")

Darrin Hughes

As a recent retiree who seeks passive income from my investments to help support my lifestyle while I no longer receive a steady paycheck, I look for strong performing CEFs (closed end funds) and ETFs that pay monthly high-yield distributions. In particular, I am attracted to monthly paying funds that offer a high-yield distribution that is expected to continue to offer a strong source of income for the months and years ahead. Secondary to my desire for income is the possibility of capital appreciation as well, or at least the avoidance of large, unrealized losses on my capital invested.

Two of my top holdings that meet those criteria include the Cornerstone funds, CLM and CRF. For example, the Cornerstone Total Return fund, which I covered in an article published in March of this year, is part of the foundation for income that I am building in my Income Compounder portfolio. This is what I wrote about CRF back in late March:

With a current distribution yield of about 17% and a level monthly distribution that is unlikely to change until next January, I rate CRF a Buy. The top holdings are all performing well, and NAV is rising while the premium is below the historical average. For those investors who wish to secure a strong source of current income with some potential capital appreciation in 2024, I suggest taking a closer look at CRF and its sibling fund, CLM, which is trading at an even smaller premium.

As funds that mimic the top holdings in the S&P 500 but offer income investors a 16% to 17% yield (with an additional bonus when you reinvest shares at NAV while the funds trade at a premium), I feel that the Cornerstone funds are a must-have for any serious long-term income investors who wish to have a relatively secure, monthly high-yield cash flow that is likely to benefit from the continued strength in the overall market for the next several years or longer.

Then a few months ago, I learned about a relatively new ETF that has similar top holdings (but only 15 stocks), offers an even higher yield currently, and has demonstrated the potential for capital appreciation as well. That fund is the Rex FANG & Innovation Equity Premium Income ETF (NASDAQ:FEPI). While I see a few similarities between FEPI and the Cornerstone funds, there are some substantial differences as well, the biggest one being that FEPI is an ETF but also the fact that the income FEPI pays out in distributions comes from covered calls on the fund holdings, versus capital gains and net income from the fund’s equity holdings in the case of CLM/CRF.

