Vanguard’s BondBuilder models are less a breakthrough than a price reset. These new investment-grade corporate bond-ladder exchange-traded fund model portfolio options have all the strengths and weaknesses of what could be built from their defined-maturity ETF predecessors but at a lower cost. Here, we revisit the topic of how bond-ladder ETFs work and how they might help in accomplishing one’s investing goals. In fact, although the models are designed for advisors, their simplicity means retail investors could easily implement them as well.

Vanguard BondBuilder Basics

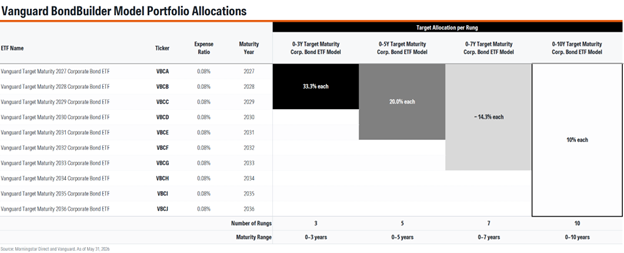

Launched on April 28, 2026, the Vanguard BondBuilder suite comprises four perpetual bond-ladder models: the 0-3Y, 0-5Y, 0-7Y, and 0-10Y Target Maturity Corporate Bond ETF Models. Each strategy equal-weights its assets across its maturity range using Vanguard Target Maturity Corporate Bond ETFs for each year. The annual cost, without factoring in any custodial or platform fees, is only 0.08%, 2 basis points less than what rivals charge.

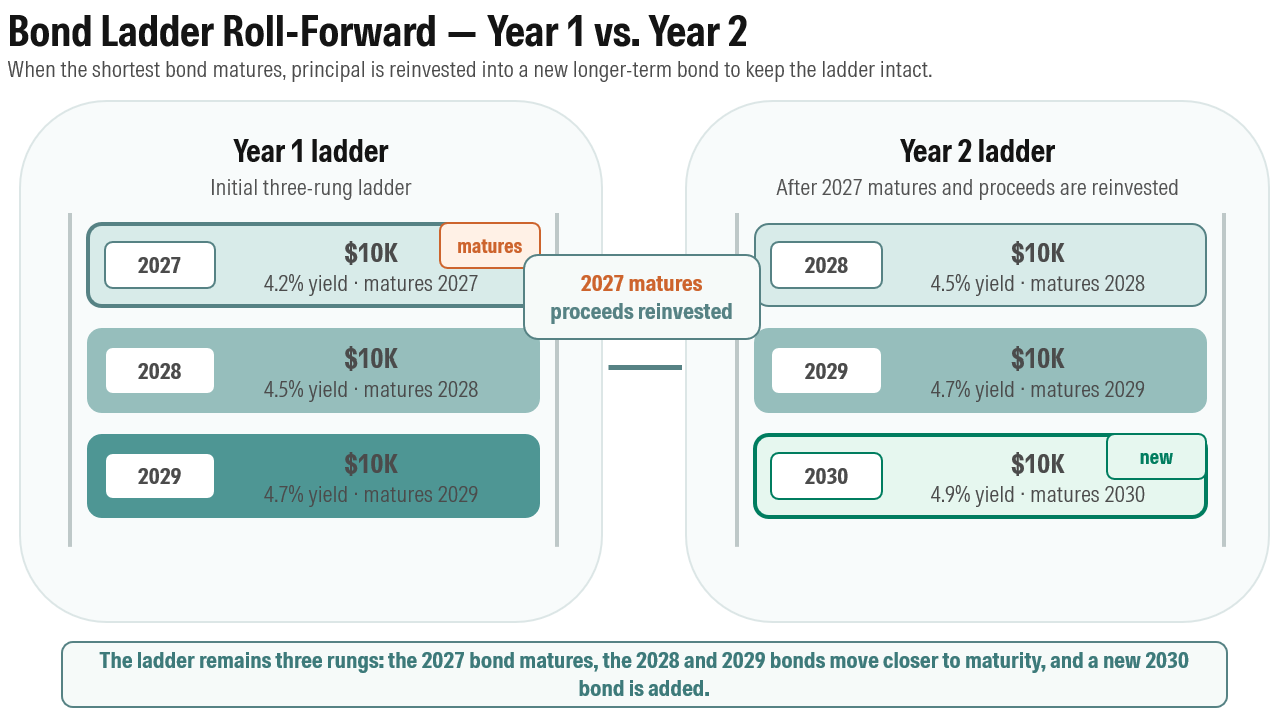

The 0-3 bond-ladder model strategy, for example, apportions a third of its assets each to the 2027, 2028, and 2029 vintages. As the 2027 bonds mature, that rung of the ladder ceases to exist, and its assets are reinvested in the 2030 vintage, creating a new rung and preserving the ladder’s three-year maturity. The five-, seven-, and 10-year models work similarly. Those preset ranges, however, are not the only possible configurations. Investors using the underlying target-maturity ETFs directly could build ladders around different horizons, such as a 0-4-year ladder that allocates a fourth of its assets to each rung, if that better matched their spending needs or liability schedule.

