sec rate at any given point in time. The current floating rate on FRSBs is 8.05 per cent per annum.

These bonds can be bought from banks or the RBI’s Retail Direct. However, the only negative is that these bonds have half-yearly interest, which is paid out and carry no cumulative option. They are neither listed nor tradeable and carry a seven-year lock-in period. However, the ability to park any amount in these bonds with no age restrictions is a big plus.

Corporate bonds

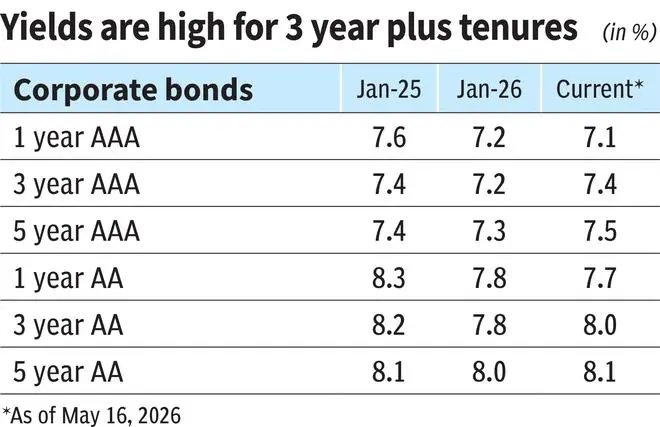

Apart from SDLs, corporate bonds have also seen their spreads over G-Secs widen sharply in the past year, presenting opportunities for bond investors (See Table 2). While yields on short-term corporate bonds (upto one year) are 40-50 basis points below 2025 levels, yields on bonds with three-year-plus maturity are back to levels that prevailed before the rate cuts started.

Currently, AAA-rated corporate bonds offer yields of about 7.4-7.5 per cent for three-year tenures. Those rated at AA offer 8 per cent for the same tenure. Within corporate bonds, NBFC bonds offer an island of higher returns.

What to buy: Investors can earn higher yields from this space in three ways.

# 1 You can buy individual AAA- or AA-rated bonds from online bond platforms. However, as these platforms tend to aggressively promote lower-rated bonds with high yields, it is important to keep off bonds with default risks. Bonds from listed entities backed by reputed business groups with AAA or AA credit ratings from CRISIL, ICRA or CARE are the safer bets. Currently, for instance, the Indiabonds platform has a CARE AA-plus rated bond from Cholamandalam Finance maturing in June 2029 and a CRISIL AAA-rated bond from Aditya Birla Capital maturing in April 2036 both at an 8 per cent yield, which are worth a look. Make sure to avoid any bonds offering double-digit yields. The higher the yield compared to G-Secs (which trade at 6.2-7 per cent), the greater your risk of losing your principal!

# 2 You can buy passive index funds that focus on highly-rated NBFC bonds. Currently, for investors with 2-year money, Edelweiss CRISIL IBX AAA Financial Services Bond January 2028 Index Fund (7.7 per cent YTM), Kotak Nifty AAA Financial Services March 2028 Fund (7.7 per cent YTM), Nippon Crisil AAA Financial Services January 2028 (7.7 per cent YTM) are some of the top options. For five-year money, Bharat Bond ETF 2031 (7.5 per cent YTM) is a good bet. Valueresearchonline listings can help you find funds with the right tenures.

# 3 You can buy actively-managed corporate bond funds, after filtering them for healthy YTMs and low costs. Currently, Franklin India Corporate Bond Fund (7.8 per cent YTM and 0.25 per cent direct plan cost), ICICI Pru Corporate Bond Fund (7.75 per cent YTM and 0.36 per cent cost) and SBI Corporate Bond Fund (YTM of 7.75 per cent and 0.37 per cent expenses) fit the bill. Most of these portfolios are invested in AAA-rated debt. Given their average portfolio maturity of five years, these options are more suited to your three- to five-year money.

The author is a Contributing Editor

Published on May 16, 2026