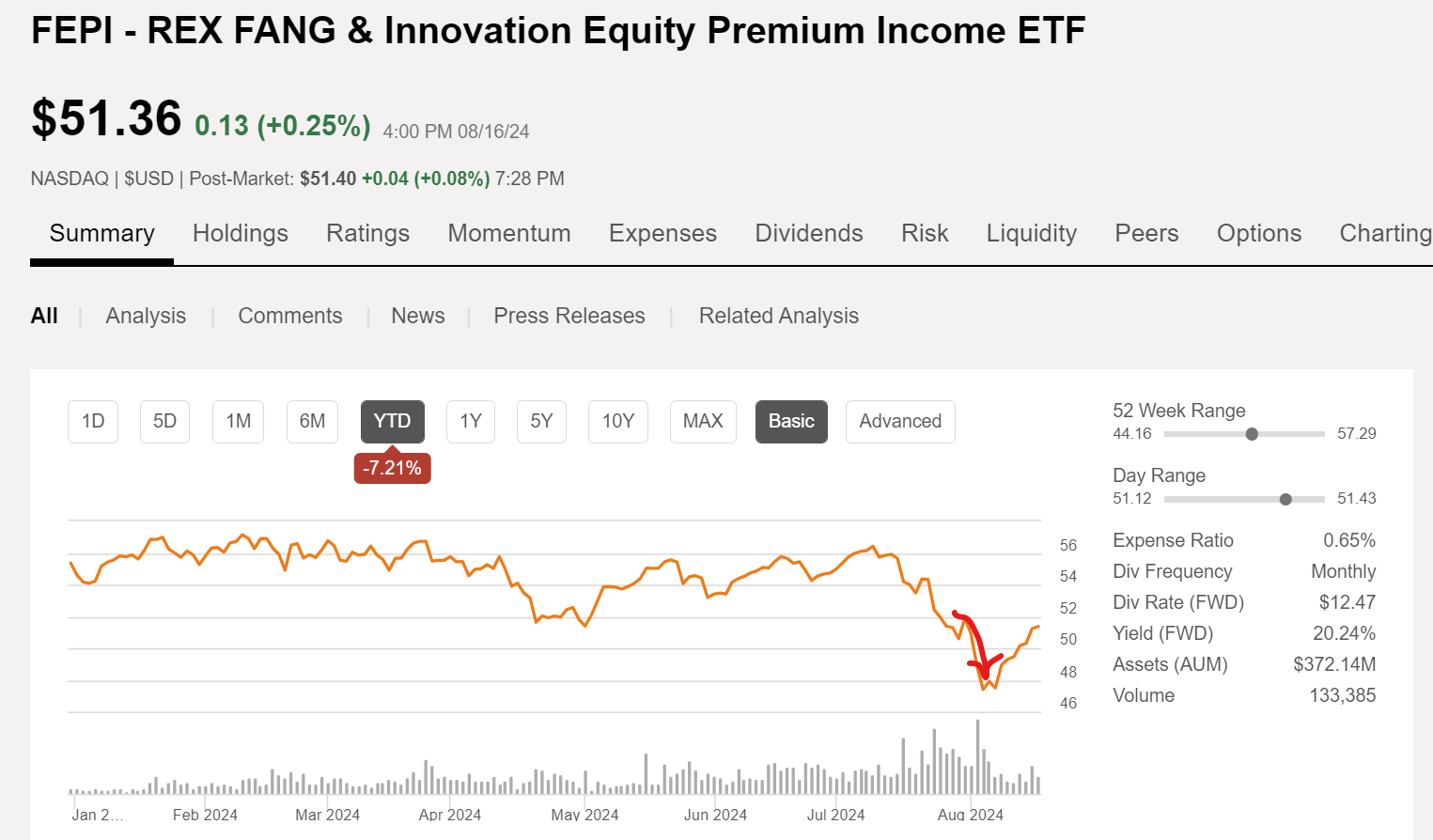

Nonetheless, I feel that FEPI could also provide another building block for the foundation of an income investor’s portfolio. According to the fund’s fact sheet, FEPI combines big tech stock exposure with covered calls to generate current income. One benefit of the fund’s approach, similar to the YieldMax funds that generate income from covered calls on single Mag 7 stocks, includes a downside buffer to mitigate potential price declines in the big tech stocks that FEPI holds. However, one risk with this strategy is that if the entire tech sector takes a turn for the worse, this fund will likely see a big drop in price, and potentially a decline in the distributions as well. In fact, that theory was tested for a few days recently, as you can see in the price chart, which witnessed a dramatic price drop in early August.

Seeking Alpha

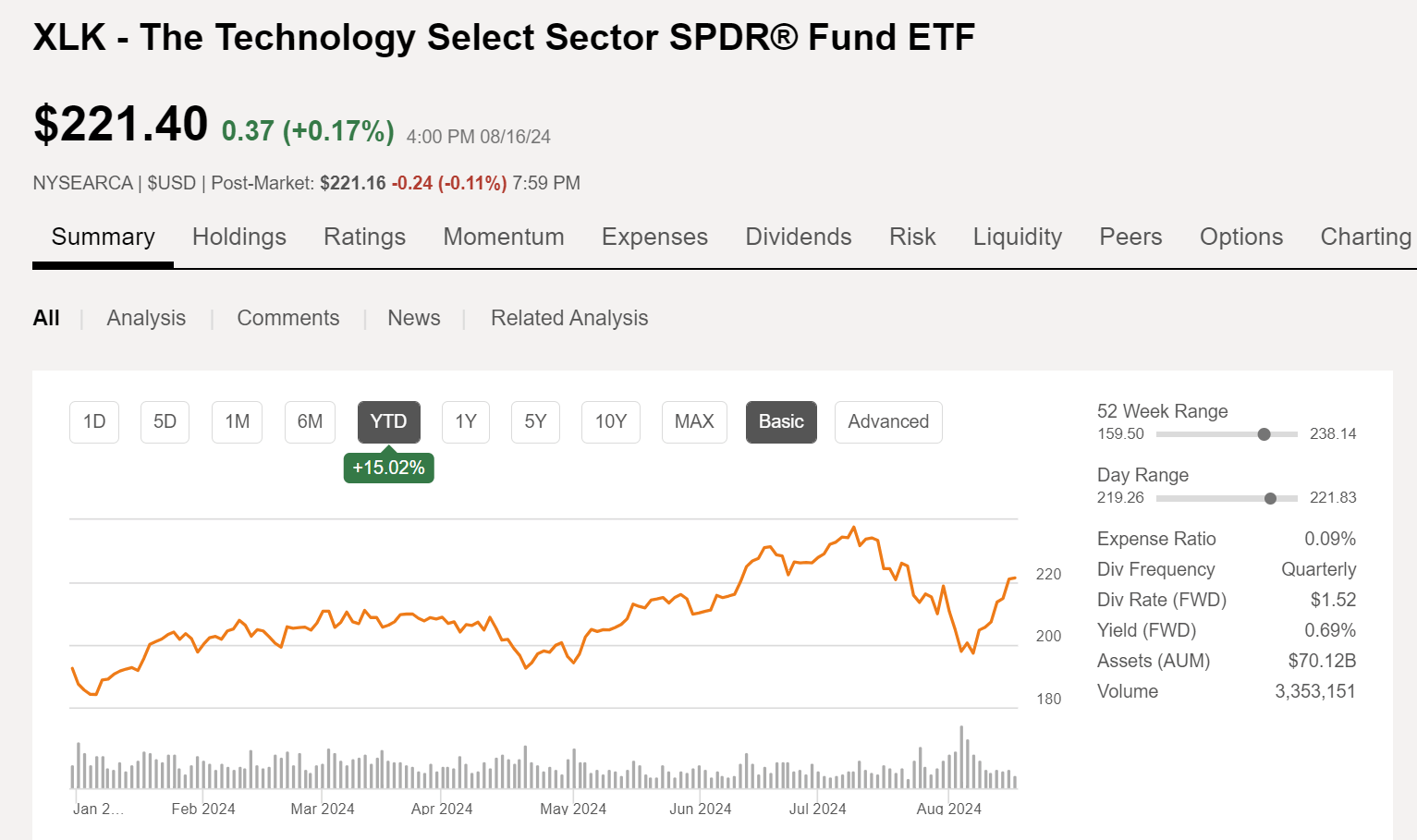

Of course, the XLK tech fund experienced a similar drop in price with essentially the entire sector falling out of favor due to the expected “rotation” out of tech stocks that many had been predicting, but now appears to be reversing again.