Like similar models from iShares and Invesco, Vanguard’s suite provides reliable and resilient options for managing bond-ladder cash flows over time. If interest rates rise, investors keeping their money in the ladder will reinvest the principal of their maturing target-maturity ETFs at the new, higher prevailing rates. If rates fall, the reinvested principal won’t earn as much as previously, but target-maturity ETFs in the ladder that have yet to mature will still have the same, now higher, rates locked in.

Assuming no defaults, this ETF adaptation of a traditional bond ladder delivers a fairly predictable income stream and protects investors from losing their principal as long as they hold each ETF to maturity and redeem it then.

Bond-Ladder ETF Practicalities

The appeal of bond-ladder ETFs is practical rather than predictive: Vanguard BondBuilder models don’t try to outsmart the bond market. Instead, they try to provide a basic laddered portfolio while easing, if not removing, operational headaches in a cheaper, more consistent, and easier-to-govern way.

That matters because bond ladders are straightforward in concept but labor-intensive to implement for certain fixed-income market segments. Individual bonds offer control and clear maturity dates, but corporate bonds can be cumbersome to source, size exposure in a portfolio, diversify through exposure to other bonds, monitor, and then roll. Separately managed accounts solve much of that burden, but they add higher fees, often require higher minimums, and may offer less transparency for advisors who want a standardized framework across clients.

Vanguard’s BondBuilder models sit between those approaches. They forfeit the customization of individual bonds and SMAs, which are more amenable to introducing credit tilts, tactical interest rate calls as measured by duration, or issuer-level control. BondBuilder models, though, offer diversified annual maturity exposure through ETFs at a cost structure that works in smaller portfolios.

Defined-Maturity ETFs as the Foundation

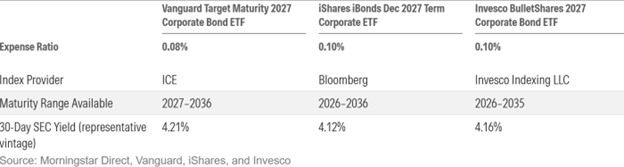

Defined-maturity ETFs are the foundation for BondBuilder portfolios, which have been around for more than 15 years. What was originally called the Claymore BulletShares Corporate Bond ETF suite debuted in June 2010, and Invesco acquired it about eight years later. BlackRock got into the game in 2013 via its iShares business. The latter now has roughly $25 billion in assets under management in defined-maturity ETFs, while Invesco has about $22 billion. With its 10 new target-maturity corporate bond ETFs covering maturities from 2027 through 2036 at a cheaper price than rivals’, Vanguard is clearly hoping to become a prominent, if not dominant, player in this market as well.

Vanguard Undercuts Competitors

Each Vanguard ETF tracks a corresponding ICE Maturity US Corporate Constrained Index, which means it holds a diversified basket of investment-grade corporate bonds maturing in the same calendar year. In its target year, the portfolio winds down as bonds mature, and the ETF ultimately liquidates by distributing its remaining assets to shareholders. The structure resembles an individual bond, but investors own a portfolio of bonds, not a single bond with a fixed payment.

Simplicity Can Mislead

Target-maturity ETFs are useful building blocks, but those maturity dates should not create a false sense of principal certainty. A defined-maturity ETF is not the same as holding an individual bond to maturity. An individual bondholder owns a specific security that, absent a default, returns par at maturity. A defined-maturity ETF owns a portfolio of bonds and is subject to taking in cash and distributing it (if in-kind redemptions are not available) throughout its life and then liquidating its remaining value when the ETF reaches its maturity date. On that score, both are mostly protected from the effect of interest rate shifts that naturally taper off as the portfolio winds down. Both are also subject to changing credit spreads, albeit idiosyncratic credit risk is high for the individual bondholder. Given that the defined-maturity ETF rung of a bond ladder is a collection of bonds, though, its composition can be affected by its interim cash flows and associated transaction costs. (The indexes on which Vanguard’s ETFs are built won’t buy any bonds callable before the ETF’s maturity year.) On the whole, then, an ETF does not provide quite the same principal certainty, absent default, as owning an individual bond to maturity.