Seeking Alpha

FEPI Top Holdings, Similar to CLM Top Holdings

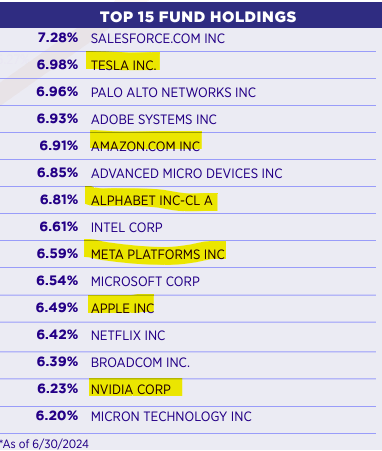

Another reason why I feel that FEPI is somewhat similar to the Cornerstone funds is due to some overlap in the top equity holdings. Six of the top 10 holdings in CLM are included in the 15 stocks that FEPI holds, at least as of 6/30/24 as shown on the FEPI fact sheet.

FEPI fact sheet

The top 10 holdings shown for CLM are as of 12/31/23, so they may have changed some since then.

Seeking Alpha

Also, CLM only holds about 30% of its total holdings in Technology sector stocks, while FEPI is 100% technology stocks with covered calls written against those 15 stocks that it rebalances each month and reconstitutes quarterly as explained on the fund website.

The FANG & Innovation Index is equally weighted and includes 15 highly liquid stocks focused on building tomorrow’s technology today. The index rebalances monthly and reconstitutes quarterly.

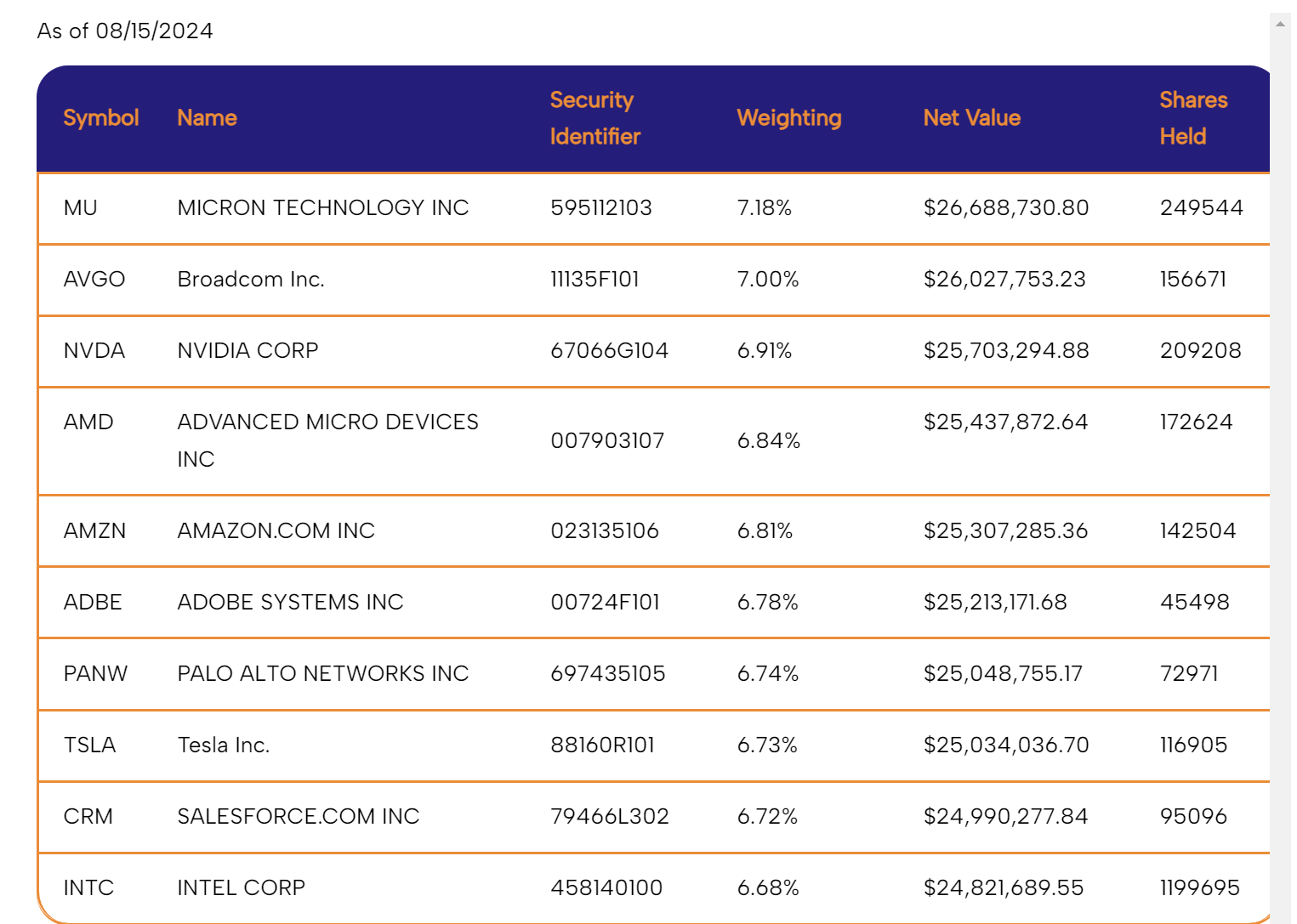

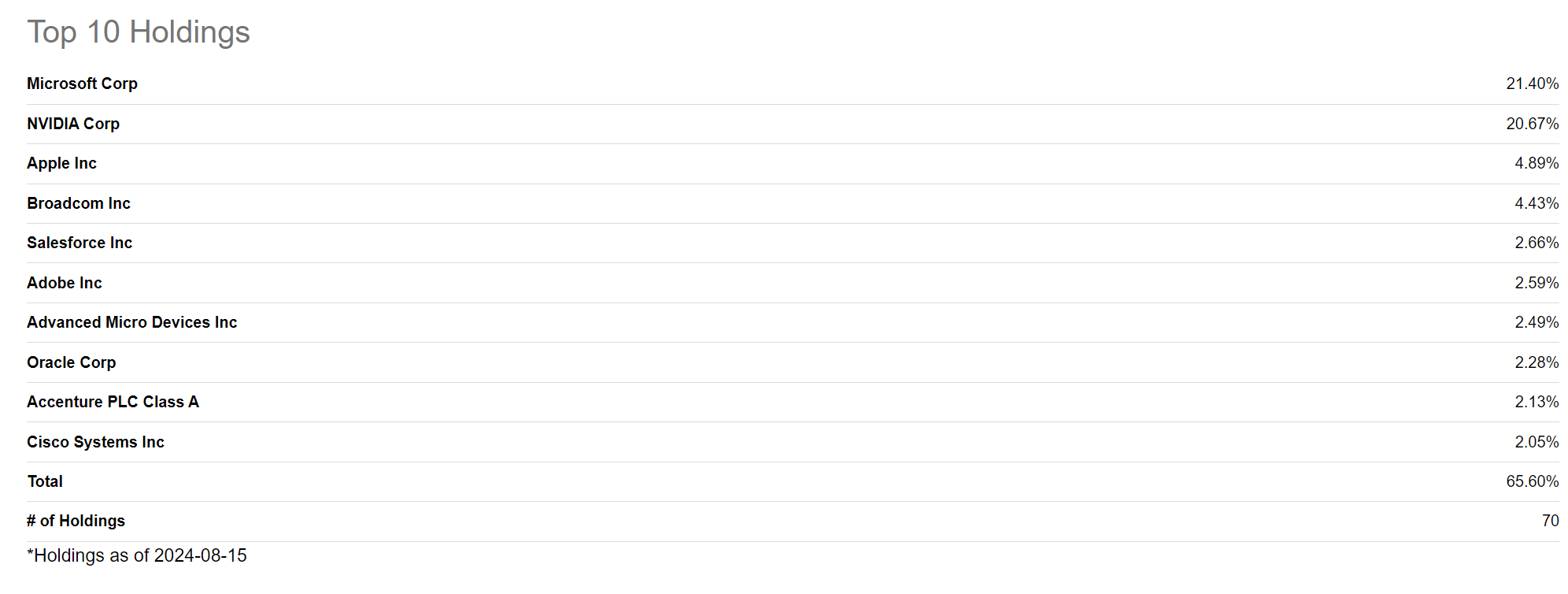

In fact, you can see from the latest snapshot of FEPI top 10 holdings from the fund website that as of 8/15/24 the top holding is now Micron, which was the bottom (smallest percentage) holding back in June. Likewise, AVGO and NVDA are now #2 and 3 while they were bottom of the list in June. Also, Intel was a top holding back in June (and still is) at about 6.6% and the poor earnings report caused that stock to plummet by 30%, also negatively impacting the NAV of the fund.

FEPI website

The 15 stock holdings in FEPI are based on the Solactive FANG Innovation Index, as described on the fund fact sheet:

The Solactive® FANG Innovation Index includes 15 highly liquid stocks focused on technology. These large, tech-enabled equity securities are all listed and domiciled in the U.S. The Index is comprised of eight core-components Apple (AAPL), Amazon (AMZN), Meta Platforms (META), Alphabet (GOOGL), Microsoft (MSFT), Netflix (NFLX), NVIDIA (NVDA), Tesla (TSLA) AND the seven top traded names across the technology sector.