In both cases, though, a laddered structure means some bonds or ETFs are becoming more stable as they approach maturity. That helps avoid the need to sell long-maturity or beaten-down investments to pull assets out of the strategy because it staggers reinvestment across years, and some are always approaching maturity. If a client needs to liquidate the entire ladder early, though, the market-value protection largely disappears whether you’re doing it with ETFs or individual bonds.

Cash drag is another consideration. As bonds mature or are called in the ETF’s final year, proceeds shift into cashlike investments. Vanguard and ICE have tried to mitigate this risk by using a SOFR-linked return that keeps final-year cash earnings closer to money market rates rather than sitting idle.

Credit risk also matters. The ETFs hold investment-grade corporate bonds, but corporate yield spreads can widen sharply in a downturn. They can provide steady cash flow through interest payments in stable credit environments, but they should not be treated as Treasury substitutes if the goal is ballast during equity selloffs.

The Roll in Action

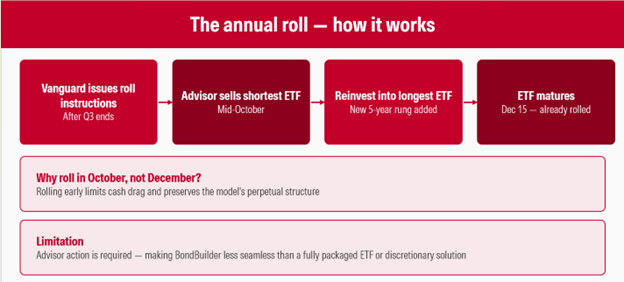

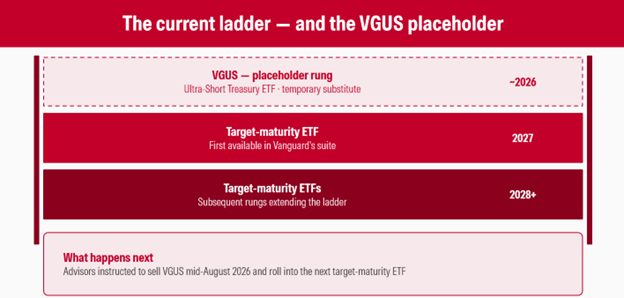

Since the BondBuilder models equal-weight their rungs and use one ETF per maturity year, adding a new rung is straightforward. Vanguard makes it as easy as possible for advisors by providing the model weights and roll instructions, though advisors remain responsible for implementation as would any retail investors who construct their own models. As the nearest-dated ETF approaches maturity, Vanguard instructs clients to sell it and reinvest in the longest-dated ETF in the ladder. The roll happens after the third quarter ends, typically in mid-October, ahead of the ETF’s Dec. 15 maturity. Rolling early limits cash drag and preserves the model’s perpetual structure. Still, the process requires action, making BondBuilder less seamless than a fully packaged ETF or discretionary solution.

Vanguard’s target-maturity ETF suite begins with 2027 maturities, so the models currently use the Vanguard Ultra-Short Treasury ETF VGUS as a temporary substitute for the nearest rung. Vanguard will instruct advisors to sell the Vanguard Ultra-Short Treasury ETF in mid-August 2026 and roll into the next target-maturity ETF for each ladder.

What BondBuilder Does—and Does Not—Deliver

BondBuilder models are best understood as a cash flow and liability-matching tool for planned liabilities. They are less compelling as a core bond allocation. The models are built entirely from corporate bond ETFs, which means they concentrate in a single credit-sensitive sector. Longer rungs are also very sensitive to changes in the overall level of interest rates and/or credit spreads; in other words, they carry meaningful risk. Investors who need portfolio ballast during equity market selloffs could pair a BondBuilder model with Treasuries or other high-quality holdings; those who want customization should use the target-maturity ETFs directly.

Vanguard’s BondBuilder models, in the end, do not change the basic logic of bond ladders, but they make them more accessible, leaving adoption as the remaining test. Vanguard’s BondBuilder models and its own defined-maturity ETFs are likely to change the bond-ladder landscape, at the very least putting pricing pressure on current incumbents BlackRock and Invesco. In that sense, it’s a win for investors writ large.