FEPI Fund Distributions

As of the end of June, the distribution rate based on the latest monthly distribution times twelve offers a 25% annual yield. Because the fund has only been in existence for just over 9 months now (with an inception date of October 2023) the annual performance is not meaningful, however, the total return of the fund since inception at market price is an impressive 26% as of the end of June, and 20% as of 8/16/24 due to the price decline that dropped the price in August.

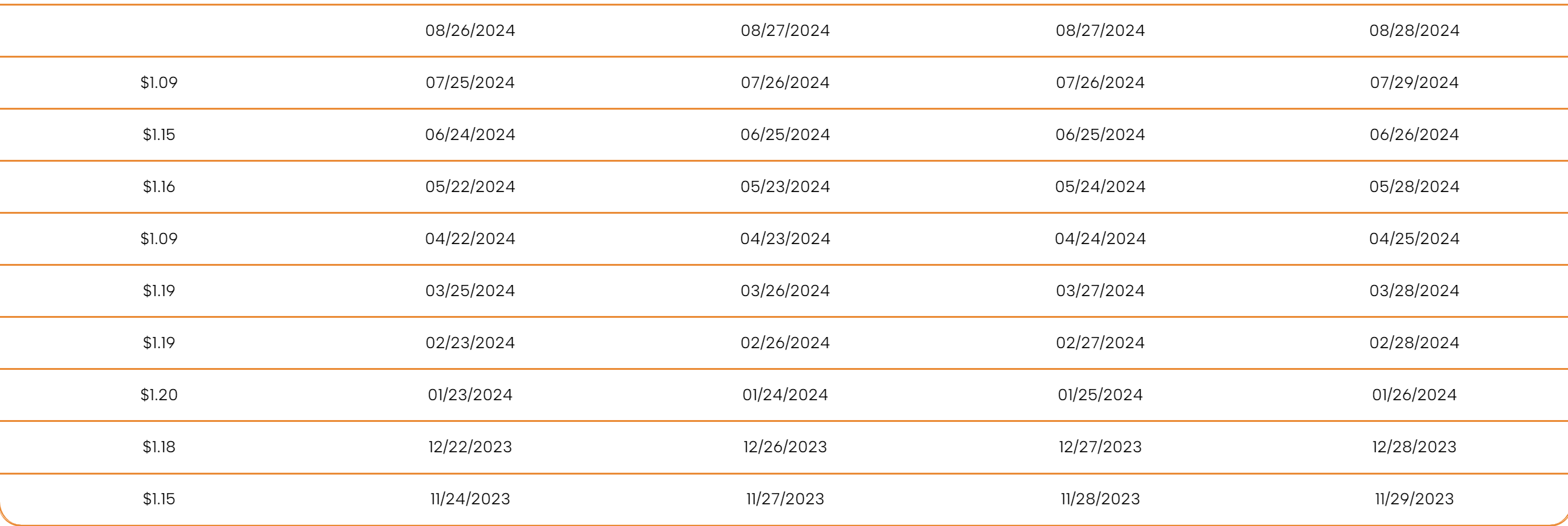

Even more importantly, as an income investor who is more interested in the monthly income coming into my account than the daily gyrations of the price, the fund has paid nine relatively consistent monthly payouts that look likely to continue on a similar pace for the foreseeable future based on the market action of the fund’s holdings. From the fund website, the distribution history shows the 9 monthly payments distributed so far in the fund’s young life. The next payout is expected at the end of August and is likely to be in the range of $1.10 to $1.20.

FEPI website

At the low end of $1.10 per share paid on average over 12 months, that would result in $13.20 per share for one year. With the current market price of the fund, closing at $51.36 on 8/16, that would result in a whopping yield of 25.7%.

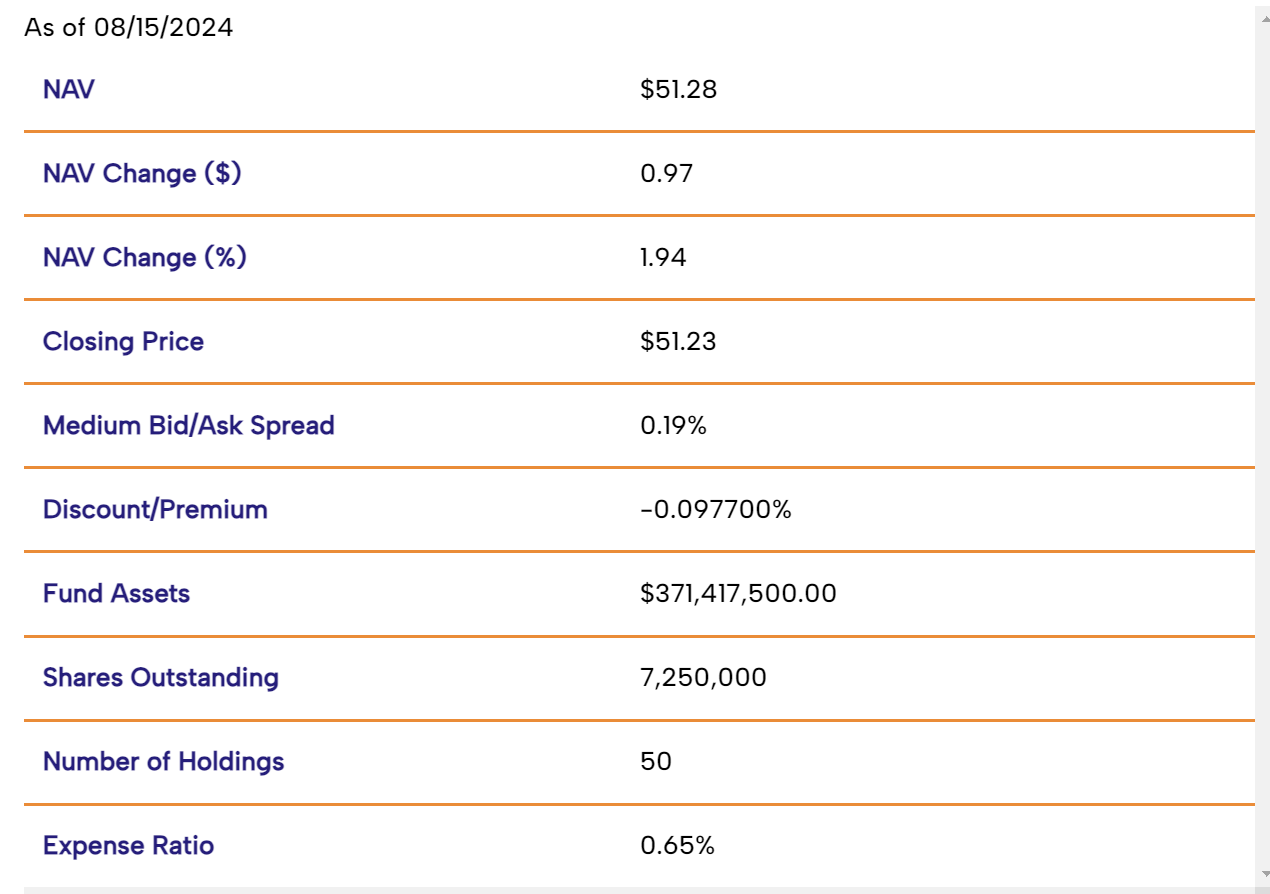

The fund has grown its net assets to more than $370M according to the latest data on the website, more than triple the fund size since March when it reached $100M. There are about 7.25M shares outstanding and like most ETFs the fund trades near par (at a $0.05 discount on 8/15/24). The fund expense ratio is a reasonable 0.65%, somewhat less than the 1% or so that the YieldMax funds claim (or 1.28% in the case of YMAX, the nearest peer fund to FEPI).

FEPI website

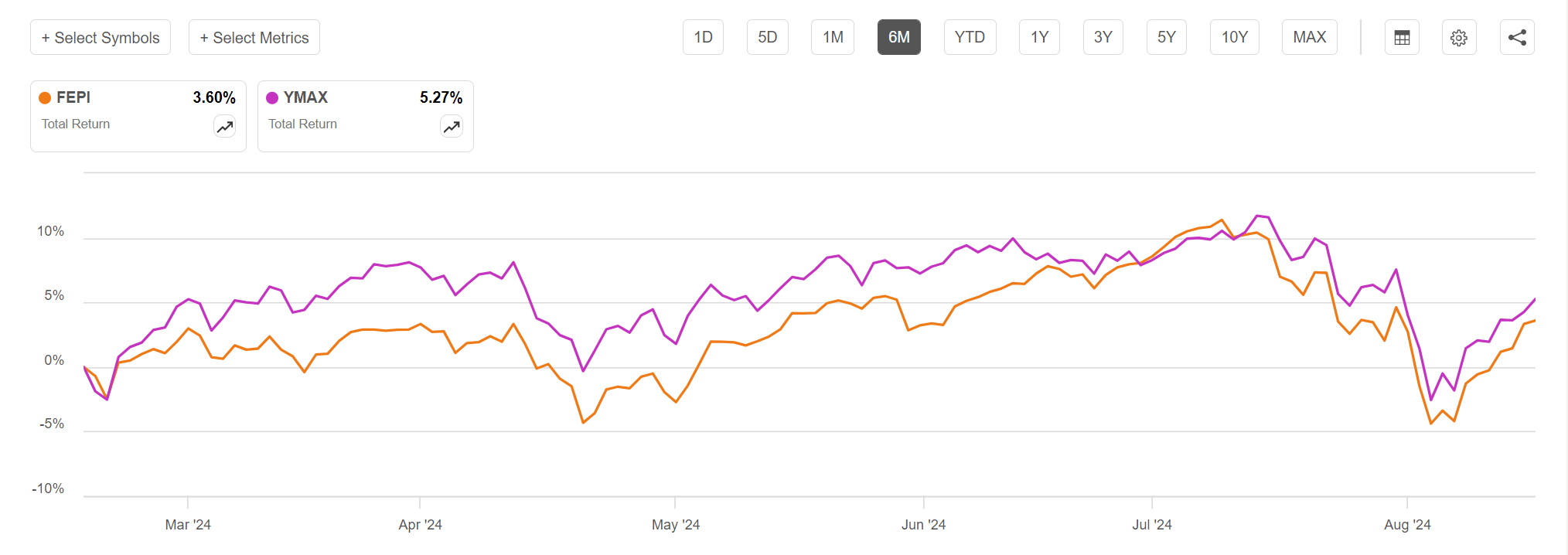

The YMAX fund from YieldMax started after FEPI (with inception date of 1/16/24) and may have been offered in response to the competition from that fund. The YMAX fund operates differently, but essentially holds the various single-reference stock covered call funds from YieldMax as its core holdings, as opposed to writing covered calls against the individual stocks in its portfolio like FEPI does. YMAX is also worth exploring further because the strategy for that fund also appears to be working well so far this year, with an even better total return than FEPI since its inception. This chart for the past 6-month period illustrates the slight outperformance by YMAX on a total return basis.

Seeking Alpha

Risks and Outlook for FEPI and Technology Stocks

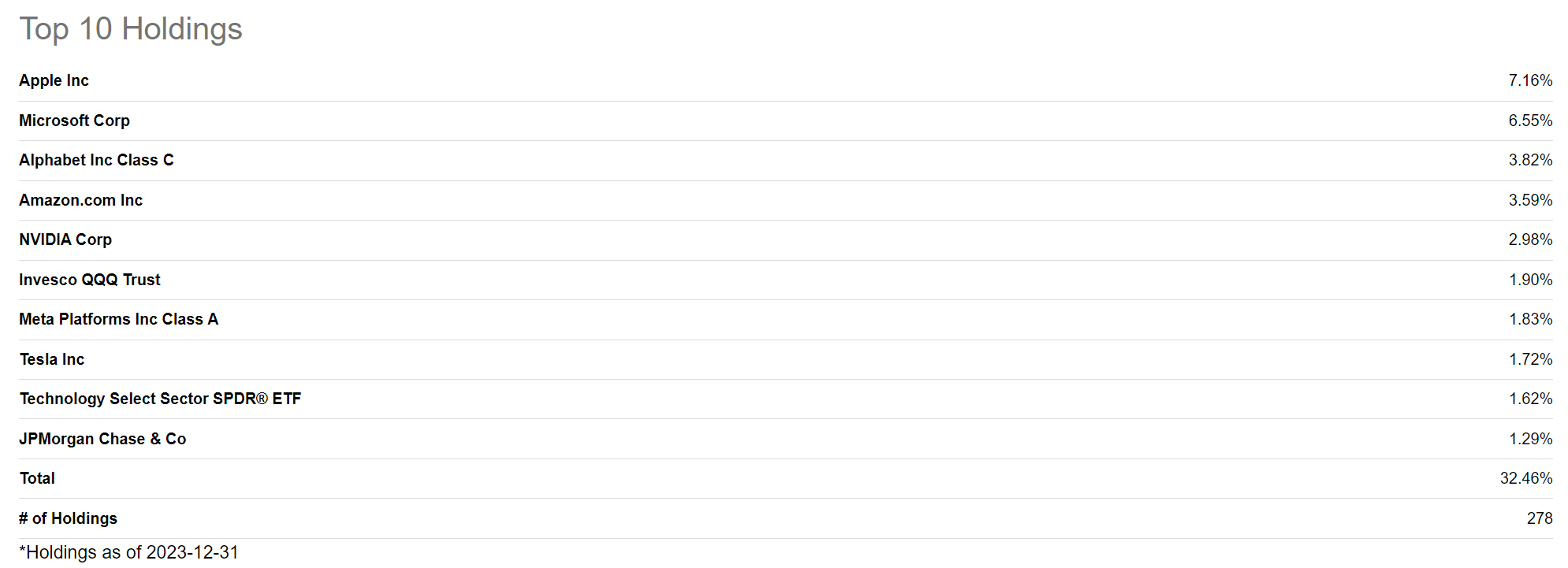

If you consider that the top holdings in the XLK technology fund are nearly the same as the top 10 holdings in FEPI, we can approximate the return potential for FEPI based on the outlook for XLK. With the added presumption of continued market volatility due to several macro concerns such as the upcoming election in the US, ongoing conflicts in Ukraine and Gaza, potential interest rate reductions (or not) in September, and lingering inflation, the income potential from covered calls becomes even more compelling.

XLK top 10 holdings (Seeking Alpha)

The impact of the AI revolution may have stalled temporarily; however, it is likely in my opinion that the future for these top tech holdings is still looking quite promising in the long run. In fact, after the early August rout on tech stocks, Truist bank came out with an overweight rating on the sector.

“The bar for positive surprises became too high leading to a sharp rotation out of the sector,” Keith Lerner, chief market strategist at Truist, said in a Thursday statement.

Now, the sector is down ~12% from its mid-July peak, with semiconductors down nearly 20%. “This is contrasted by tech’s forward earnings estimates continuing to rise and are currently hovering at all-time highs. This suggests the recent setback was due more to crowded positioning as opposed to a shift in fundamentals,” he said. “Still, our view is the risk/reward has improved for the tech sector and the secular story remains intact.”

Similarly, JPMorgan suggested on August 5 that tech stocks could be offering an opportunity to “buy the dip” and suggested that the rotation out of tech stocks may have run its course. Based on weekly results for the week ending August 16th, it appears that JPM made the correct call as XLK was the top-performing sector fund for the week as encouraging economic data quelled recession fears.

Call Writing Strategy Risk

It is worth noting that there is some risk in the potential effectiveness of the call writing strategy the fund employs. This risk is spelled out in detail in the fund Prospectus, so I am including here for investors to read and understand.

The path dependency (i.e., the continued use) of the Fund’s call writing strategy will impact the extent to which the Fund participates in the positive price returns of the individual stocks comprising the Index and, in turn, the Fund’s returns, both during the term of the sold call options and over longer time periods. If, for example, each month the Fund were to sell 7% out-of-the-money call options having a one-month term, the Fund’s participation in the positive price returns of the individual stocks comprising the Index will be capped at 7% in any given month. However, over a longer period (e.g., 5 months), the Fund should not be expected to participate fully in the first 35% (i.e., 5 months x 7%) of the positive price returns of the individual stocks comprising the Index, or the Fund may even lose money, even if the prices of the individual stocks comprising the Index have appreciated by at least that much over such period, if during any month over that period the individual stocks comprising the Index had a return less than 7% . This example illustrates that both the Fund’s participation in the positive price returns of the individual stocks comprising the Index and its returns will depend not only on the price of the individual stocks comprising the Index but also on the paths that the individual stocks comprising the Index take over time.

Another risk to the fund is turnover in the management team, leading to the potential for poor returns despite individual stock performance. On the fund website, there were two portfolio managers indicated as portfolio managers working for Vident Asset Management as sub-advisors implementing the fund strategy. On May 28, 2024, one of those managers departed from his role at Vident and left the team.

Our investment strategies are robustly designed and rules-based, firmly ensuring that the transition will not impact the management and performance of the fund. Rex Advisors continues to lead with a strong commitment to the stability and integrity of our investment processes. The departure of a team member from our sub-advisor does not affect our ability to effectively manage the fund or our ongoing promise to deliver consistent results.

Fortunately, there does not appear to be any immediate impact to the fund due to this change, and perhaps that is because of the robust, rules-based strategy employed. Also, as pointed out in the press release, REX Advisors is the fund advisor and Vident serves as sub-advisors under the guidance and direction of REX. The REX team is impressive on its own merits, with Greg King, CEO and Founder, having filed a patent for the first ETN in 2006.

Summary: Buy FEPI for the Income if you Believe in the Future of Big Tech

While I have mostly watched from the sidelines as the AI-hyped technology sector led by the likes of Nvidia and the other Mag 7 stocks have resulted in incredible returns for growth investors, the FEPI ETF offers an opportunity for income investors to get on the big tech bandwagon. Like the mature, high-yield Cornerstone CEFs that generate high-yield income from top S&P 500 stocks, FEPI takes advantage of the price gains from top technology stocks (specifically those 15 stocks that are in the Solactive FANG Innovation index) to grow the fund’s NAV while writing covered calls against the stocks to generate income.

If you believe as I do that, we are still in the relative early innings of the AI revolution, and as fund strategies that include income generation from writing call options become better optimized and continue to demonstrate successful returns, this relative newcomer to the public market should offer potential for strong returns. Furthermore, markets are likely to stay choppy even as macro conditions remain healthy, leading to increased potential for even greater income from covered calls.

Tony Pasquariello, in a Friday note, assessed the risk/reward of the market following a “remarkable stabilization” in the S&P 500 after U.S. recession fears early last week fired up Wall Street’s key volatility measure (VIX) to pandemic-era levels, above 65. They also drove a 12% plunge in Japan’s Nikkei 225 Index. Since then, the S&P 500, after dropping more than 8% from its all-time high, has narrowed the loss to ~2%, and marked a sixth consecutive gain on Thursday. “At the same time, however, I think the market will continue to sweat the trajectory of growth and the political/geopolitical news feed,” he said. “In addition, the narrative around AI is less one-sided than it was just a few months ago,” Pasquariello said.

The FEPI fund is not well suited for growth investors or for more conservative total return investors, though. As we witnessed during the early August market plunge, the fund price and income generation potential can be adversely affected by strong moves to the downside. There are risks to consider, but overall, this fund offers solid potential for high-yield income paid monthly along with some price gains from growth in the underlying holdings. I rate FEPI a Buy at a price under $52 and a Strong Buy if the price should drop below $49 again. As of June of this year, I added FEPI to my own Income Compounder portfolio at a 2% position and I am enjoying the monthly high-yield income.